As was widely expected, the Federal Reserve Open Market Committee (FOMC) put rate hikes on pause at the June meeting, although it indicated we should expect additional hikes before the end of the year.

The question is how long with the pause last and will the next Fed move actually be a rate cut?

That likely depends on whether or not something breaks in the economy before the July meeting.

With the annual CPI increase coming in at the lowest level in over two years in May, the Fed had the cover it needed to put rate hikes on pause. But falling energy prices papered over sticky price inflation. If you look at the core CPI data, it’s clear the Fed hasn’t won the inflation fight.

How the central bank proceeds from here will depend on what happens over the next month.

On Pause For Now

At its June meeting, the FOMC “decided to maintain the target range for the federal funds rate at 5 to 5.25%.”

Holding the target range steady at this meeting allows the Committee to assess additional information and its implications for monetary policy.”

The vote was unanimous.

The official FOMC statement was virtually identical to May’s, and while the Fed put hikes on pause after 10 straight interest rate increases, there was no hint that the Fed intends to end the hiking cycle here.

As the committee did in May’s statement, it once again emphasized it will be “data dependent” moving forward.

In determining the extent of additional policy firming that may be appropriate to return inflation to 2 percent over time, the Committee will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments.”

Federal Reserve Chairman Jerome Powell reiterated this message during his press conference.

Nearly all committee participants expect that it will be appropriate to raise interest rates somewhat further by the end of the year. But at this meeting, considering how far and how fast we’ve moved, we judged it prudent to hold the target range steady. … The committee will take into account the cumulative tightening of monetary policy, the lags with which monetary policy effects economic activity and inflation, and economic and financial developments,”

The FOMC statement also once again asserted that “the Committee is strongly committed to returning inflation to its 2 percent objective.”

The problem is it’s a long way from achieving that goal. Even with the headline CPI number cooling significantly to 4% in May, it remains more than double that elusive target. And when you consider core inflation, the situation appears even worse.

The FOMC continues to claim that “the Committee will continue reducing its holdings of Treasury securities and agency debt and agency mortgage-backed securities, as described in its previously announced plans.”

The problem with this statement is that it hasn’t come anywhere near reducing its balance sheet according to the plan it announced a year ago. In fact, it has never reduced its holdings of mortgage-backed securities by its $35 billion per month target. Even if the central bank met its balance sheet reduction target, it would take more than seven years for it to unwind all of the quantitative easing that it did during the pandemic.

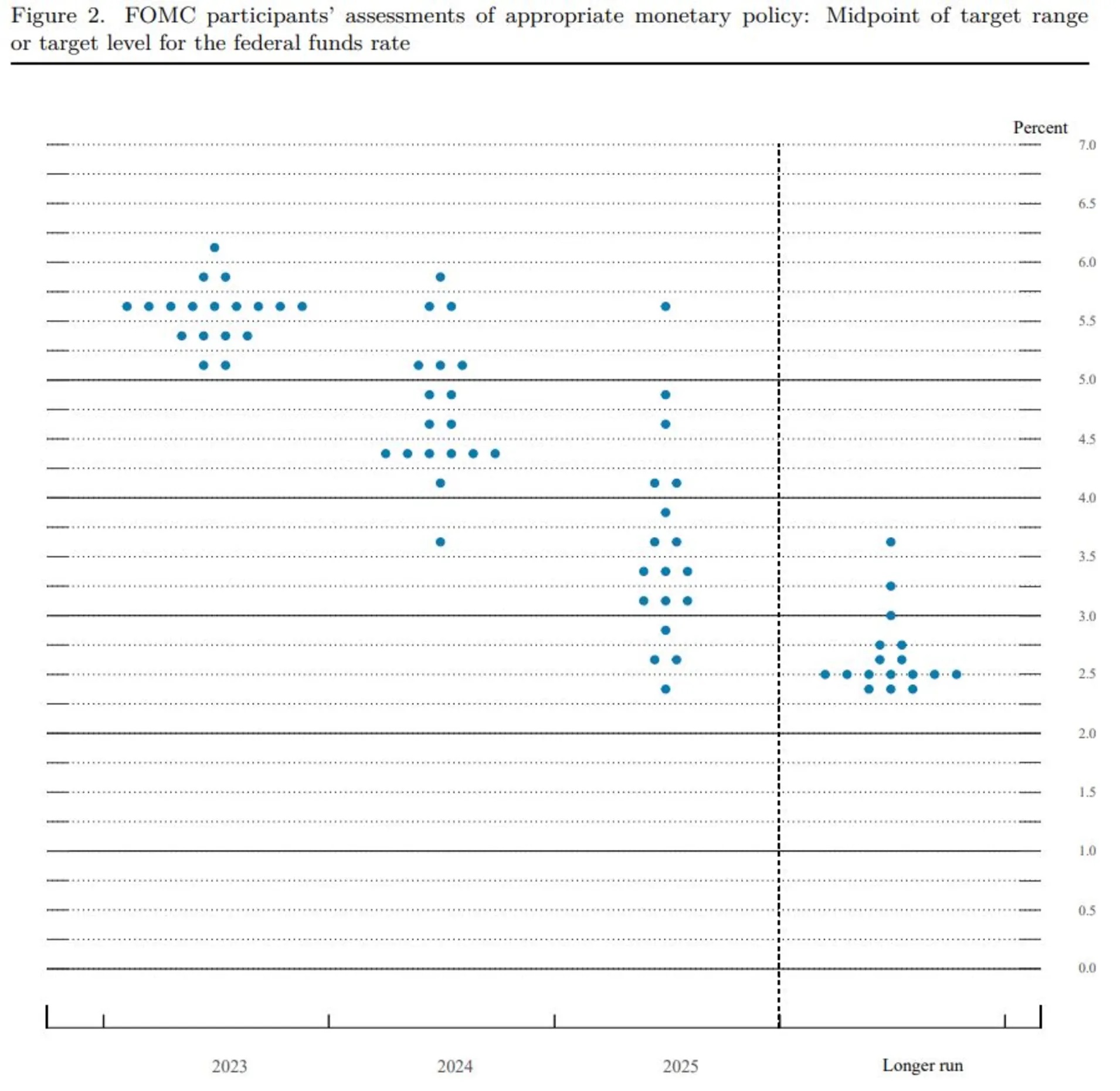

While the FOMC statement didn’t yield much new information, the FOMC also released a new “dot plot” projecting two more rate hikes before the end of the year. That was the thing that grabbed everybody’s attention and sent stocks plunging, along with gold and silver.

Four committee members projected one more rate hike in 2023. Nine members indicated they expect two. Two members projected a third hike, and the most hawkish member forecast four more rate increases this cycle. Two doveish members signaled that they don’t see any more hikes this year.

During the post-meeting press conference, Powell doubled down on the hawkishness, saying he doesn’t see rate cuts in the near future, and perhaps not for years.

It will be appropriate to cut rates at such time as inflation is coming down really significantly. And again, we’re talking about a couple of years out. As anyone can see, not a single person on the committee wrote down a rate cut this year, nor do I think it is at all likely to be appropriate.”

WHERE DO WE GO FROM HERE

The Fed is clearly trying to project a hawkish tone, but talk is cheap. And with price inflation still hot (despite mainstream reporting to the contrary) the Fed can’t plausibly declare victory.

But if the Fed was really that hawkish, why skip a rate hike?

The Fed is between a rock and a hard place, and I think they know it. They realize the economy can’t function much longer in this high interest rate environment. But I think they also feel obligated to keep fighting against price inflation. They can’t plausibly pivot now with CPI still running hot.

So how do the central bankers justify this pause?

They’re claiming that they need to pause and let the previous rate cuts take full effect. Powell said, “We’ve covered a lot of ground and the full effects of our tightening have yet to be felt.”

That’s probably true. It was months after the last hike before the financial crisis in 2008. So, we are going to eventually feel the impact of these rate hikes. But it’s not likely going to be in the form of lower price inflation. It’s going to come in as another financial crisis or major economic crash.

Interest rates are already at the highest levels since June 2006. The Feld held them there until Bernanke cut rates in September 2007 when home sales started to collapse. In other words, rates are at levels that set off the 2008 financial crisis and Great Recession. The difference is today we have even more debt and malinvestments in the economy. One has to wonder why anybody thinks things will turn out differently this time.

It must be wishful thinking.

The Federal Reserve has screwed up everything that is a function of interest rates. Rate hikes have already precipitated a financial crisis. Despite Fed’s insistence that “the US banking system is sound and resilient,” we’ve already witnessed three major bank failures. The Fed’s bank bailout papered over those problems and plugged that hole in the dam, but it’s only a matter of time before something else breaks. (Commercial real estate is a good candidate.)

Cuts are coming, no matter how tough Powell talks today, or what the rest of his crew put on a dot plot.

Ultimately, the Fed is going to reverse course and cut rates in order to keep banks from failing, stop the auto industry from imploding, save the housing market, prop up the government, bail out over-levered corporations, or try to reinflate whatever pops next in this bubble economy.

If things hold together until July, maybe we will see another rate hike. But the longer this plays out, the closer we get to rate cuts instead of rate hikes.

And that means even more price inflation is in your future.

No matter what Powell says, it’s only a matter of time before the Fed has to abandon the pretense of an inflation fight, pivot, and start cutting rates. Even if this tightening cycle brings down CPI in the next few months, it will only be temporary. The moment it is forced to reckon with the damage done by decades of easy money, it will return to easy money like a pig to mud — no matter what the central bankers are telling you today.

Call 1-888-GOLD-160 and speak with a Precious Metals Specialist today!

Buka akaun dagangan patuh syariah anda di Weltrade.

Source link