FRA-OIS Explodes: Here Is The Only Chart Powell Is Closely Watching, And Why It Is Soaring

Some were quick to mock repo guru and former NY Fed staffer Zoltan Pozsar when he warned that the unexpected western blockade of Russia had the feel of a Lehman weekend, because virtually nobody had any idea what the forced exclusion of a G-20 economy from the global financial system would lead to. In fact, just yesterday Jerome Powell admitted that he had not been consulted, suggesting that arguably the most momentous financial decision in modern history has made without consulting the single most important financial person in the world.

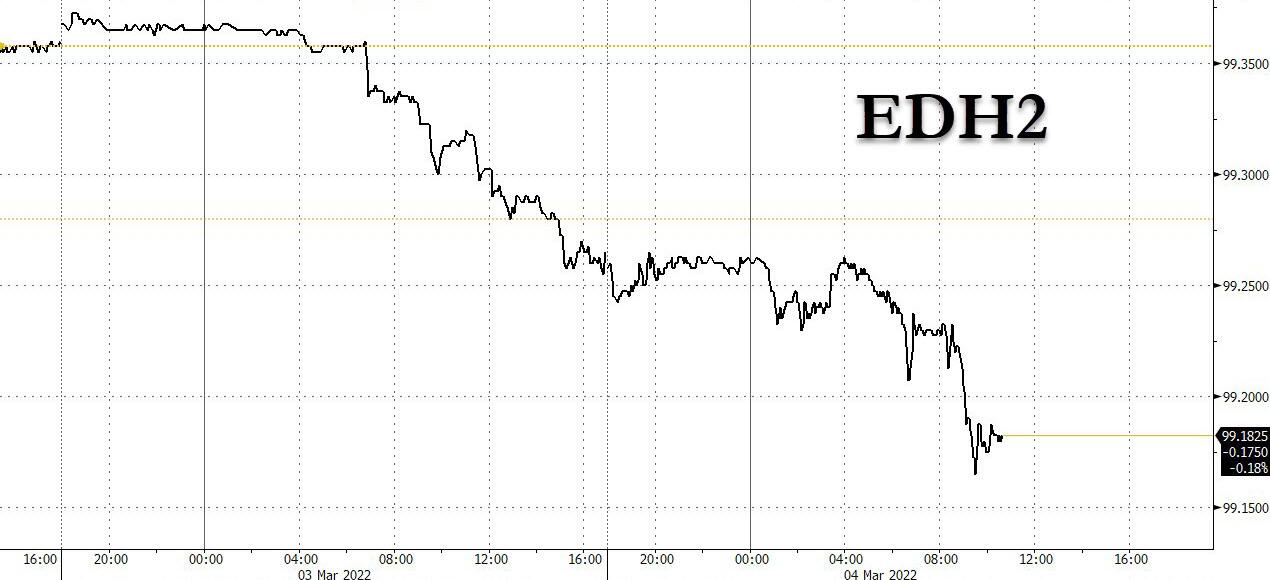

However, it appears that while Pozsar may have been ahead of the curve, as usual, he was not wrong, and today the all important FRA-OIS indicator of interbank funding stress (and money-market risk) is surging, and at last check was above 37bps, up a whopping 12 pts…

… amid relentless selling in March 2022 eurodollar futures with the contract off session lows but remains cheaper by around 10bp on the day, with some speculating that at least some funding markets are starting to grind to a halt.

One can argue that while Powell and the Fed may be oblivious to the ongoing collapse in stocks, which they view as overvalued and as having enough buffer to drop especiallyhe is closely watching every uptick in this most critical stress indicator.

A very quick primer on this all important spread:

- What is FRA? A forward rate agreement is a deal to swap future fixed interest payments for variable ones, or vice versa. The key rate for U.S. markets is the three-month London interbank offered rate, or Libor, in U.S. dollars. The benchmark is derived by major banks submitting rates based on transactions that are compiled to establish benchmark for five different currencies across seven different loan periods. Those benchmarks underpin interest rates on trillions of dollars of financial instruments and products from student and car loans to mortgages and credit cards.

- What is OIS? The Overnight Index Swap rate is calculated from contracts in which investors swap fixed- and floating-rate cash flows. Some of the most commonly used swap rates relate to the Federal Reserve’s main interest-rate target, and those are regarded as proxies for where markets see U.S. central bank policy headed at various points in the future.

Oh, that’s the theory. But why does the FRA-OIS spread matter in practice?

Well, it’s regarded as the markets’ measure of how expensive or cheap it will be for banks to borrow in the future, as shown by Libor, relative to a risk-free rate, the kind that’s paid by highly rated sovereign borrowers such as the U.S. government. The FRA-OIS spread provides another snapshot of how the market is viewing credit conditions because of the fact that traders are betting on where Libor-OIS — its underlying spread — will be.

As a further reminder, there are typically 3 reasons why it would blow out:

- the risk premium for uncertainty of US monetary policy,

- recently elevated credit spreads (CDS) of banks, and

- demand for funds in preparation for market stress.

While FRA-OIS exploded to 80bps in March 2020, at the peak of the covid crash, and is currently at just half that level, never before has funding stress been so high with a Fed balance sheet near $9 trillion and with some $1.6 trillion in the Fed’s overnight reverse repo facility.

In other words, when adjusted for the statutory level of liquidity in the market, which we don’t need to tell readers is at an all time high, the FRA-OIS would almost certainly be at all time highs.

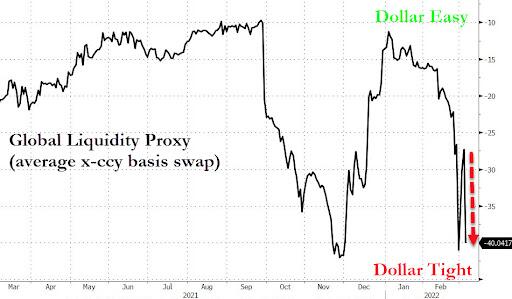

Whatever the reasons, a blow out in FRA/OIS means that dollar funding is becoming increasingly problematic, and absent a sharp tightening in the Libor-OIS and FRA-OIS spread, while bank credit concerns may not have been the catalyst for the sharp spike, it will be banks that are eventually impacted by what is increasingly emerging as an acute tightening in short-term funding markets and/or a global dollar shortage. And in another indication that the FRA-OIS is indeed spiking in response to an ominous global dollar shortage – just the outcome Pozsar warned about and one which shouldn’t be happening when factoring in the record endogenous market liquidity – we find that the average cross-currency basis swap is tumbling. This global liquidity proxy tends to shrink any time there is prevailing dollar tightness in the market.

While this is a topic we covered extensively back in March 2020 (see “There Is No Liquidity” – Market Paralyzed As FRA/OIS Explodes), especially right before the Fed unleashed its monetary bazooka with trillions in QE and opening up repos to virtually unlimited amount, as well as announcing it would buy corporate bonds and ETFs, expect to hear much more about this in the days and weeks ago come.

Meanwhile, if the FRA-OIS spikes another 10-15 points, the Fed will have no choice but to emerge from its paralysis and reassure markets that the financial system isn’t about to experience another paralysis (oh, and unless the Ukraine war magically ends in the next few weeks, say goodbye to “six or seven” rate hikes this year).

Source link