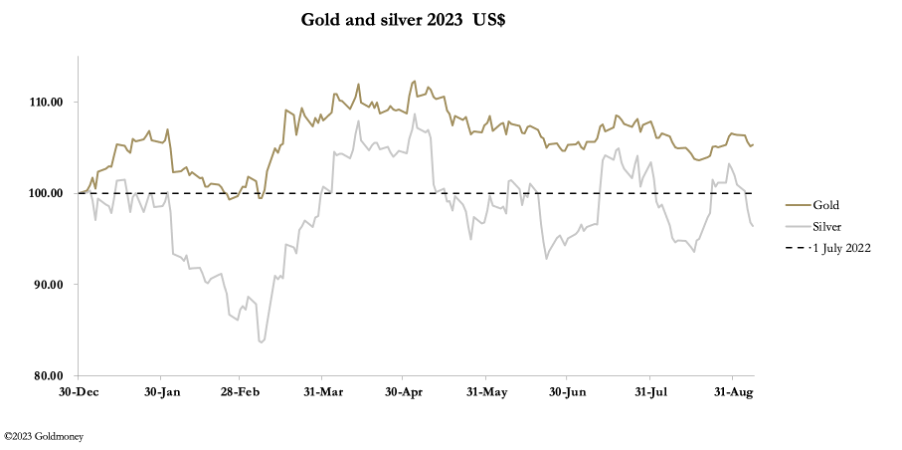

Gold and silver prices fell this week in light trade, with US markets closed on Monday for Labor Day. In European trade this morning, gold was at $1925, down $15 from last Friday’s close, and silver was at $23.05, down $1.10.

Holidays are the speculators’ enemy. Holding trading positions over a weekend is risky, let alone an extended one, such as occurred last weekend. They started to wind down their position last Wednesday, bringing silver prices perilously close to stops, making it simple for the Swaps on Comex to take them out with a few short sales.

Speculators do not generally appreciate that their trading behaviour is priceless information to market makers and bullion bank trading desks. They know that when the clients of Broker A or Broker B enter the market how skittish they are likely to be. They will have assessed the quality of speculative buying on the previous rally and acted accordingly. Clearly motivated by their underlying bullishness, commentators with little or no skin in the trading game were reading the charts and saying that silver was going to the moon. It is this that creates profitable opportunities for market makers.

On 15 August, when the silver price bottomed at $22.25, the Managed Money category on Comex was net short 6,670 contracts, worth $742,037,500. By 29 August, they had been whipsawed into losses, and went net long 16,479 contracts worth $2,035,156,500. They were whipsawed again, with the price crashing to $22.86 at one point yesterday. The extent of their collective losses on this third swing will be indicated in the Commitment of Traders figures due to be released shortly.

It is the collective stupidity of speculators which has led to them being fleeced so badly. This point being made, silver’s technical position has been improved significantly, giving grounds for expecting a subsequent rally to be better founded now that the idiot brigade has been shaken out.

Gold’s moves have been more subdued. Partly, this is due to a lower level of speculation in the Comex contract, coupled with low bullion liquidity. And Open Interest, the best general indicator of speculator interest overall remains historically low as shown in the next chart.

Scaring speculators away is the resilience of the dollar, and the stubbornness of bond yields, illustrated in the next two charts.

While everyone expects a recession and therefore a lessening of CPI inflation and a return to lower interest rates, this does not appear to be happening. Dispassionate readings of the two charts above strongly suggest that the dollar is consolidating earlier declines, and that the yield on the 10-year UST is going significantly higher. But timing is of the essence.

There is little doubt that higher bond yields will intensify problems for the banks. The next chart shows the extent to which banks with bond losses are seeking cover from the Fed’s Bank Term Funding Programme, set up to prevent banks going under due to mark-to-market losses.

At $108bn, it is still rising…

Buka akaun dagangan patuh syariah anda di Weltrade.

Source link