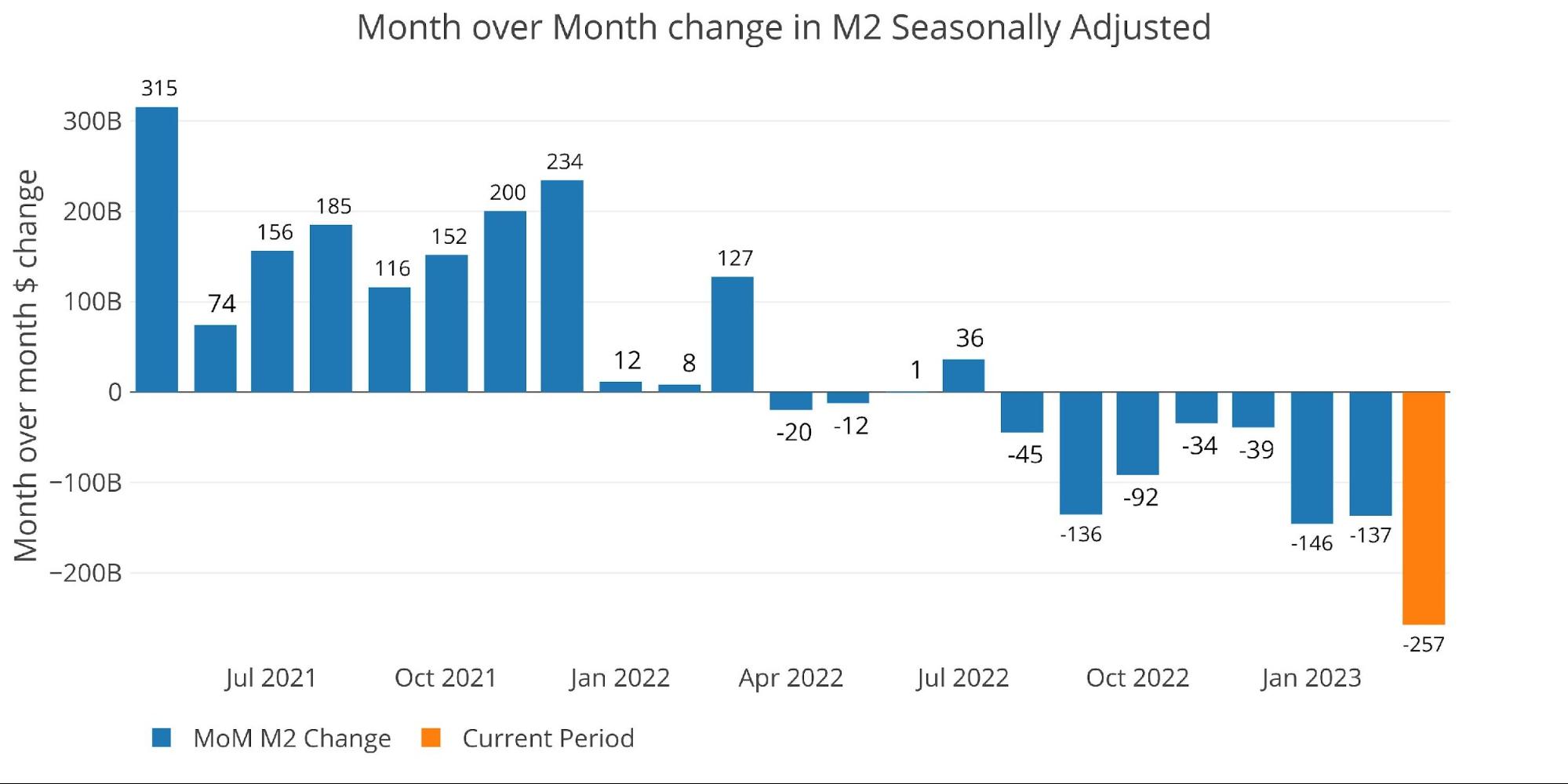

Seasonally Adjusted Money Supply in March fell $257B. As the chart below shows, this is now the 8th consecutive monthly drop. Going back to the 1970s, the drop in March was actually the biggest on record from an absolute and relative basis.

Figure: 1 MoM M2 Change (Seasonally Adjusted)

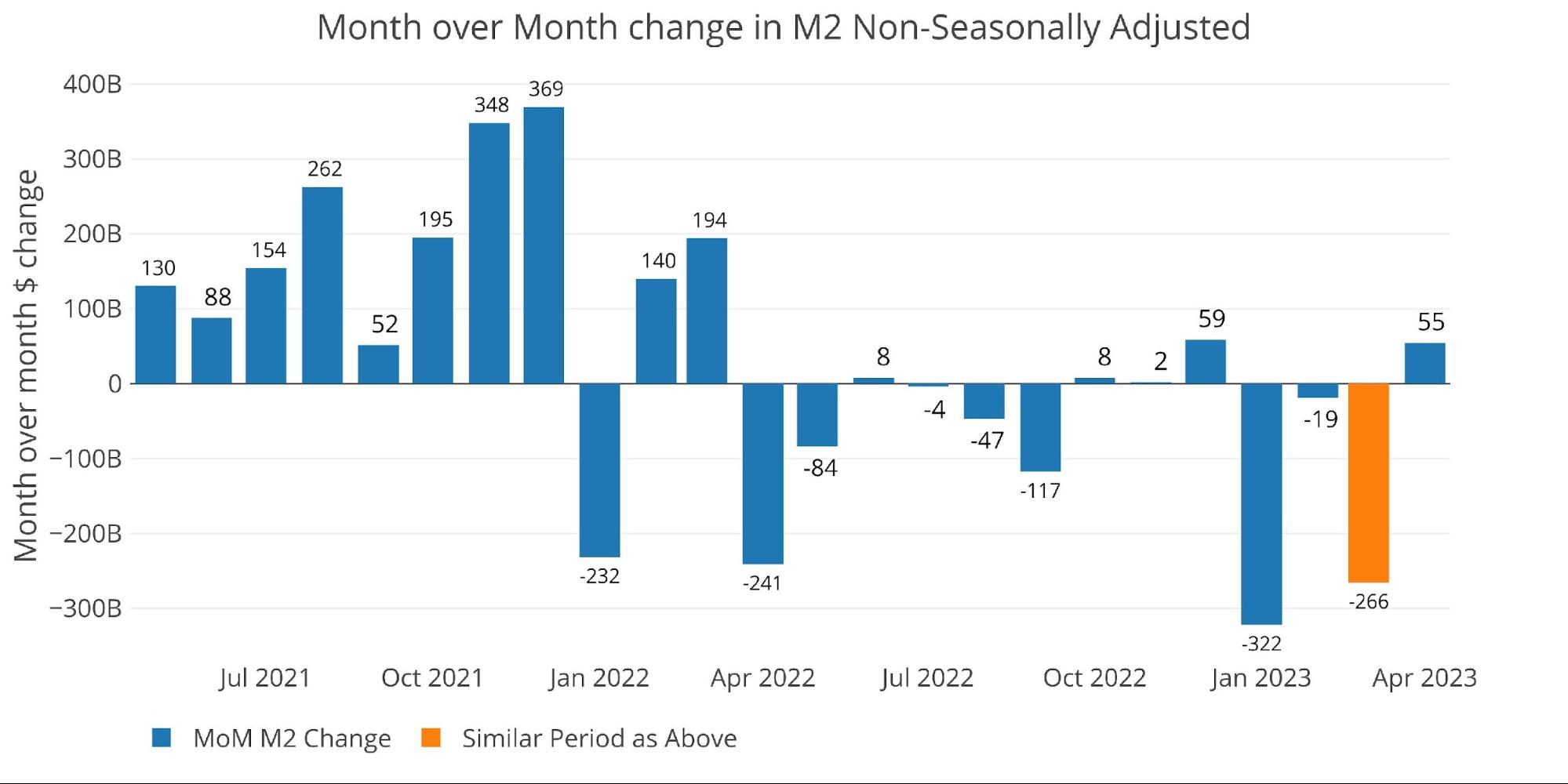

Below are the unadjusted raw numbers which are slightly ahead of the adjusted numbers. The orange bar aligns with the same time period as the orange bar above. March came in as a drop of $266B which is very close to the adjusted number. April is only showing one week so far but is positive by $55B. Based on the current trend, this will likely turn negative by the time April data is complete.

Figure: 2 MoM M2 Change (Non-Seasonally Adjusted)

Looking at the seasonally adjusted numbers shows that this month decreased the Money Supply by an incredible -13.7% annualized which is well below both the 6-month and 12-month trend (-6.4% and -4.1% respectively).

Figure: 3 M2 Growth Rates

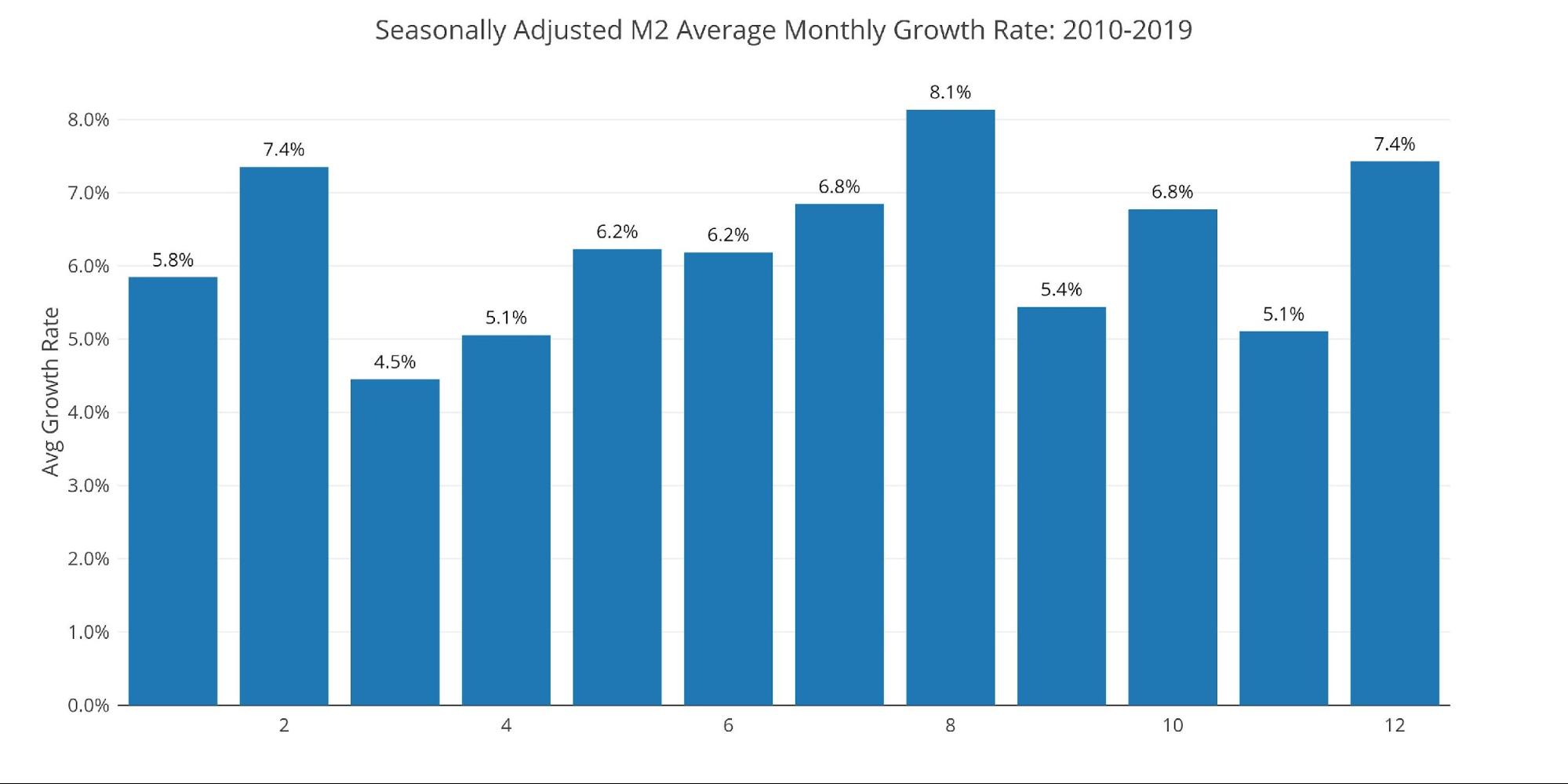

The average for March (pre-Covid) was 4.5%, which means this month was below the average by an incredible 1820 bps!

Figure: 4 Average Monthly Growth Rates

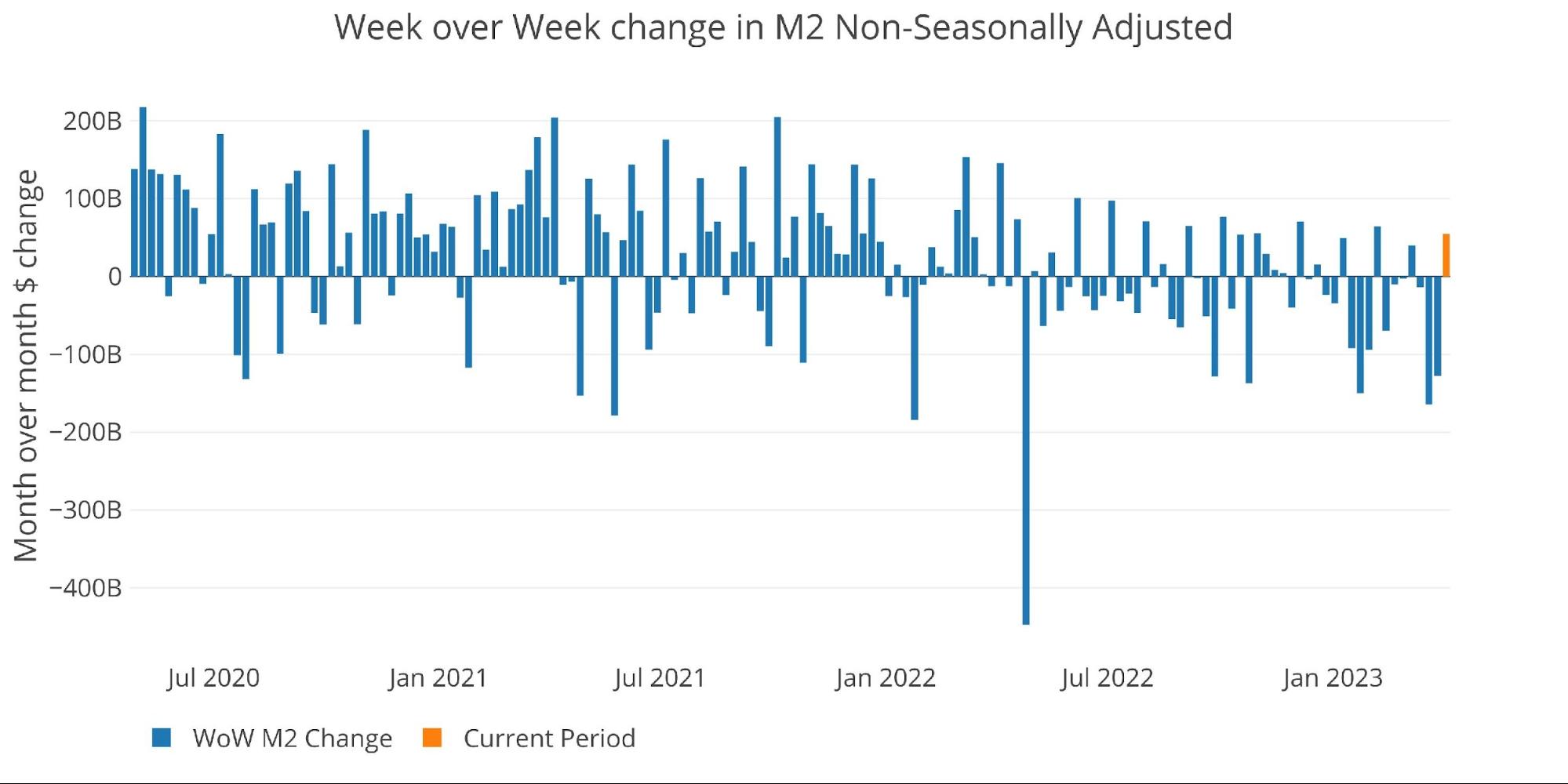

The Fed only offers weekly data that is not seasonally adjusted. As the chart below shows, there is a clear trend of the weekly increases being smaller (when they occur) and the weekly decreases being more frequent and much larger on average.

Figure: 5 WoW M2 Change

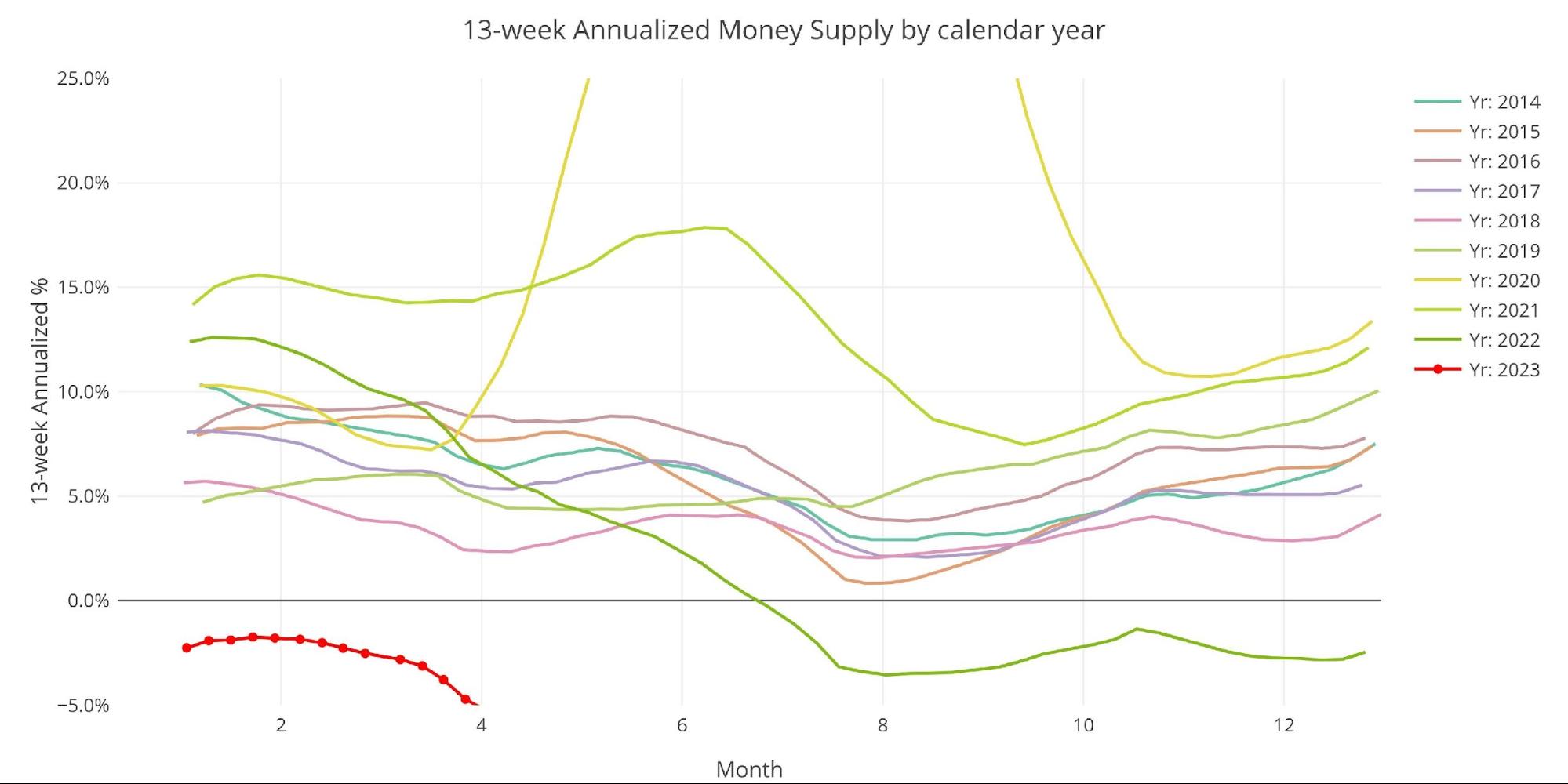

The “Wenzel” 13-week Money Supply

The late Robert Wenzel of Economic Policy Journal used a modified calculation to track Money Supply. He used a trailing 13-week average growth rate annualized as defined in his book The Fed Flunks. He specifically used the weekly data that was not seasonally adjusted. His analogy was that in order to know what to wear outside, he wants to know the current weather, not temperatures that have been averaged throughout the year.

The objective of the 13-week average is to smooth some of the choppy data without bringing in too much history that could blind someone from seeing what’s in front of them. The 13-week average growth rate can be seen in the table below. Decelerating trends are in red and accelerating trends in green.

The 13-week average has now reached a new all-time low of -5.37%. This is lower than what occurred last August when 13-week Money Supply had crashed to its lowest point ever. That move bottomed at -2.83% while the current down move is at the beginning of the seasonal move down.

Figure: 6 WoW Trailing 13-week Average Money Supply Growth

The plot below really helps show the seasonality of the Money Supply. As noted above, this is the time of year when Money Supply starts to trend lower. If Money Supply is only at the beginning of the current move down then this could mean hitting 13-week rates that were unthinkable only 18 months ago.

The current rate is already an incredible divergence from history, so any further move down will only make matters worse.

Figure: 7 Yearly 13-week Overlay

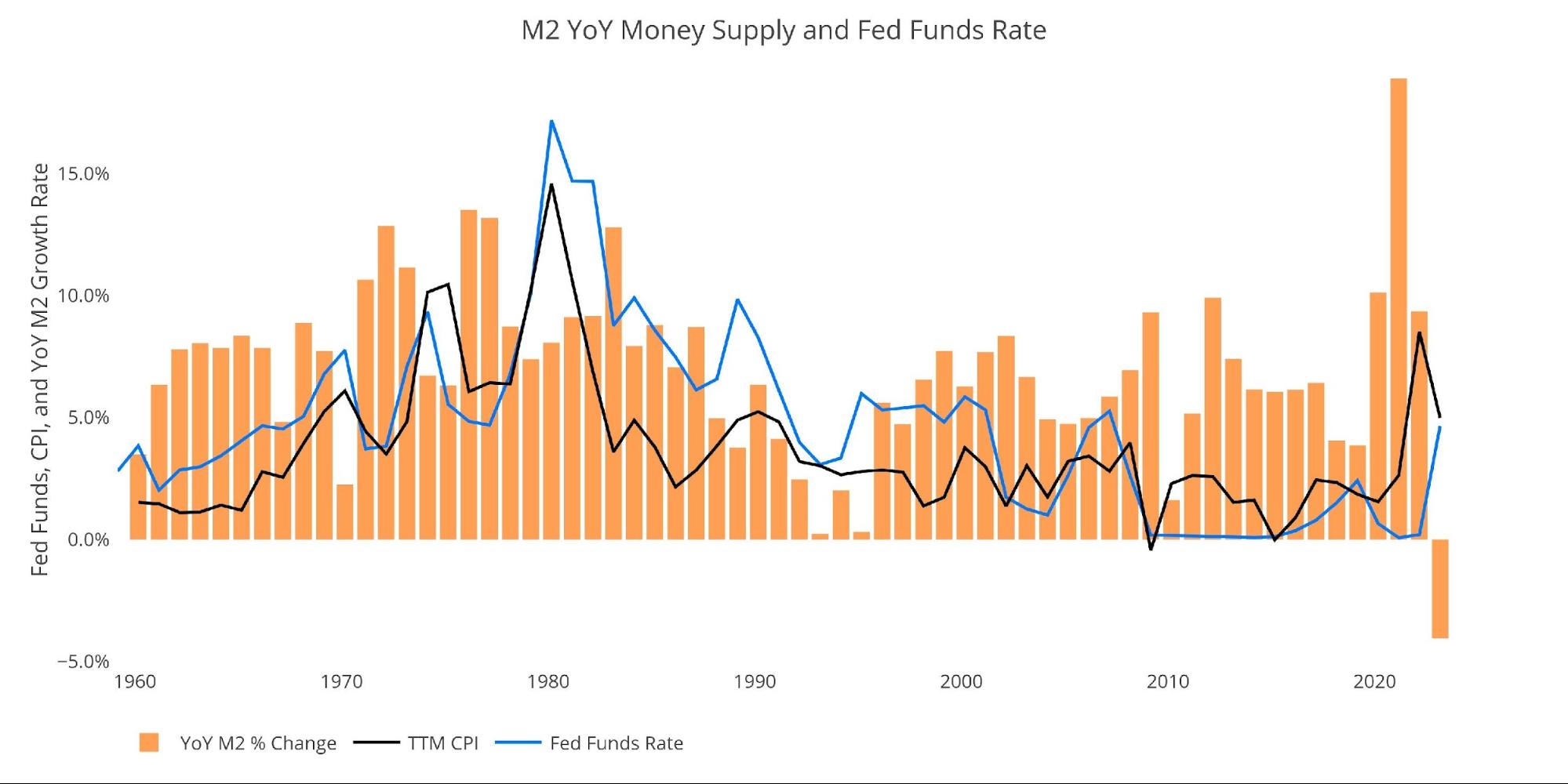

Behind the Inflation Curve

Incredibly, even with the contracting Money Supply, the Fed is still not doing enough to solve the inflation problem. This is due to how much money was created over the last few years. Undoing this money creation will require an even bigger drop in Money Supply in the months ahead.

Unfortunately, the Fed does not have that much time. The economy is already struggling big time with the banking crisis and the unfolding real-estate crisis. First Republic is already back in the news, requiring a bailout to survive. This just shows how the economy needs new money to be pumped in sooner rather than later or the reckoning will be epic. In fact, the Fed has probably already passed the point of no return and it’s simply a matter of time before something major breaks that the government cannot “fix” over a weekend.

Figure: 8 YoY M2 Change with CPI and Fed Funds

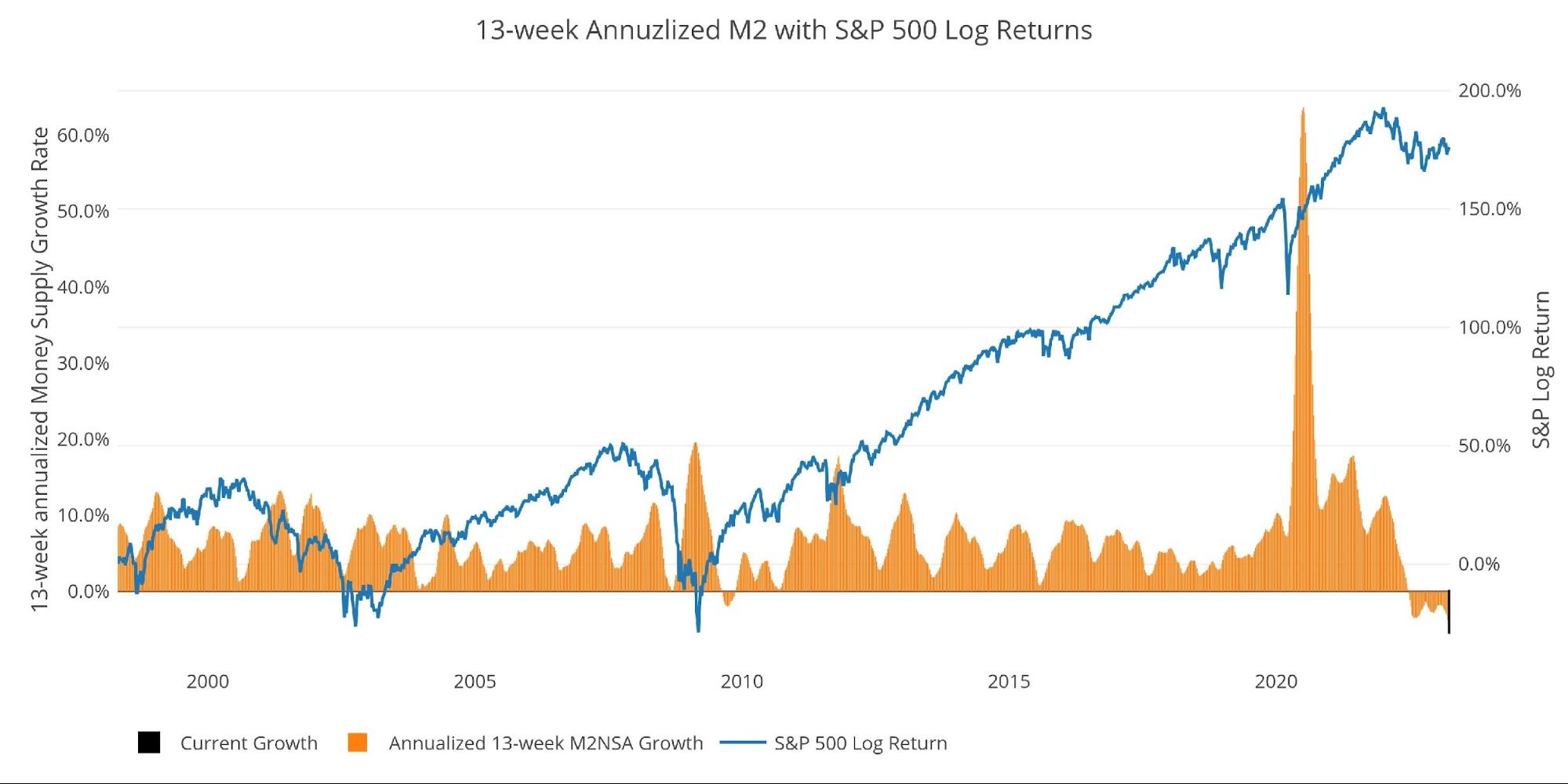

Historical Perspective

The charts below are designed to put the current trends into historical perspective. The orange bars represent annualized percentage change rather than raw dollar amount. The current slowdown can be seen clearly on the right side.

The Money Supply slowdown is a major driver of the weakness seen in the stock market over the last year. The massive increase seen in 2020 is what pushed the market to explode higher. The stock market has been out of fuel for months which is why the major indices remain choppy.

Figure: 9 M2 with Growth Rate

Taking a historical look at the 13-week annualized average also shows the current predicament. This chart overlays the log return of the S&P. Mr. Wenzel proposed that large drops in Money Supply could be a sign of stock market pullbacks. His theory, derived from Murray Rothbard, states that when the market experiences a shrinking growth rate of Money Supply (or even negative) it can create liquidity issues in the stock market, leading to a sell off.

While not a perfect predictive tool, many of the dips in Money Supply precede market dips. Specifically, the major dips in 2002 and 2008 from +10% down to 0%. The economy is now grappling with a peak growth rate of 63.7% in July 2020 down to more than 9.5 months of negative growth rates.

Given the current drop in Money Supply, it’s incredible the stock market has not been under more pressure. This could be from the fact that everyone is still waiting for the Fed pivot to rescue the market. Unfortunately, enough damage has been done that even a hard pivot from the Fed will be unlikely to do much to save the economy and stock market.

Please note the chart only shows market data through April 3rd to align with available M2 data.

Figure: 10 13-week M2 Annualized and S&P 500

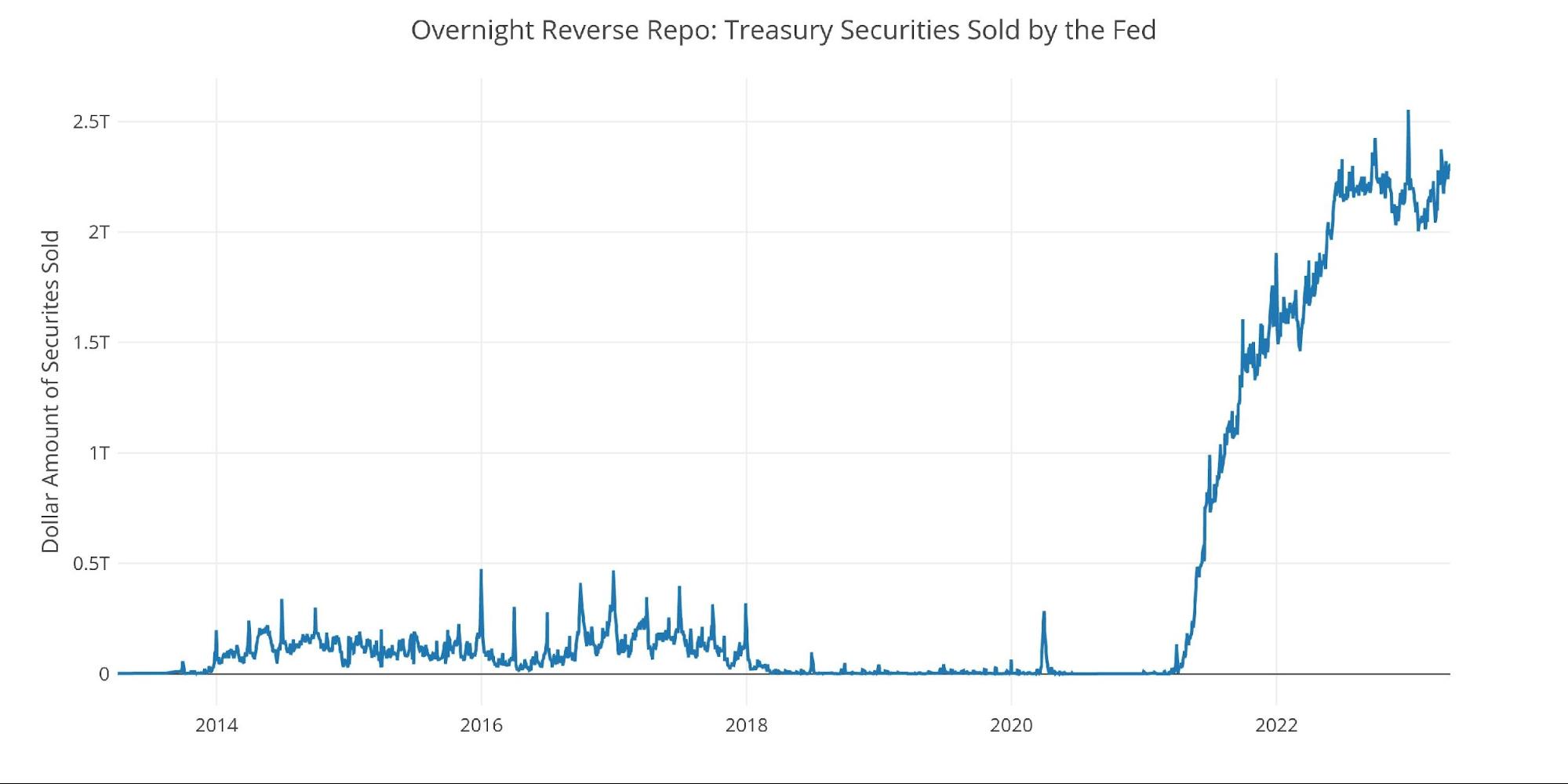

One other consideration is the massive buildup in the reverse repo market at the Fed. This is a tool that allows financial institutions to swap cash for instruments on the Fed balance sheet.

Current Reverse Repos peaked at $2.55T on Dec 30. This broke the previous record from September. The value typically tops out at the quarter end. This past March 31st, the value topped out at $2.37T which was a bit shy of the December record.

Figure: 11 Fed Reverse Repurchase Agreements

Wrapping Up

The 13-week annualized Money Supply has been screaming for some time that something is going to break. The value continues to move down suggesting things are only getting worse. Things have already broken (Crypto last year, banks this year), but the worst is definitely yet to come. The First Republic rescue being contemplated is just the next domino. More will fall in the months ahead.

It takes time for these things to develop. It happens slowly at first and then gains momentum. Looking back to 2008, there was a full 6 months between Bear Stearns and Lehman. The Fed has moved so quickly that the malinvestment in the economy has not yet been brought to light. Make no mistake, it will!

The economy is built on cheap credit and easy money. That easy money is now gone and the Money Supply is in free-fall. Something will break and the Fed will then need to reverse the recent fall in Money Supply that has occurred. This likely means a bigger increase than what was seen during Covid. Unfortunately, it won’t be enough to rescue the economy but it will be enough to blast inflation to new highs and potentially destroy the dollar. When that happens, it’s likely gold will return as the global reserve currency as it always has throughout human history.

Data Source: https://fred.stlouisfed.org/series/M2SL and also series WM2NS and RRPONTSYD. Historical data changes over time so numbers of future articles may not match exactly. M1 is not used because the calculation was recently changed and backdated to March 2020, distorting the graph.

Data Updated: Monthly on fourth Tuesday of the month on 3-week lag

Most recent data: Apr 03, 2023

Interactive charts and graphs can always be found on the Exploring Finance dashboard: https://exploringfinance.shinyapps.io/USDebt/

Call 1-888-GOLD-160 and speak with a Precious Metals Specialist today!

Buka akaun dagangan patuh syariah anda di Weltrade.

Source link