Why do virtually all the mainstream pundits think the Federal Reserve has won the inflation fight?

Maybe it’s just wishful thinking. They want the Fed to win so it can go back to what it does best – creating more inflation with artificially low interest rates and quantitative easing.

Regardless, most of the mainstream punditry hyped the November CPI report as more positive news on the inflation front. The CNBC headline reflected the consensus – inflation “slowed” last month.

Except it really didn’t.

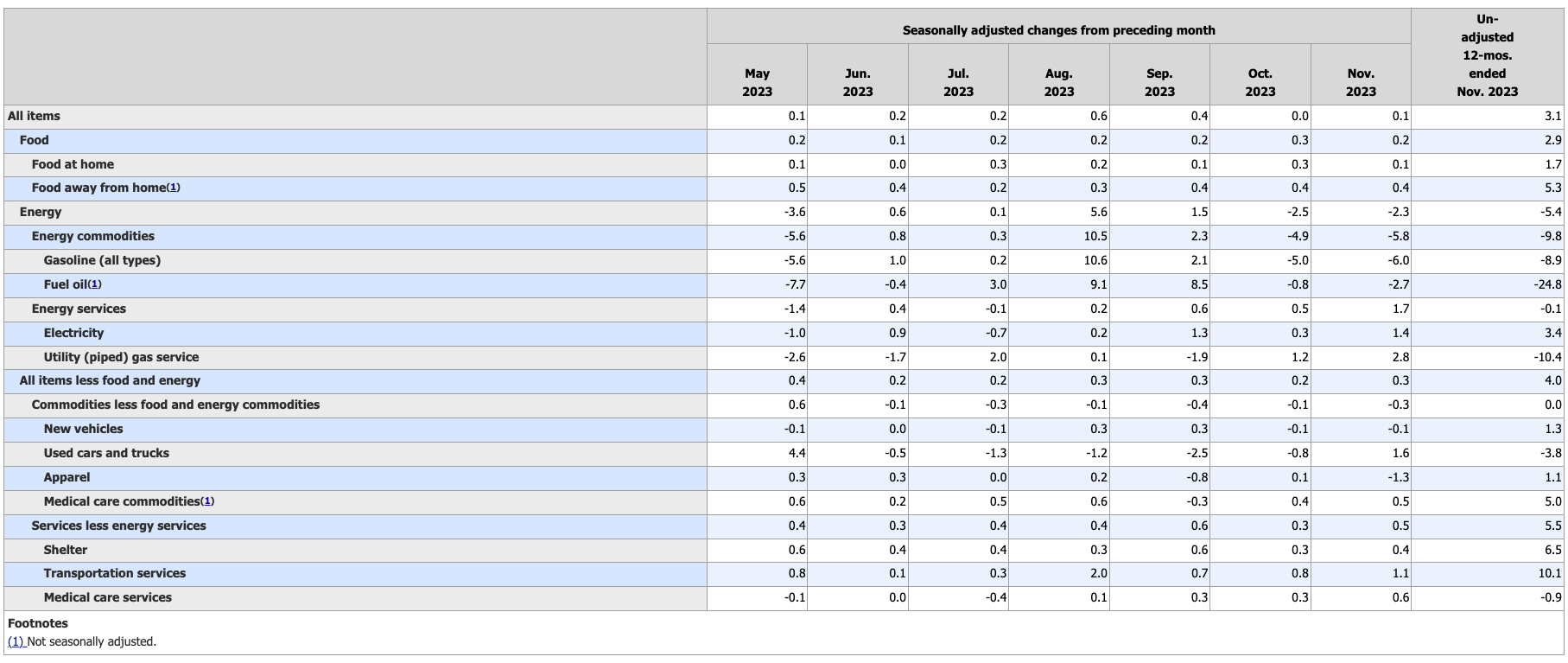

The only number that fell was the headline annual CPI. It dropped a tick from 3.2% in October to 3.1% in November, according to the latest Bureau of Labor Statistics data. Every other number indicated persistent, sticky price inflation.

Month on month, prices rose 0.1%. The expectation was for prices to remain flat as they did in October. The CPI ticked up despite another big dip in energy prices.

Stripping out more volatile food and energy prices, core CPI rose by 0.3%. That was up from 0.2% in November but in line with estimates. The annual core CPI was 4.0%, unchanged from the prior month.

Looking at the monthly increases so far in 2023 reveals that core CPI remains sticky. It rose by 0.4% in January, 0.5% in February, 0.4% in March, 0.4% in April, 0.4% in May, 0.2% in June and July, 0.3% in August and September, 0.2% in October, and 0.3 in November. That averages to 0.33% per month or 4.0% annually – still more than double the Fed’s 2% target.

In fact, core CPI has been hovering in the 4% range since July.

To put the monthly core CPI increase in perspective, it would need to average just under 0.17% to hit the 2% annual target.

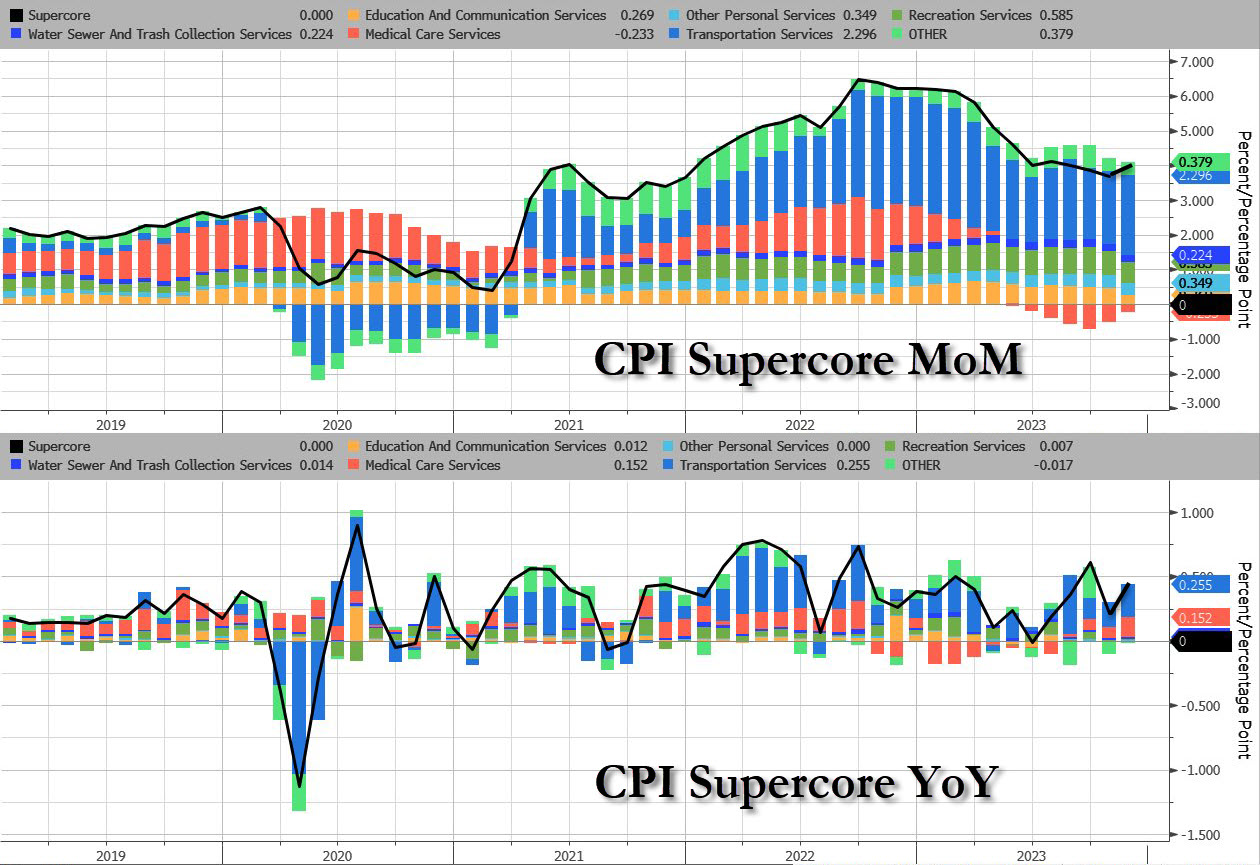

The report also showed a sudden uptick in “supercore” inflation – stripping out shelter costs along with food and energy.

Keep in mind, inflation is worse than the government data suggest. This CPI uses a formula that understates the actual rise in prices. Based on the formula used in the 1970s, CPI is closer to double the official numbers.

Even accepting the government data, every number remains well above the Fed’s 2% target.

Another big 2.3% month-on-month decline in energy prices helped push the overall CPI lower. Gasoline prices fell by 6% and fuel oil costs dropped 2.7%.

Price rose in most other categories.

Services (minus energy services) CPI charted a 0.5% increase on a monthly basis. That was up from 0.3% in October. The annual increase came in at 5.5% for the second straight month. Service prices are considered a leading indicator of future price inflation.

REACTION

As already noted, most mainstream headlines trumpeted the CPI report as another sign that price inflation is cooling.

Charles Schwab chief investment strategist Liz Ann Sonders told CNBC the Fed “will probably talk about continued disinflation being good news.”

President Biden said the CPI report showed “more progress” in bringing down inflation. Treasury Secretary Janet Yellen said she believes inflation is coming down “meaningfully.”

“I see no reason, on the path that we’re currently on, why inflation shouldn’t gradually decline to levels consistent” with the Federal Reserve’s 2% target,” she said.

Stock indexes were up and gold generally held steady, indicating market optimism that the report would not push the Fed to resume rate hikes,

But the latest CPI report did dampen optimism that the Federal Reserve would start cutting interest rates in March. After the data came out, traders pushed the likely start date for rate cuts to May 2024.

As Peter Schiff pointed out after the October CPI came out, core CPI remains double the Fed target of 2%, and he said nothing indicates we’re heading toward two.

Just because we’re at four now doesn’t mean we’re going to two. We could just as easily double and go back up to eight. There’s no reason to just conclude that that’s where we’re headed. But even at four, we’re still way above the Fed’s target of 2%.”

As already mentioned, the mainstream wants the Fed to claim victory over inflation so it can go back to inflationary policies. In effect, an end to rate increases, subsequent rate cuts, and loosening monetary policy will eventually lead to more price inflation. In other words, as soon as the Fed declares victory, inflation wins.

How?

Because rising prices are a symptom of monetary inflation. And monetary inflation is exactly what we will get when the central bank reverts to a looser monetary policy.

In fact, despite the rate hikes, the Fed hasn’t been nearly as aggressive in tightening monetary policy as you might think.

Jim Grant pointed out that the Chicago Fed’s Financial Conditions Index reveals financial conditions are still looser than average even after the Fed’s “short of zero to 60 in six seconds of rate increases.” As of the first week of December, the index stood at -0.46. A negative number indicates loose financial conditions.

This reinforces a point Schiff made in a post on X.

The Fed was far more aggressive when its goal was to raise the inflation rate up to 2% than it’s been to reduce the rate down to 2%. To raise the rate the Fed held interest rates at zero, the lowest rate in history. But to lower it the Fed stopped at a historically modest 5.5%.”

While recent CPI data may reflect a slowdown in rising prices and create a sense of optimism, the victory dance seems a bit premature.

Call 1-888-GOLD-160 and speak with a Precious Metals Specialist today!

Buka akaun dagangan patuh syariah anda di Weltrade.

Source link