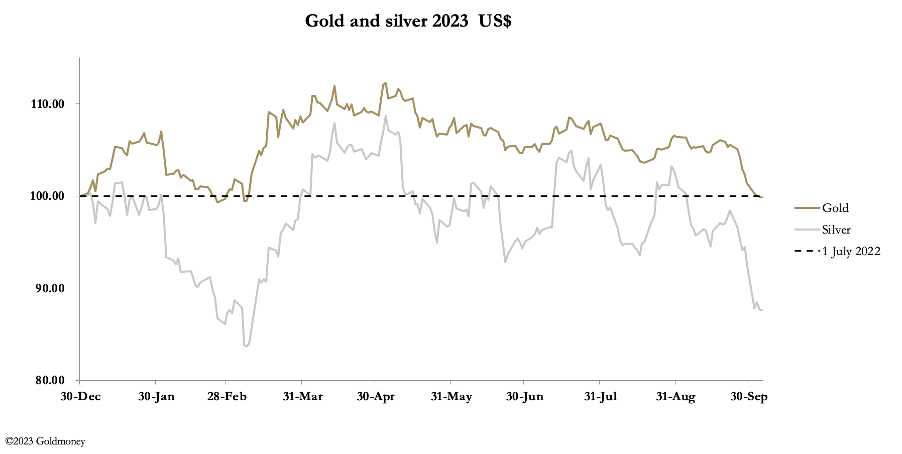

The sell-off in precious metals continued as bond yields continued to rise and a strong dollar persisted. In early trade in Europe this morning, gold was $1822, down another $26, unchanged on the year. Silver traded at $21, down $1.17. Comex volumes in both metals declined from good levels, indicating that selling pressure is declining.

Comex deliveries in both metals increased in volume, reflecting the end of the October contract. Including last Friday, 8,735 gold contracts stood for delivery in the last five business days, representing 27.17 tonnes, and 334 silver contracts representing 52 tonnes. This persistent demand for delivery is becoming a must-have source for those turning paper gold and silver into bullion, with 338.25 tonnes of gold and 3,514 tonnes of silver delivered this year so far.

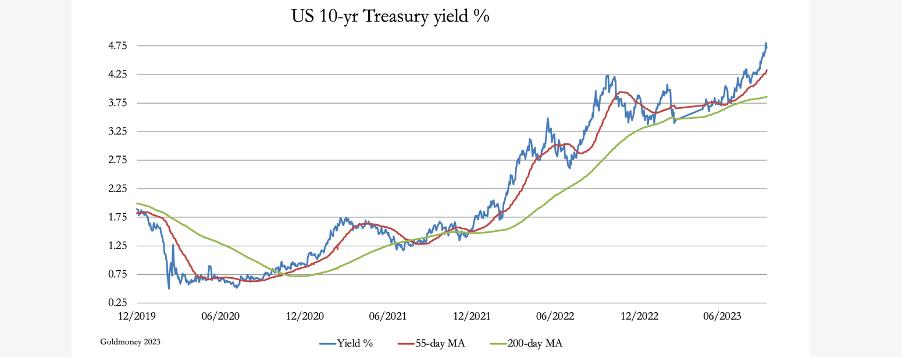

Driving gold and silver lower have been persistently rising bond yields taking markets by surprise. The chart below of the US Treasury 10 year note yield is remarkably bullish — until you remember that this is of rising yields, collapsing bond prices, undermining all financial asset values.

What’s driving this? It appears to be a demand for collateral in a global version of liability driven insurance, which created a crisis in the UK gilt market a year ago. Demand for collateral top-ups is leading to bonds being sold for cash. It is also affecting not just dollars, but euros as well. The problem centres on interest rate swaps, a global market with a notional value of over $400 trillion. Those on the fixed interest leg of an interest rate swap are being forced to provide collateral to those on the floating rate leg. And, like the UK’s LDI market, these swaps are often leveraged by four- or five-times requiring matching multiples of collateral.

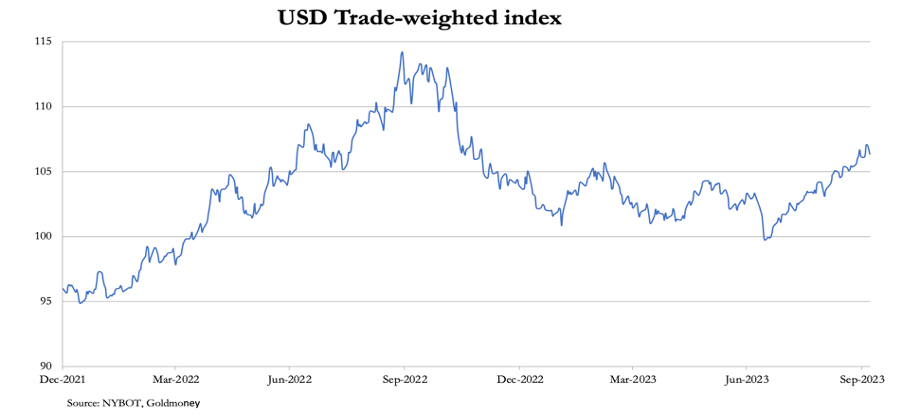

At times when interest rate differentials matter, bond markets under selling pressure are a headwind for gold. And the liquidation of bonds to meet collateral demands are not yet leading to wider systemic concerns. Consequently, higher bond yields are supporting the dollar’s TWI, which is up next.

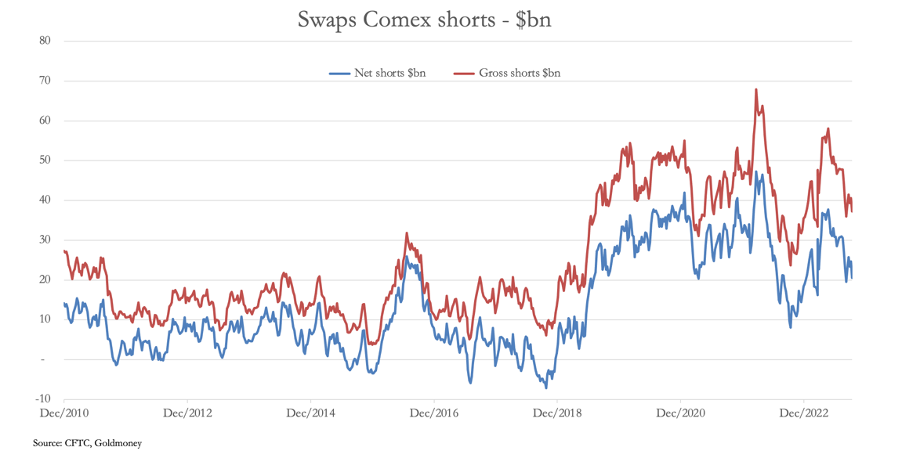

Again, this is seen by traders as negative for gold. It helps the bullion banks to close down their short positions in paper markets. Our next chart is of the value of gold futures shorts in the Swaps category on Comex.

Having reduced the value of their shorts significantly, on the 26 September, the last Commitment of Traders report, the Swaps (mostly bullion bank trading desks) were still net short $21bn. That will have reduced somewhat from there, but they are still some way from closing them out. Other things being equal, there will still be downward pressure from this source.

But this reckons without the damage bond yields are doing to the banking sector. Bond losses on bank balance sheets are mounting and collateral values are falling. Non-performing loans in the commercial real estate sector and a residential mortgage crisis is in the wings. When markets become more aware of these systemic risks, gold and silver prices should soar.

Buka akaun dagangan patuh syariah anda di Weltrade.

Source link