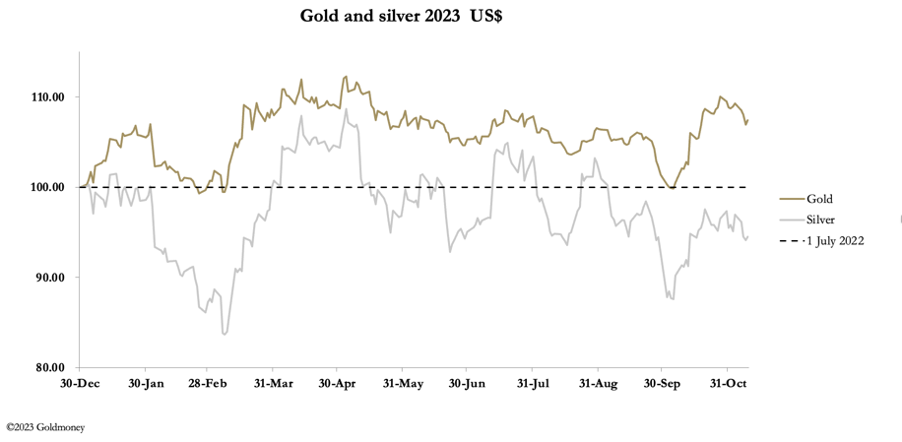

This week, gold and silver extended their correction of October’s sharp rise. In European trade this morning, gold was $1953, down $24 from Last Friday, and silver was $22.54, down 66 cents. Comex volume in both contracts was moderate.

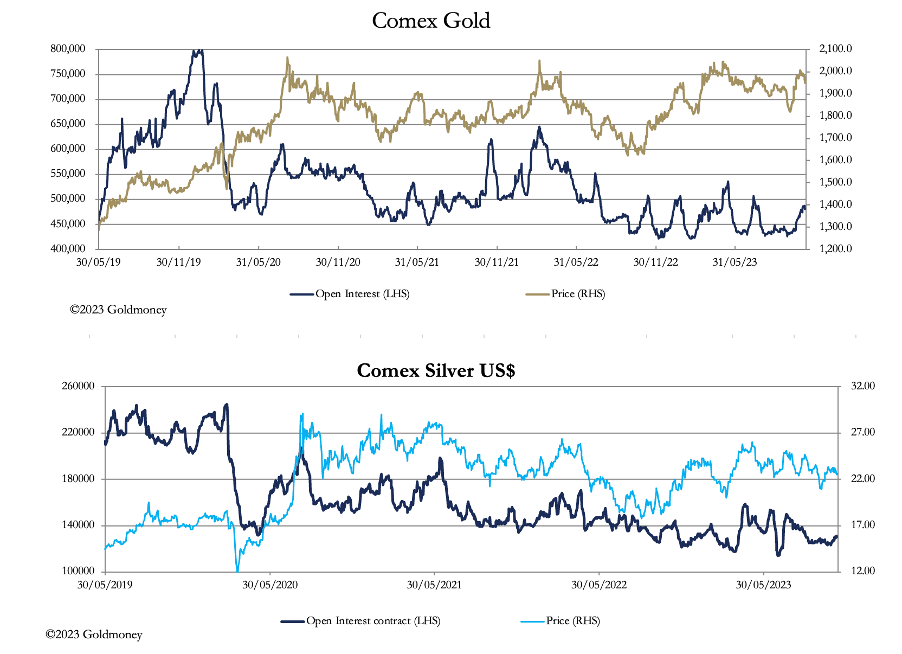

Open Interest in both Comex contracts has been on the low side for some considerable time, evidenced in the two charts below.

At the same time, prices have broadly maintained their levels represented by the widening visual gap between prices and Open Interest in the charts above.

Furthermore, gold’s technical chart below is immensely bullish.

Having tested the psychologically important $2000 level, gold has backed off requiring some further consolidation perhaps before another attempt. It could easily decline to test support at $1910—1925, which is where the two moving averages are presently. A move of that sort would certainly wash out weak paper bulls, creating the platform for the next move higher.

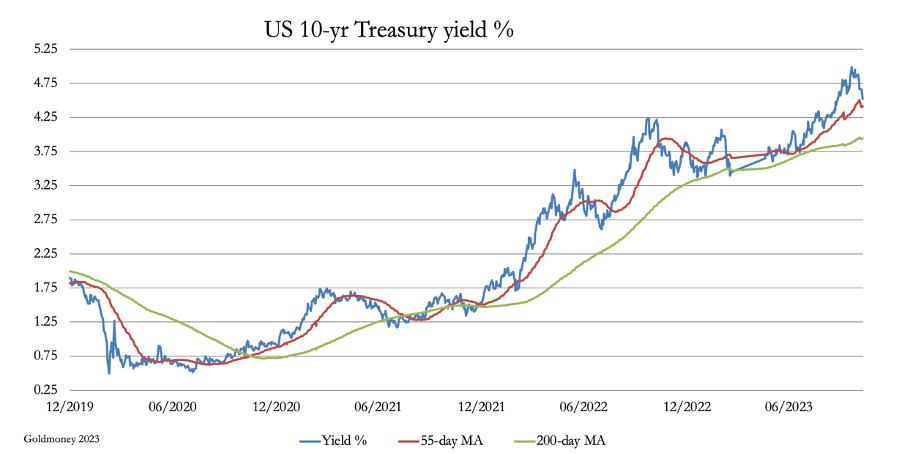

Interestingly, the recent decline in the gold price was accompanied by a decline in US Treasury yields, which is our next chart.

Technicals are one thing: fundamentals are another. To have the gold price and Treasury yields going in the same direction is a notable development. Until very recently, perceived wisdom was that falling bond yields was good for gold, and rising bond yields bad for it. That has now changed and can only reflect a change in market views on risk. Higher values for both are now consistent with systemic fears, reflected in concerns that higher interest rates and bond yields are destabilising for all forms of credit from currencies to bank deposits.

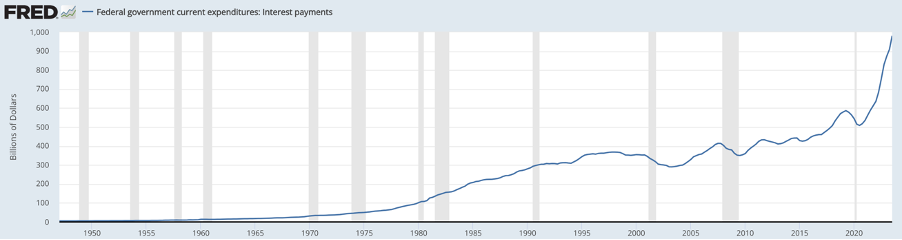

This being the case, we can understand the strong motivation for the authorities to suppress yields along the yield curve. The US Government’s budget deficit is soaring out of control, partly because of its spending plans, which traditionally increase during a presidential election year, and partly due to runaway debt funding costs. Take a look at the next chart:

Latest estimates are that federal government interest payments now exceed a trillion dollars in an accelerating trend. With a financially induced recession all but certain, the deadly combination of current and potentially higher funding costs, the refunding of $7.6 trillion maturing debt, lower tax receipts, and higher welfare costs could together push interest payments to $1.5 trillion this fiscal year. The question arises as to how all this debt is going to be funded at even current bond yields, let alone the higher yields otherwise expected to cover such a massive increase in government debt.

The US is not the only G7 nation with this problem. The only G7 member not in a debt trap is Germany. Japan with its government debt to GDP ratio of over 260% is acutely affected, and Japan along with China have been the largest foreign buyers of US Treasuries. They are now sellers because of their own problems and politics.

The Fed must be extremely concerned about all this, but a debt trap is a debt trap.

Buka akaun dagangan patuh syariah anda di Weltrade.

Source link