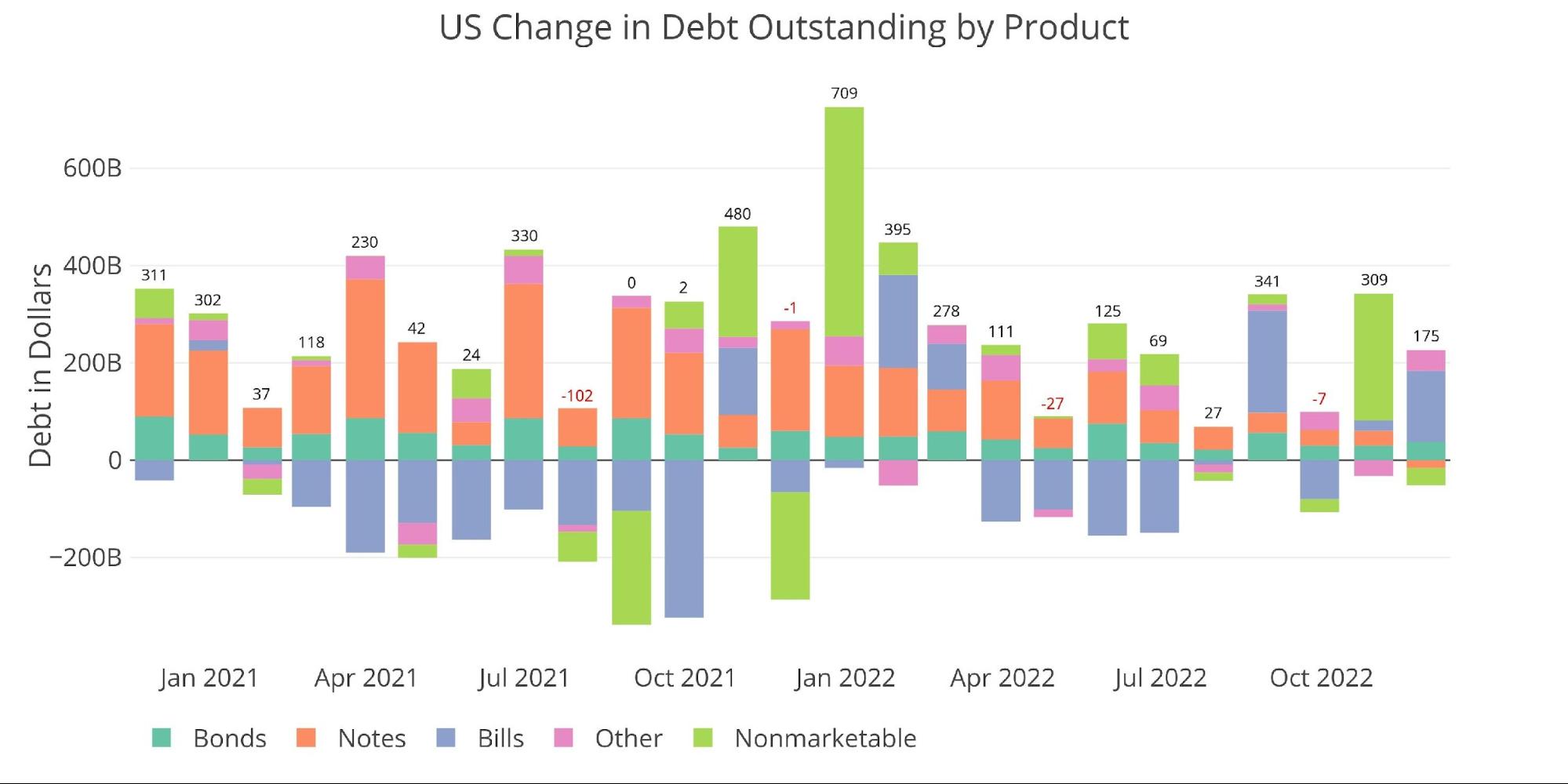

The Treasury added $175B in new debt during November, hitting the debt ceiling of $31.4T. New debt issuance was focused on the short end of the curve with $145B in Treasury Bills issued.

As is typically the case when the debt ceiling is hit, the Treasury starts pulling from Non-Marketable debt to cover additional expenses. They pulled $35B out of Non-Marketable, which is likely just a start. The last two debt ceilings saw Non-Marketable, specifically government employee retirement accounts, fall by over $220B.

Note: Non-Marketable consists almost entirely of debt the government owes to itself (e.g., debt owed to Social Security or public retirement)

Figure: 1 Month Over Month change in Debt

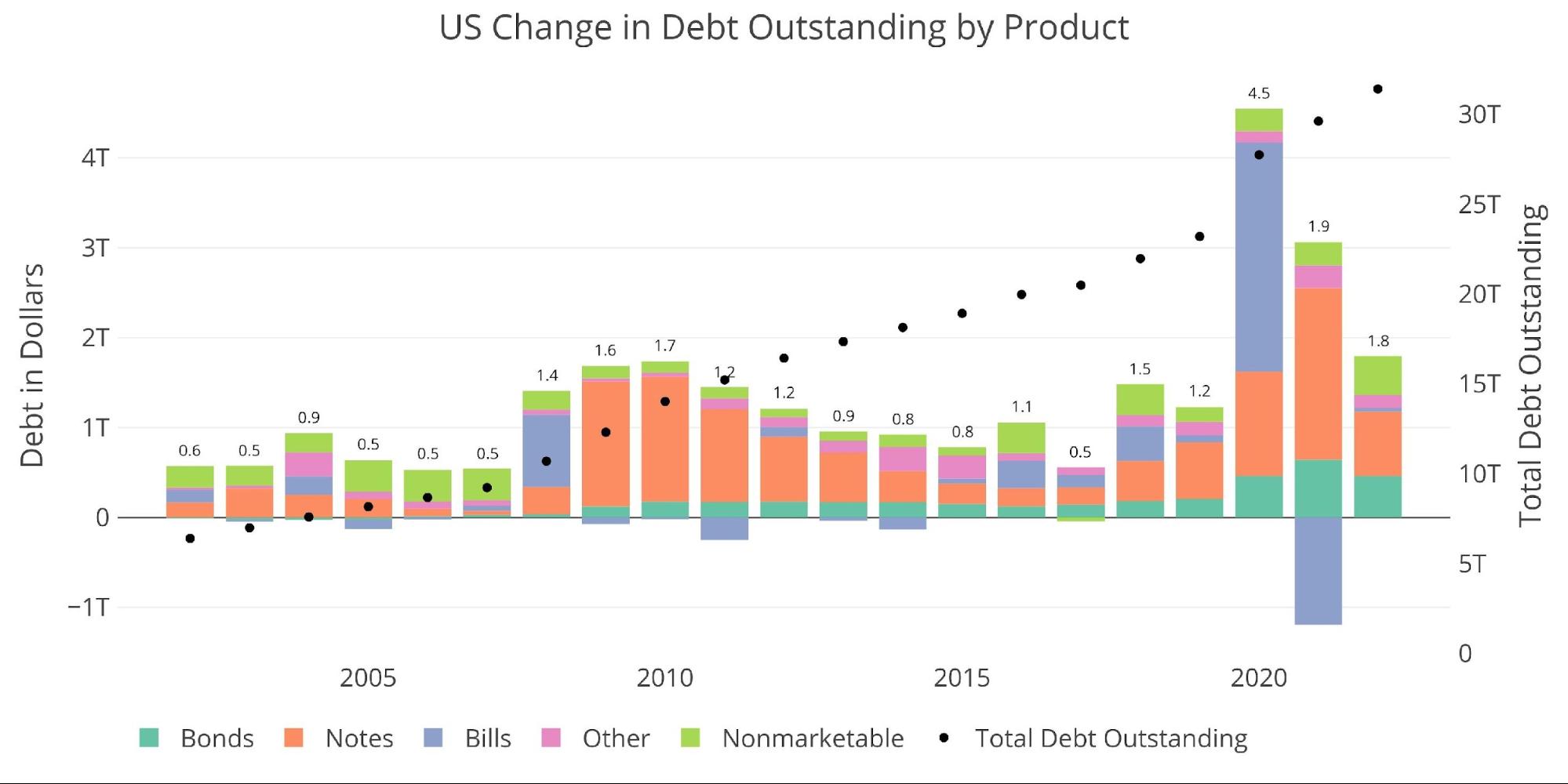

YTD the Treasury has added $1.8T in new debt in 2022 despite record-high tax revenues. With one month still to go, the total debt has already exceeded all other years before Covid.

Figure: 2 Year Over Year change in Debt

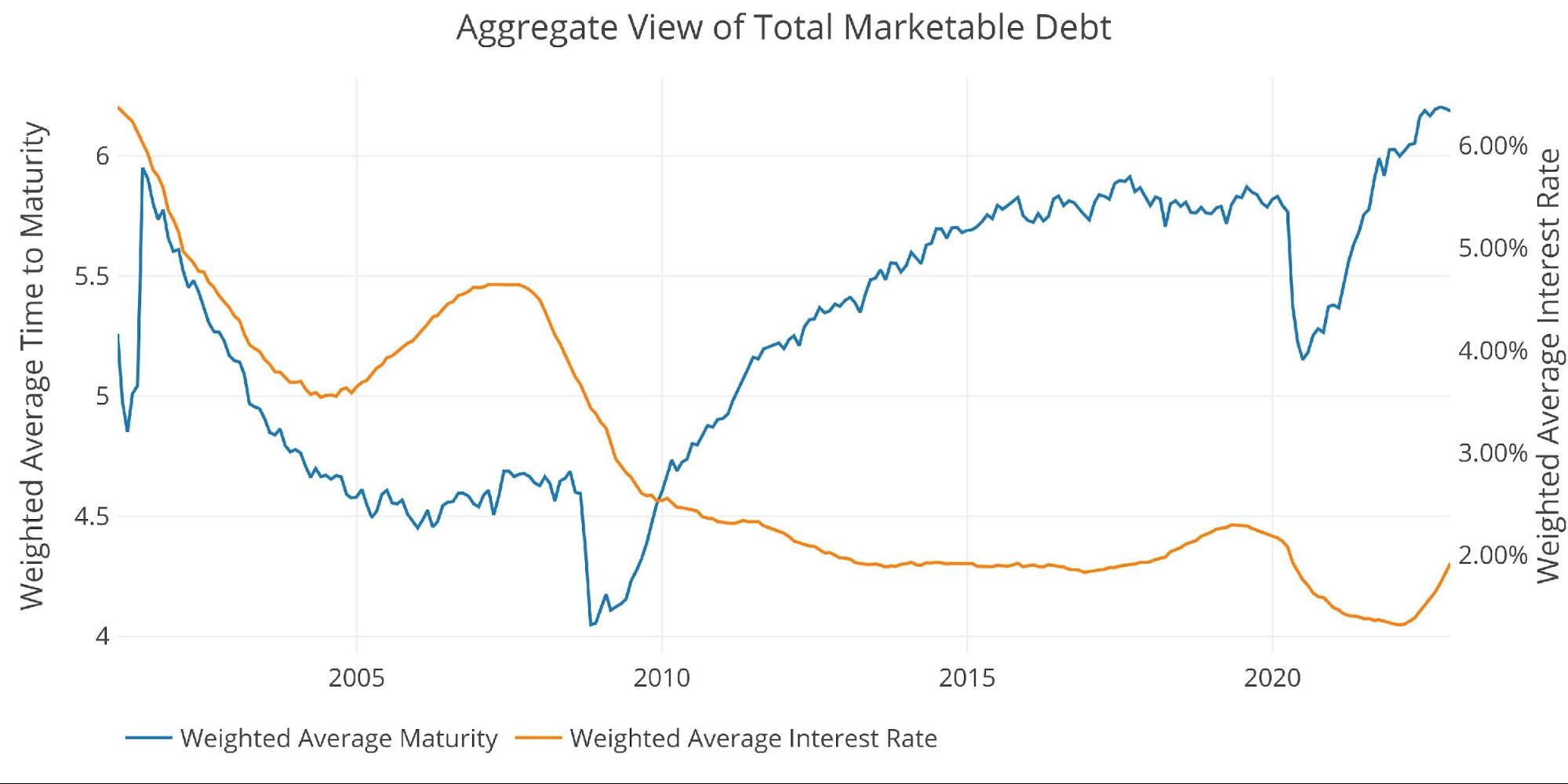

The chart below shows the impact of the current rise in interest rates, and the steps by the Treasury to prepare for such an event. Weighted average interest is at 1.92%, up 60bps from February of this year and 10bps from last month.

To try and extend the maturity of the curve, the Treasury did a massive conversion of short-term debt into long-term debt last year. That pushed the average maturity of the debt to 6.2 years.

Figure: 3 Weighted Averages

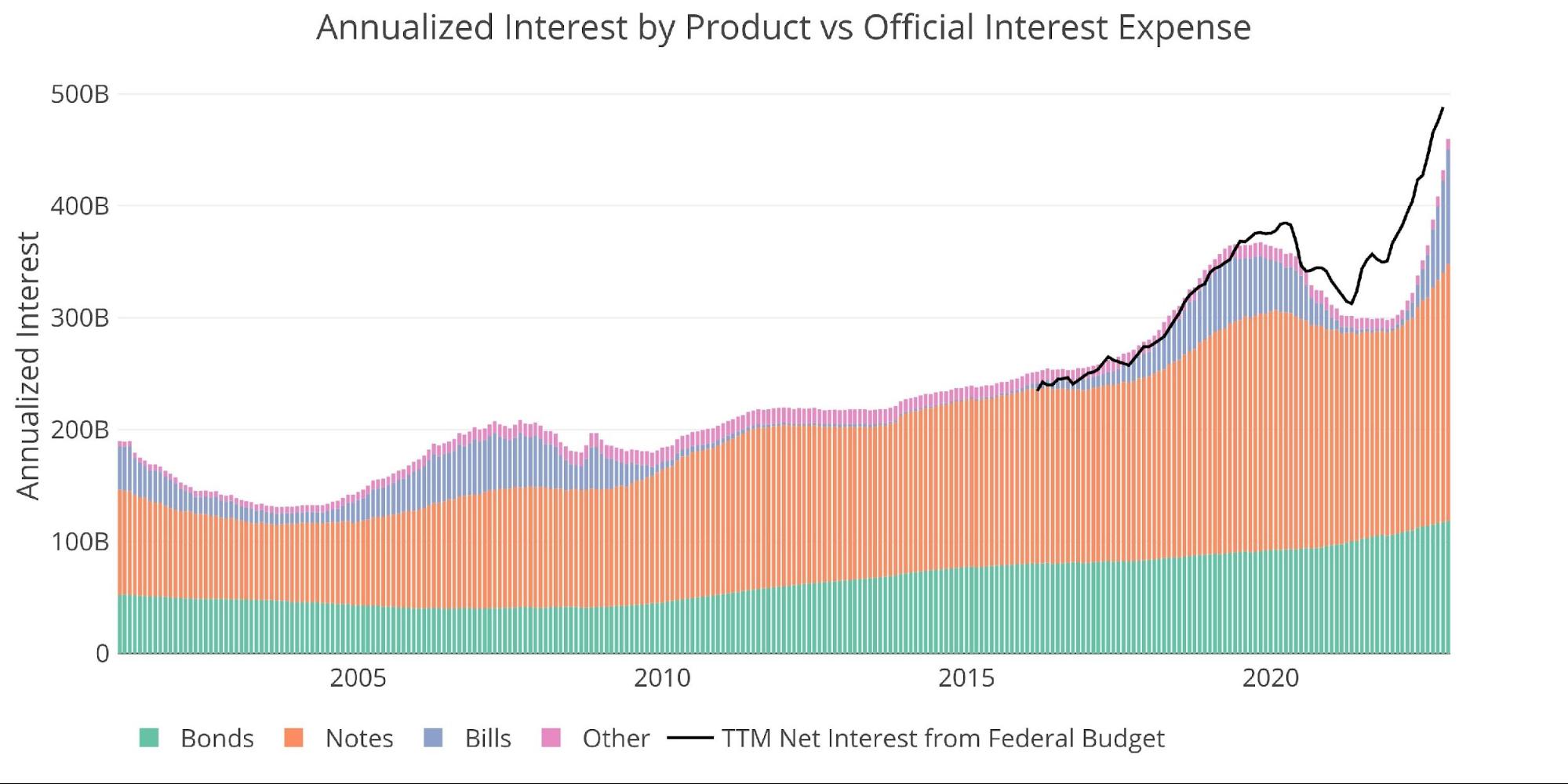

The Fed continues to talk a tough game about battling inflation, but the situation for the Treasury is getting uglier each month. The interest on bonds has been on a slow steady increase for years as the balance has grown. For Notes and especially Bills, the chart shows a dramatic spike in recent months that is completely unsustainable.

Figure: 4 Net Interest Expense

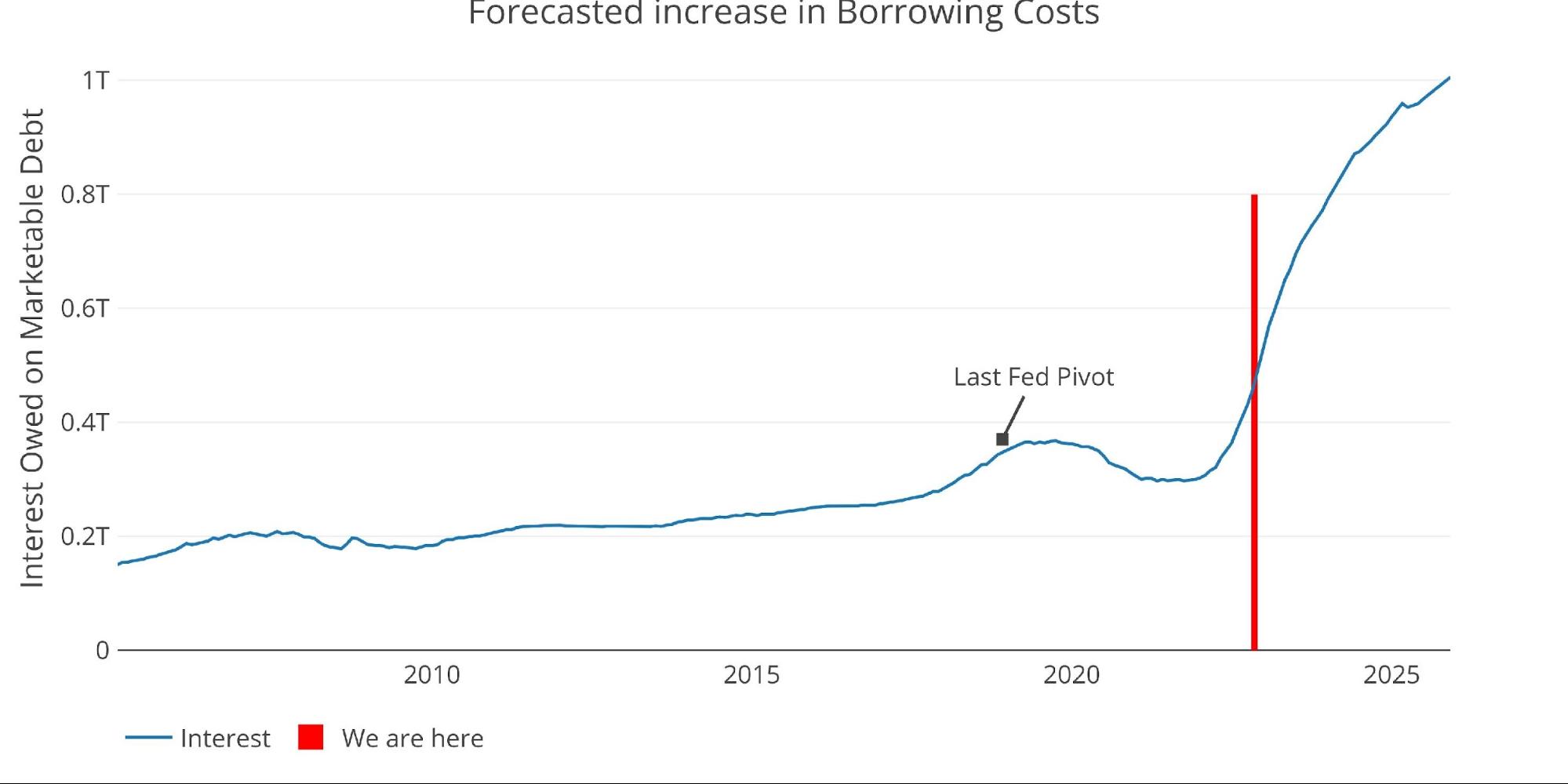

The chart below shows the gravity of the situation. In the latest month, annualized interest on marketable debt is at $459B, up $28B in the last month alone. Despite this massive run-up, the trajectory is still looking dramatically worse as existing debt is rolled over. By March, annualized interest is set to be $600B, reaching almost $700B by July.

This means that on the current path, the Treasury will owe an extra $200B a year in interest within just 8 months!

Please note: for simplicity, this model assumes the same (conservative) level of interest rate for all securities. It also only looks at Marketable debt and assumes $1.5T a year in new debt, which is less than the current year, and does not consider increased spending and lower tax revenues from a recession.

Figure: 5 Projected Net Interest Expense

The annualized interest is surging because so much debt needs to roll over at much higher rates. The chart below shows how much debt is rolling over (~$1T per month). Much of this is short-term debt, hence the steep drop-off in the light green bars, but each time the Fed raises rates, the impact on the Treasury is nearly immediate. This can be seen by the massive spike in short-term interest owed in the chart above.

Figure: 6 Monthly Rollover

Note “Net Change in Debt” is the difference between Debt Issued and Debt Matured. This means when positive it is part of Debt Issued and when negative it represents Debt Matured

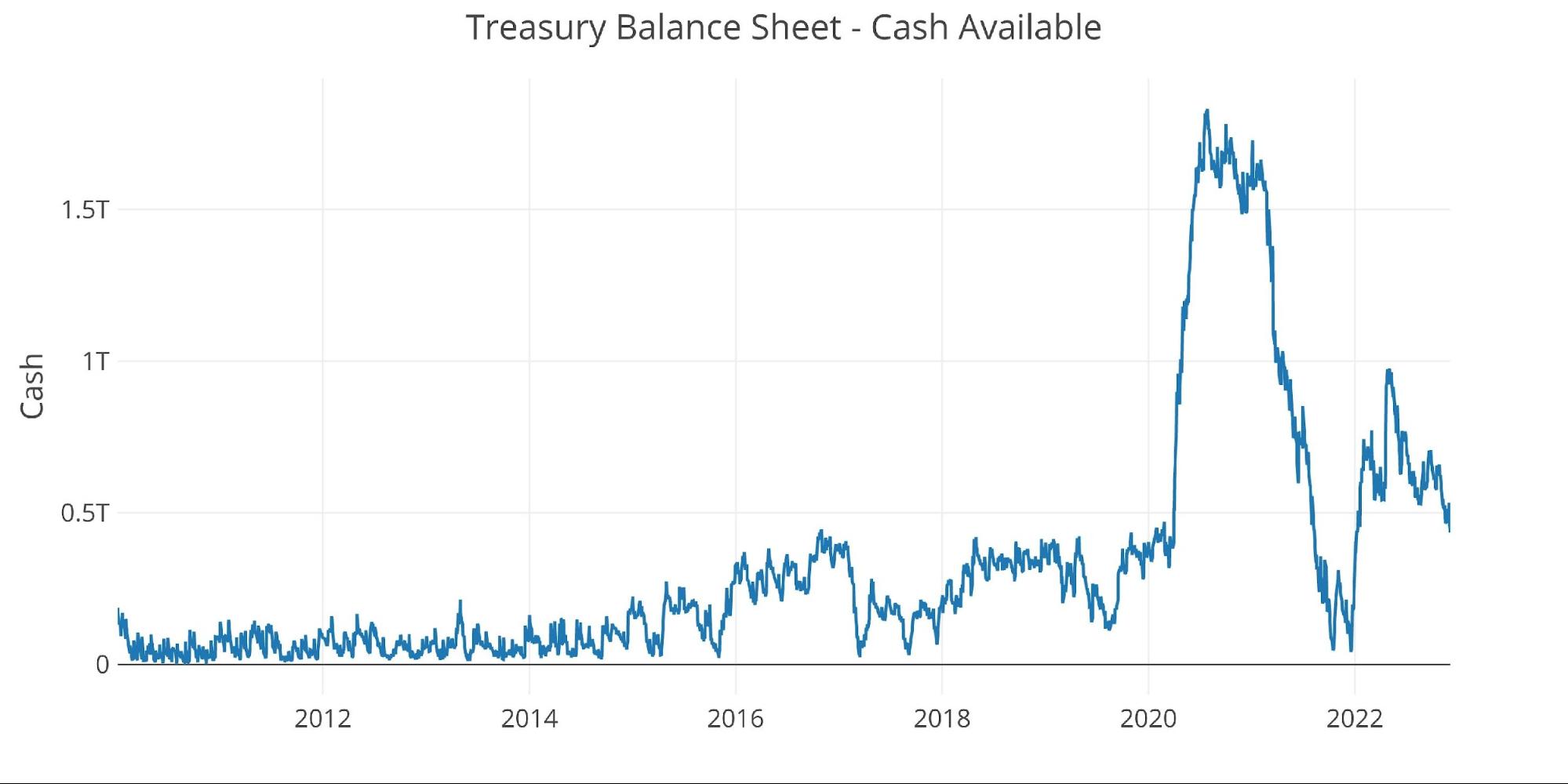

The current debt ceiling saga will likely come to a quicker conclusion given the elections are now behind the politicians. The Treasury has let its cash balance drop to under $500B.

Figure: 7 Treasury Cash Balance

Digging into the Debt

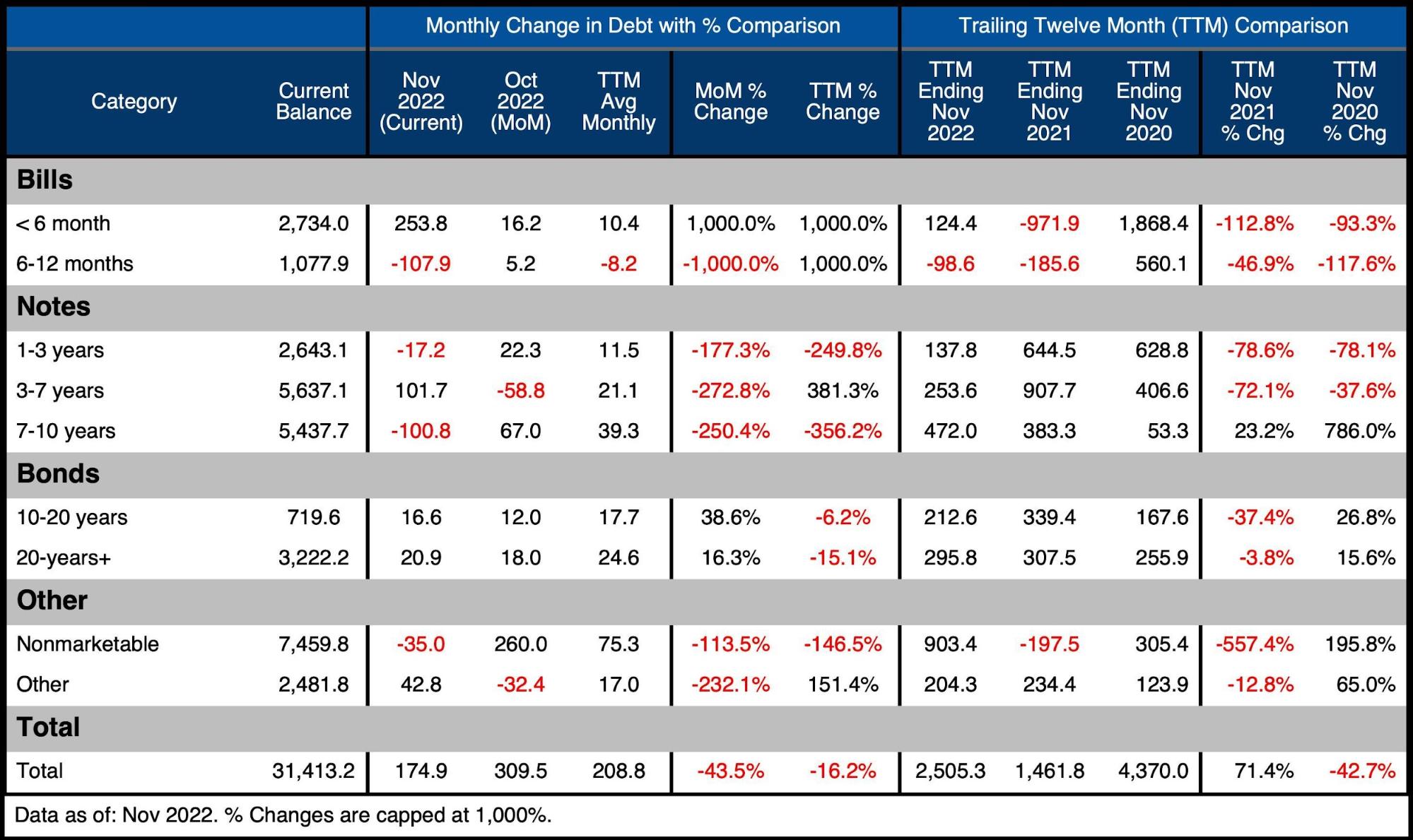

The table below summarizes the total debt outstanding. A few key takeaways:

On a monthly basis:

-

- Short Term debt was dominated by Bills maturing in less than 6 months

-

- This is likely a maneuver to move money around for the debt ceiling

-

- Notes actually fell slightly while bonds added $36.5B (below the TTM average)

- Short Term debt was dominated by Bills maturing in less than 6 months

On a TTM Basis:

-

- Bills are now positive over the TTM vs a fall of $1.5T in the previous 12 months

- Over the last 12 months, total debt has increased $2.5T

-

- Non-Marketable added almost $1T over that time vs ~$100B over the prior two years combined

-

Figure: 8 Recent Debt Breakdown

A Looming Recession

Making matters much worse is the looming recession. This will likely mean higher federal spending against a backdrop of falling tax revenues. The yield curve is the most inverted in 40 years, which indicates the markets believe a recession is coming.

Figure: 9 Tracking Yield Curve Inversion

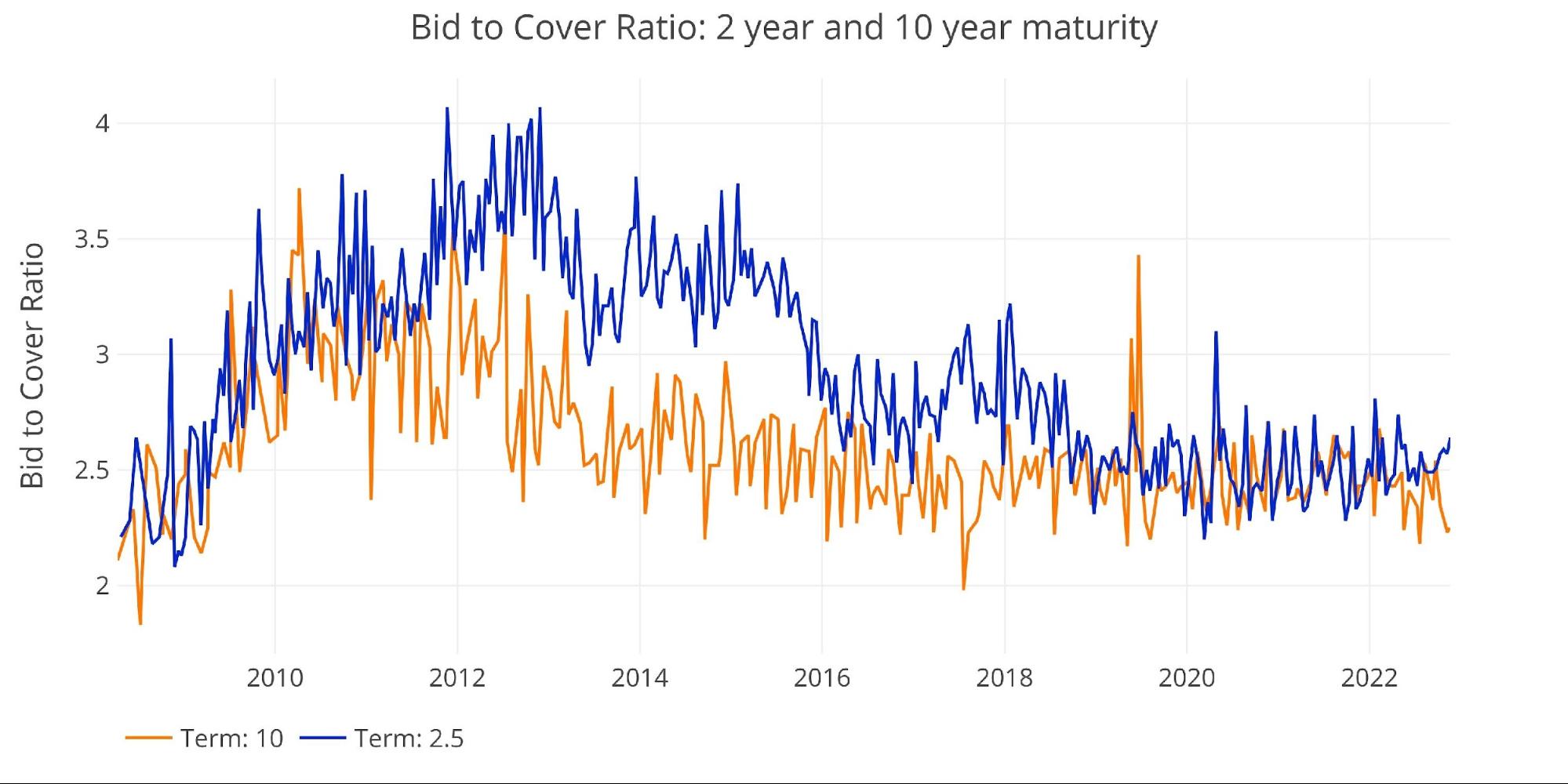

Unfortunately, just as the Treasury will need to issue more debt, the bid-to-cover ratio for new Notes 7-10 years is near multi-year lows. This indicates sagging demand for Treasuries.

Figure: 10 2-year and 10-year bid to cover

Putting the picture together, the Treasury is facing exploding debt, surging interest costs, and shrinking demand for its debt. The Fed will not be able to sit on the sidelines long in this environment.

Historical Perspective

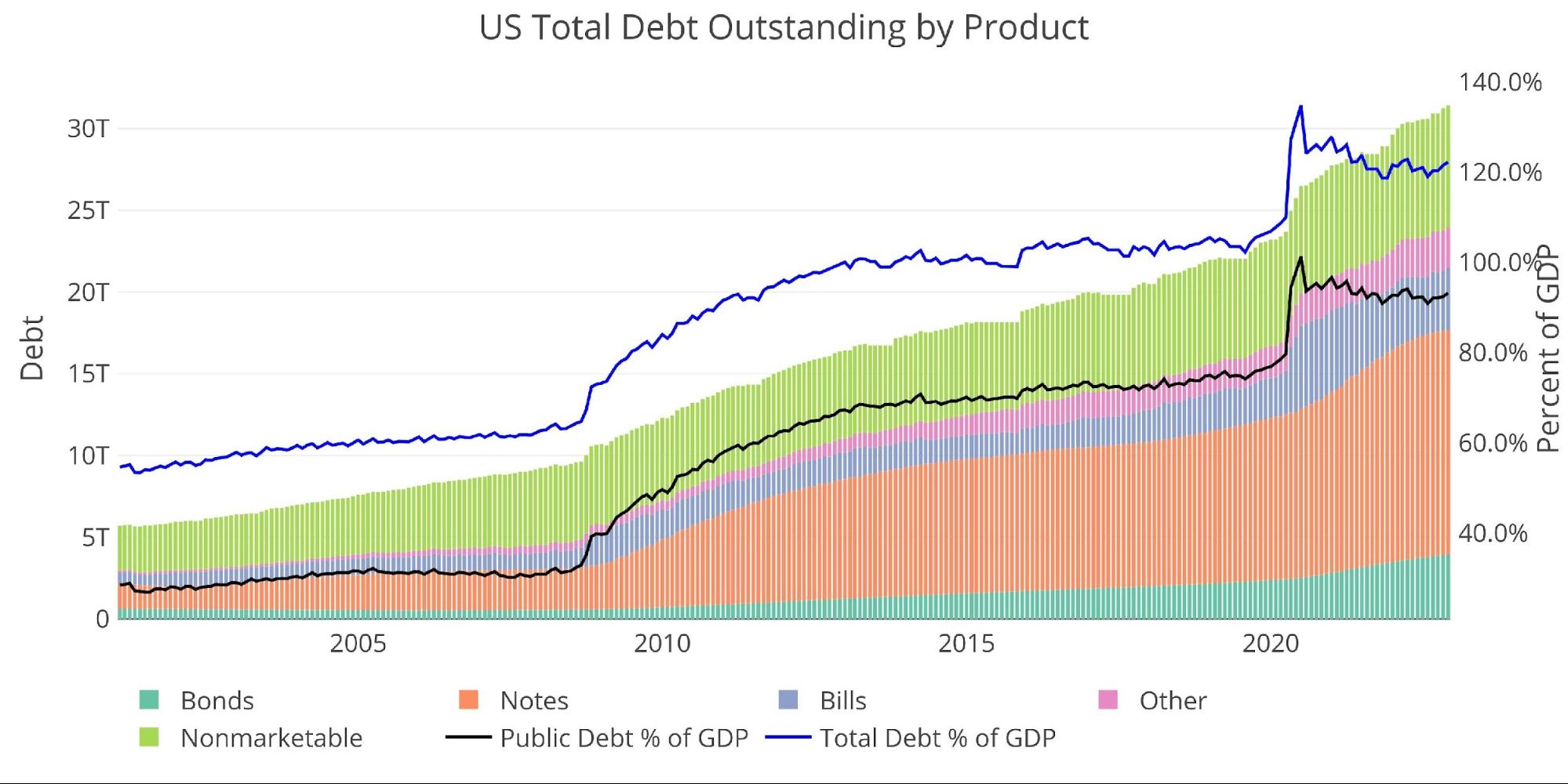

While total debt now exceeds $31T, not all of it poses a risk to the Treasury. There is $7.5T+ of Non-Marketable securities which are debt instruments that cannot be resold and the government typically owes itself (e.g., Social Security).

Figure: 11 Total Debt Outstanding

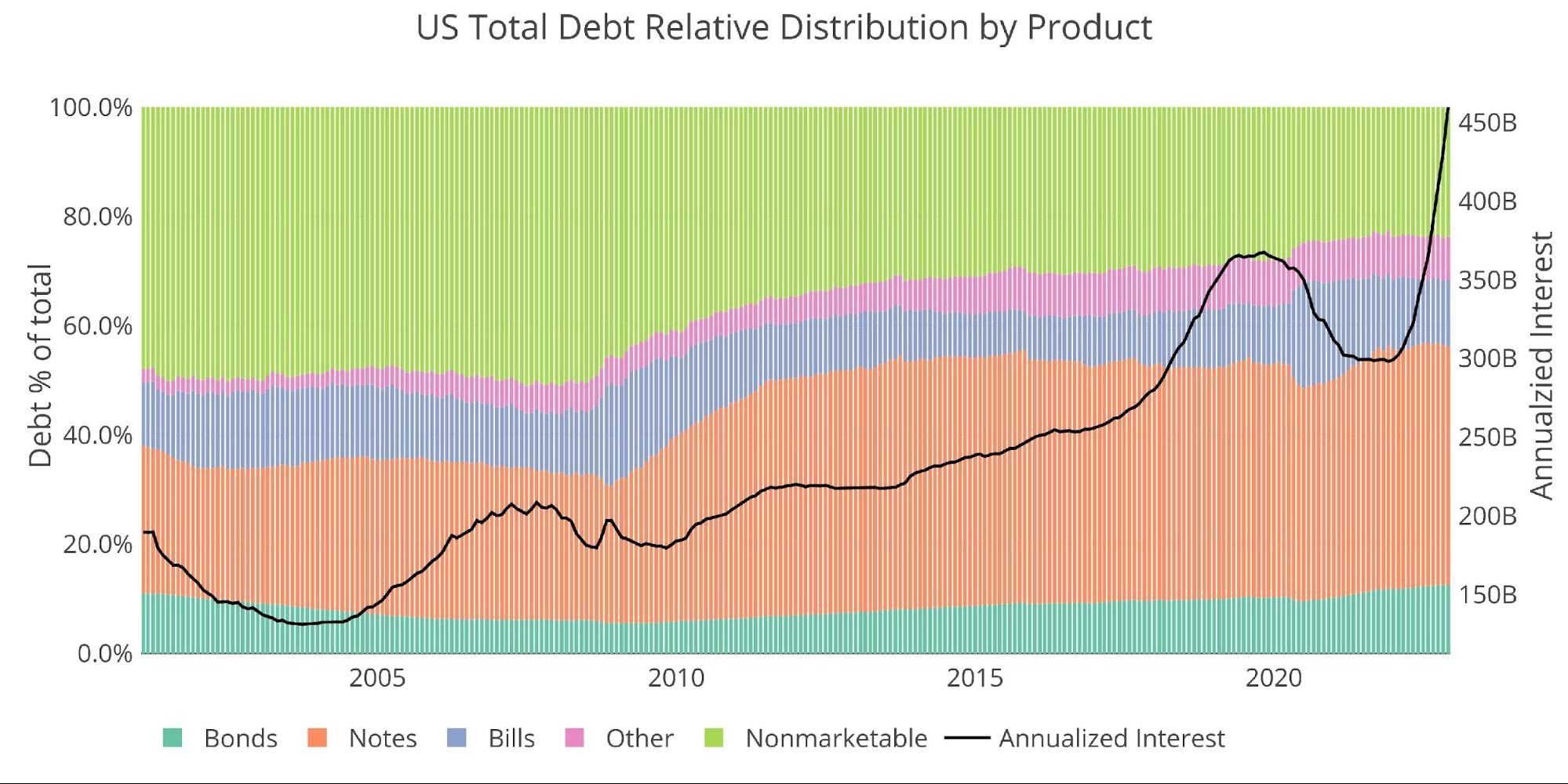

Unfortunately, the reprieve offered by Non-Marketable securities has been fairly limited in recent years, as the Treasury has been forced to rely more heavily on private markets. This has made Non-Marketable fall from over 50% of the debt to less than 25% of total debt outstanding.

Figure: 12 Total Debt Outstanding

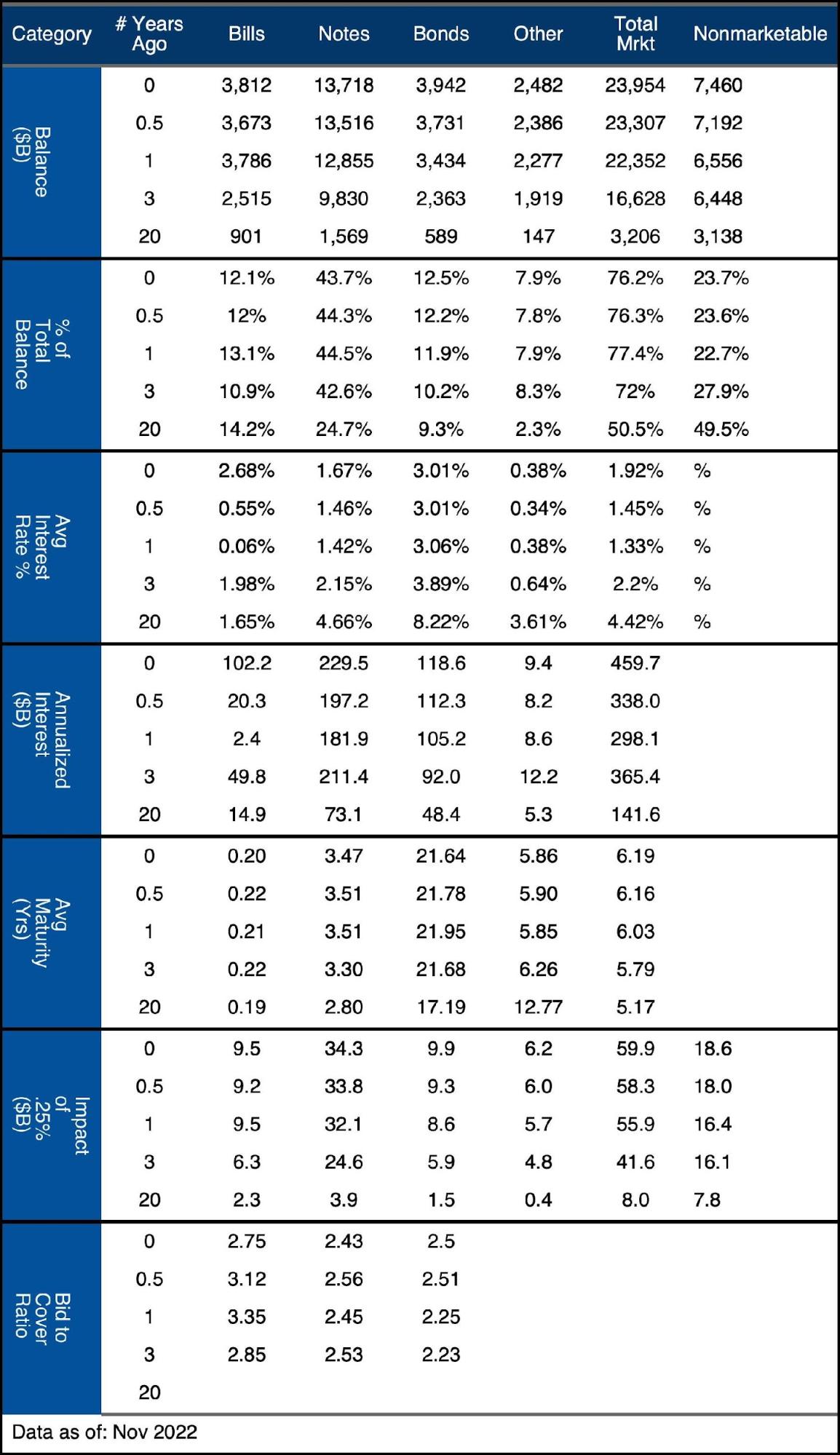

Historical Debt Issuance Analysis

The table below breaks down the trends shown above with specific numbers.

Figure: 13 Debt Details over 20 years

It can take time to digest all the data above. Below are some main takeaways:

-

- Average interest rates on Bills have increased from 0.06% to 2.68% in 12 months

-

- This has increased annualized interest from $2.4B to $102B just on Bills

-

- The increased interest in Notes has been slower, rising 25bps over the same period

-

- Despite the relatively small move, the increase in dollars is almost $50B

-

- Every 25bps hike will cost the Treasury $60B after it works its way through the curve.

- Average interest rates on Bills have increased from 0.06% to 2.68% in 12 months

What it means for Gold and Silver

This is clearly an unsustainable situation. By July, interest on the debt will have increased $400B or 135% since July 2021! Where is the Treasury going to find an extra $400B? It will borrow it, increasing the debt and initiating the downward spiral.

The Fed can talk as tough as it wants, but the math is pretty simple at this point. Either the Fed folds or the Federal Budget blows up. Gold and silver offer excellent insurance against either scenario. For anyone who doesn’t hold their metal, keep in mind that the paper claims on remaining vaulted metal continue to increase. For example, there are now 17.4 paper ounces of silver for each physical ounce on the Comex. Something to consider as the Treasury hurtles towards a debt crisis.

Data Source: https://www.treasurydirect.gov/govt/reports/pd/mspd/mspd.htm

Data Updated: Monthly on fourth business day

Last Updated: Nov 2022

US Debt interactive charts and graphs can always be found on the Exploring Finance dashboard: https://exploringfinance.shinyapps.io/USDebt/

Call 1-888-GOLD-160 and speak with a Precious Metals Specialist today!

Buka akaun dagangan patuh syariah anda di Weltrade.

Source link