The following analysis breaks down the Fed balance sheet in detail. It shows different parts of the balance sheet and how those amounts have changed. It also shows historical interest rate trends. The analysis concludes that the resulting lack of Treasury demand is likely another reason Yellen is betting $2T on lower interest rates… she has to focus on the short-term of the curve to make sure the market can absorb the debt!

Breaking Down the Balance Sheet

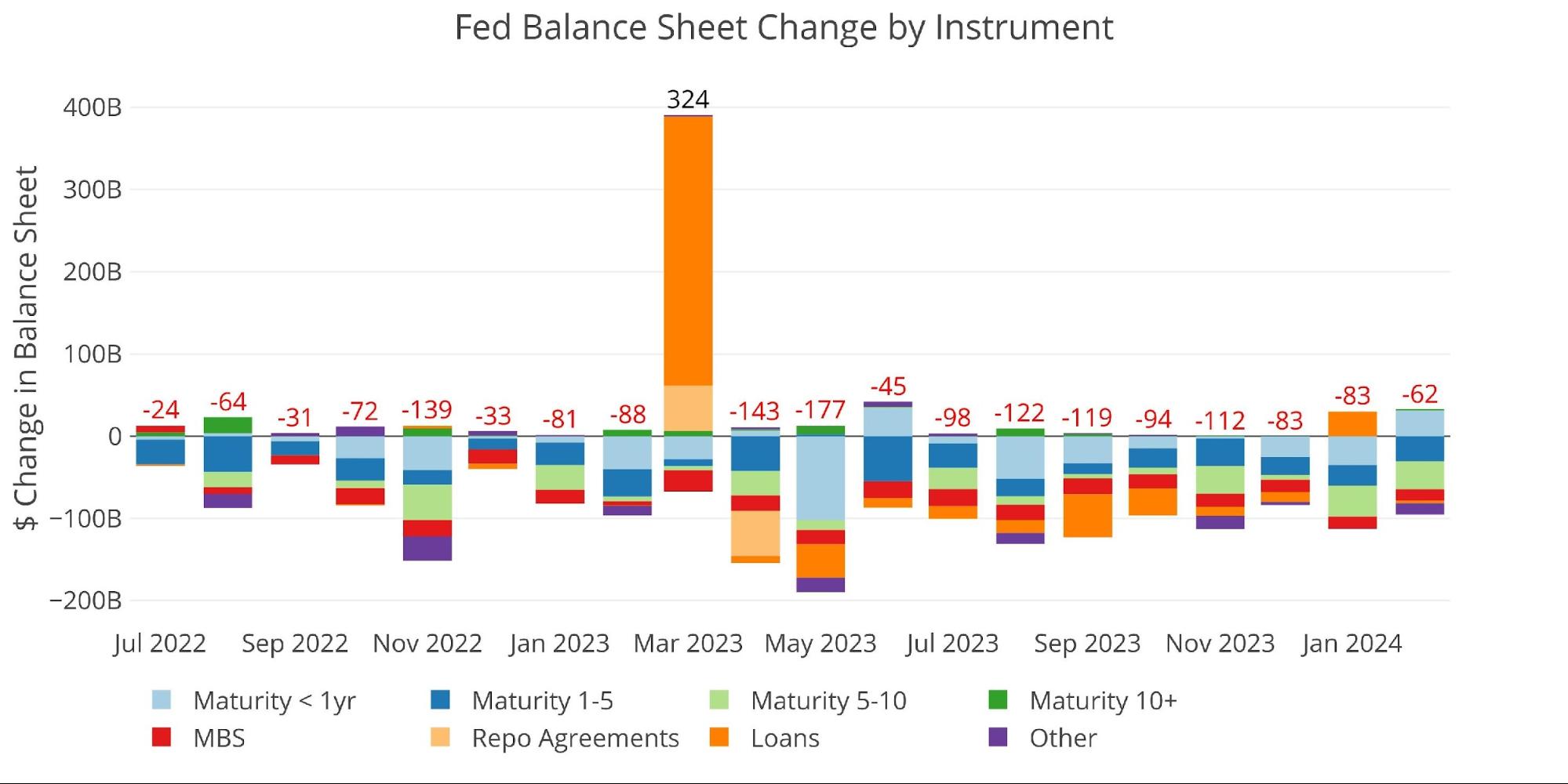

The Fed balance sheet shrunk by $62B in February, the smallest amount since the Regional Banking Crisis in 2023. The change in trend was primarily driven by an increase in short-term debt (Maturity <1 year).

Figure: 1 Monthly Change by Instrument

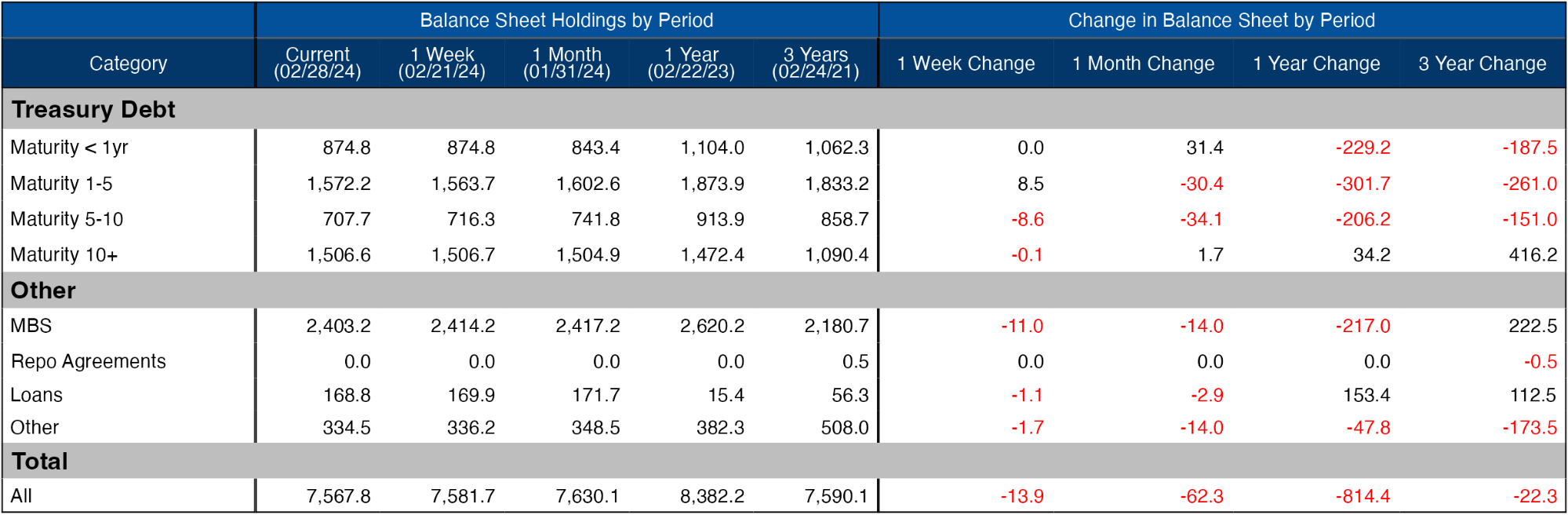

The table below provides more detail on the Fed’s QT efforts. It shows the increase in short-term debt happened at the beginning of February ($31.4B).

Figure: 2 Balance Sheet Breakdown

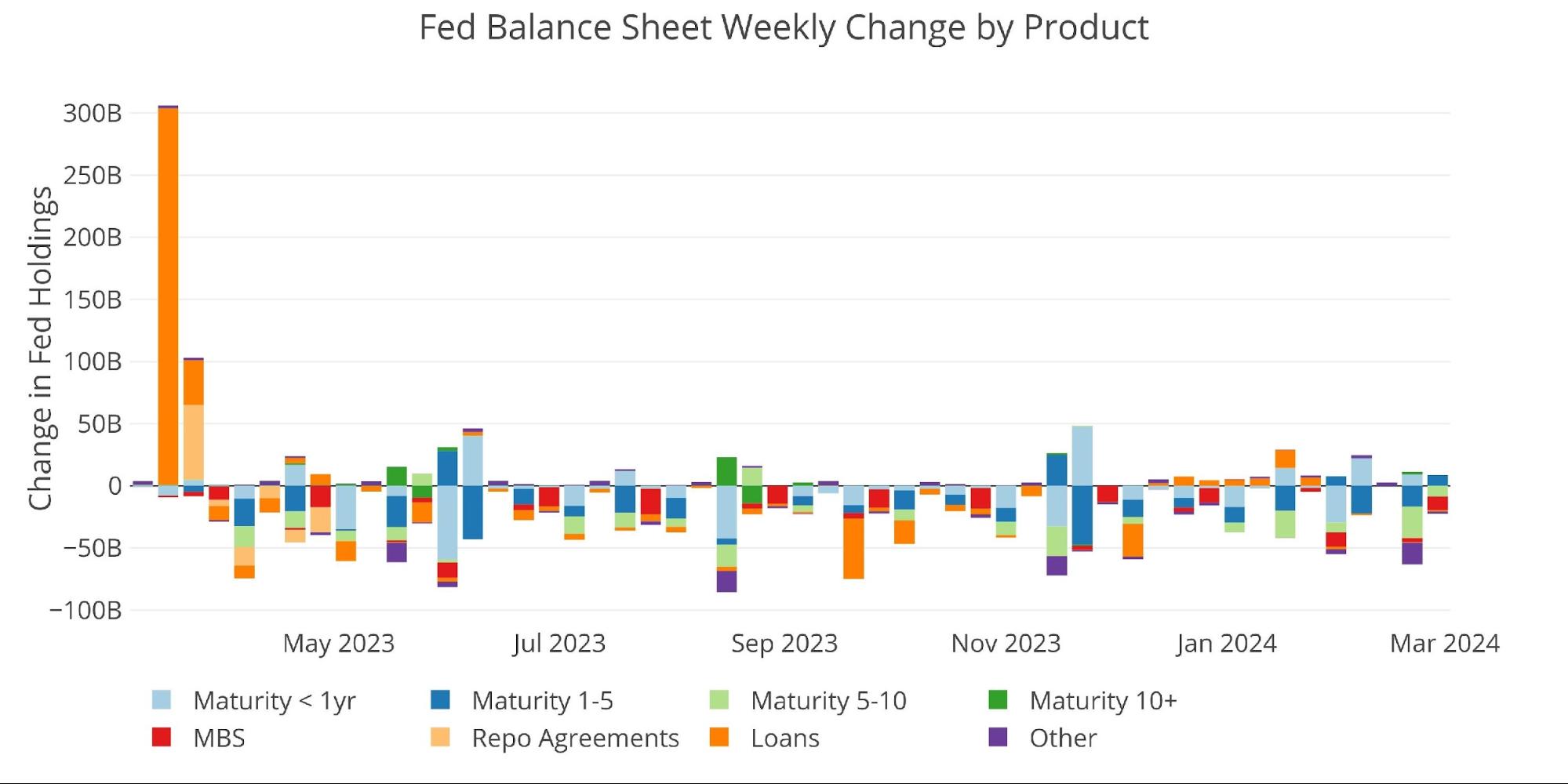

The weekly activity can be seen below. It shows that a big move in T-bills happened in the first week of February.

Figure: 3 Fed Balance Sheet Weekly Changes

The chart below shows the balance on detailed items in Loans and also Repos. These were the programs set up in the wake of the SVB collapse last year. Three of the four programs have dropped close to zero, but the Bank Term Funding Program (BTFP) remains elevated. The BTFP was the program that allowed banks to value their Treasury assets at par for up to one year. The initial surge happened throughout March of last year so it will be interesting to see how those agreements unwind next month.

Figure: 4 Loan Details

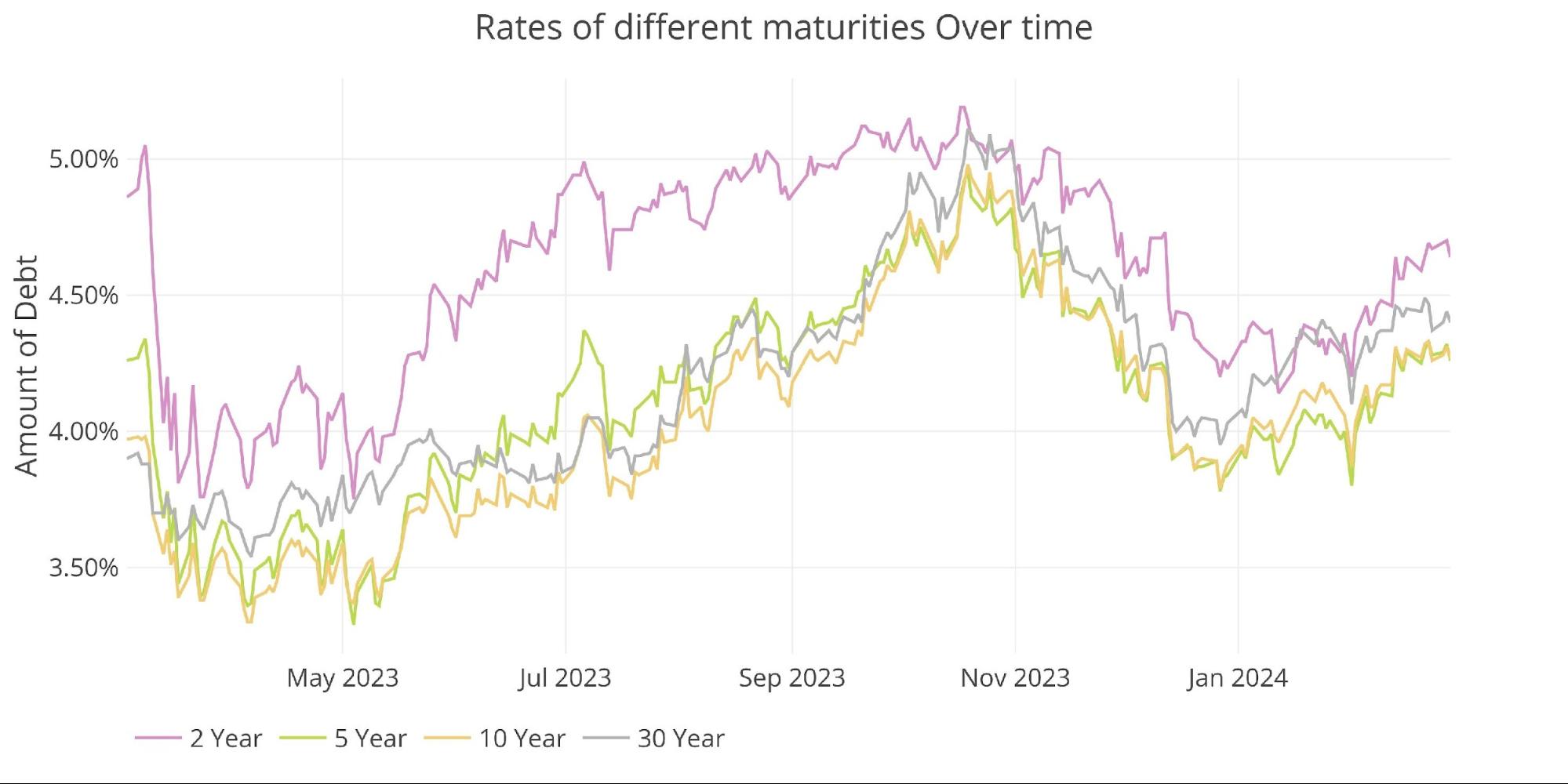

Yields

Yields have climbed back up in recent weeks.

Figure: 5 Interest Rates Across Maturities

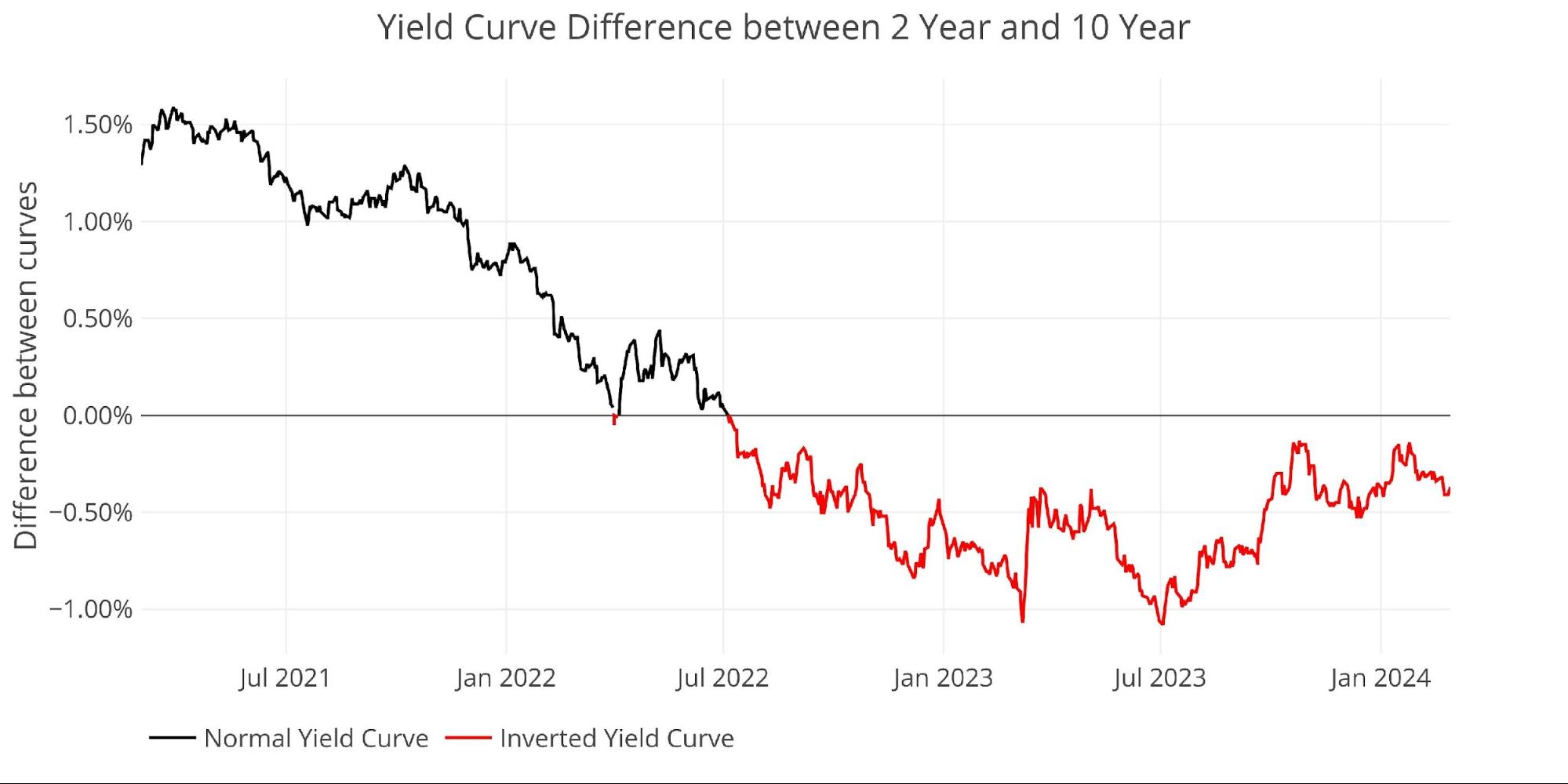

The yield curve remains inverted at -39bps.

Figure: 6Tracking Yield Curve Inversion

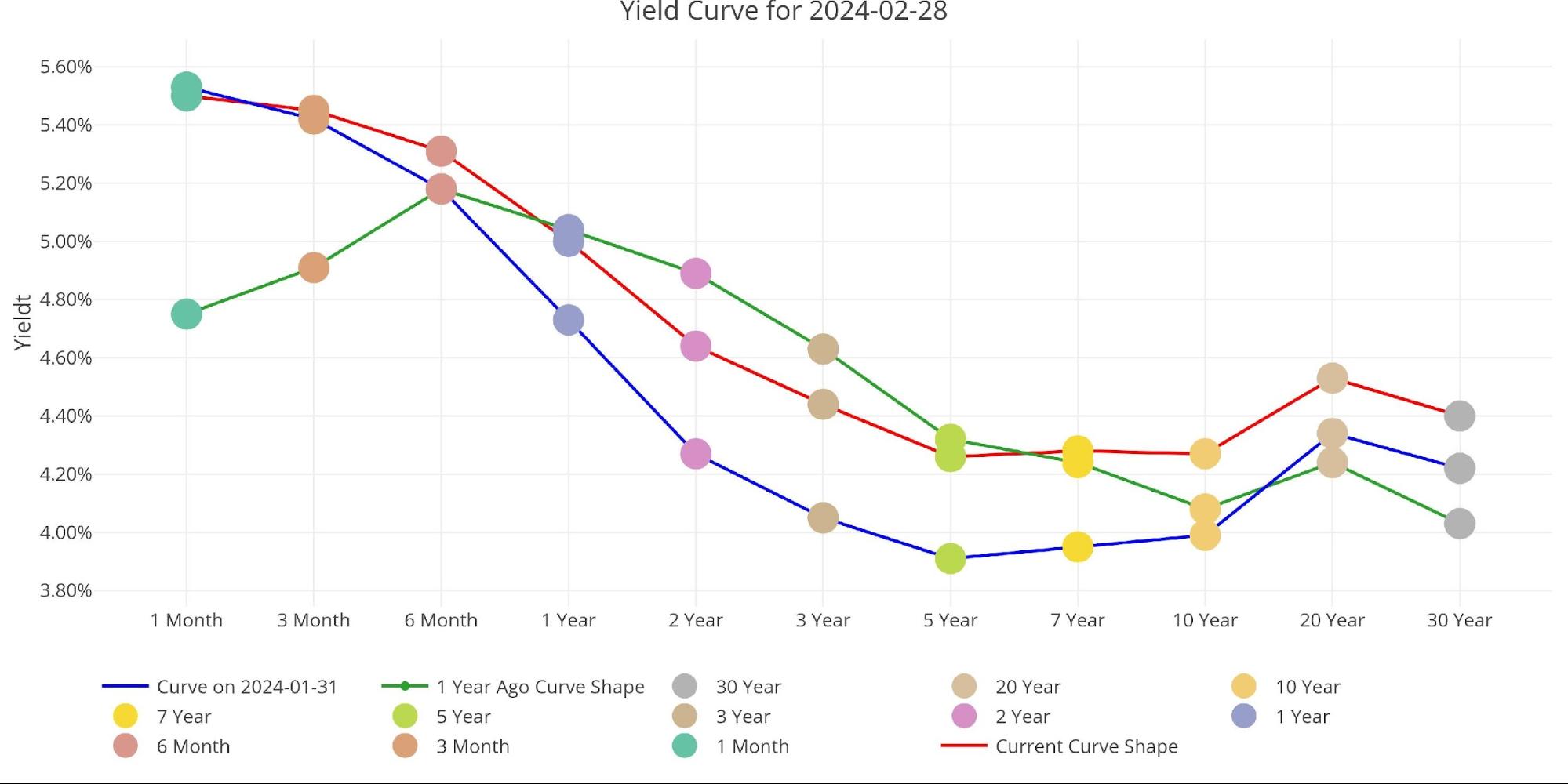

The chart below shows the current yield curve, the yield curve one month ago, and one year ago. This view clearly shows the inversion of the yield curve across most maturities

Figure: 7 Tracking Yield Curve Inversion

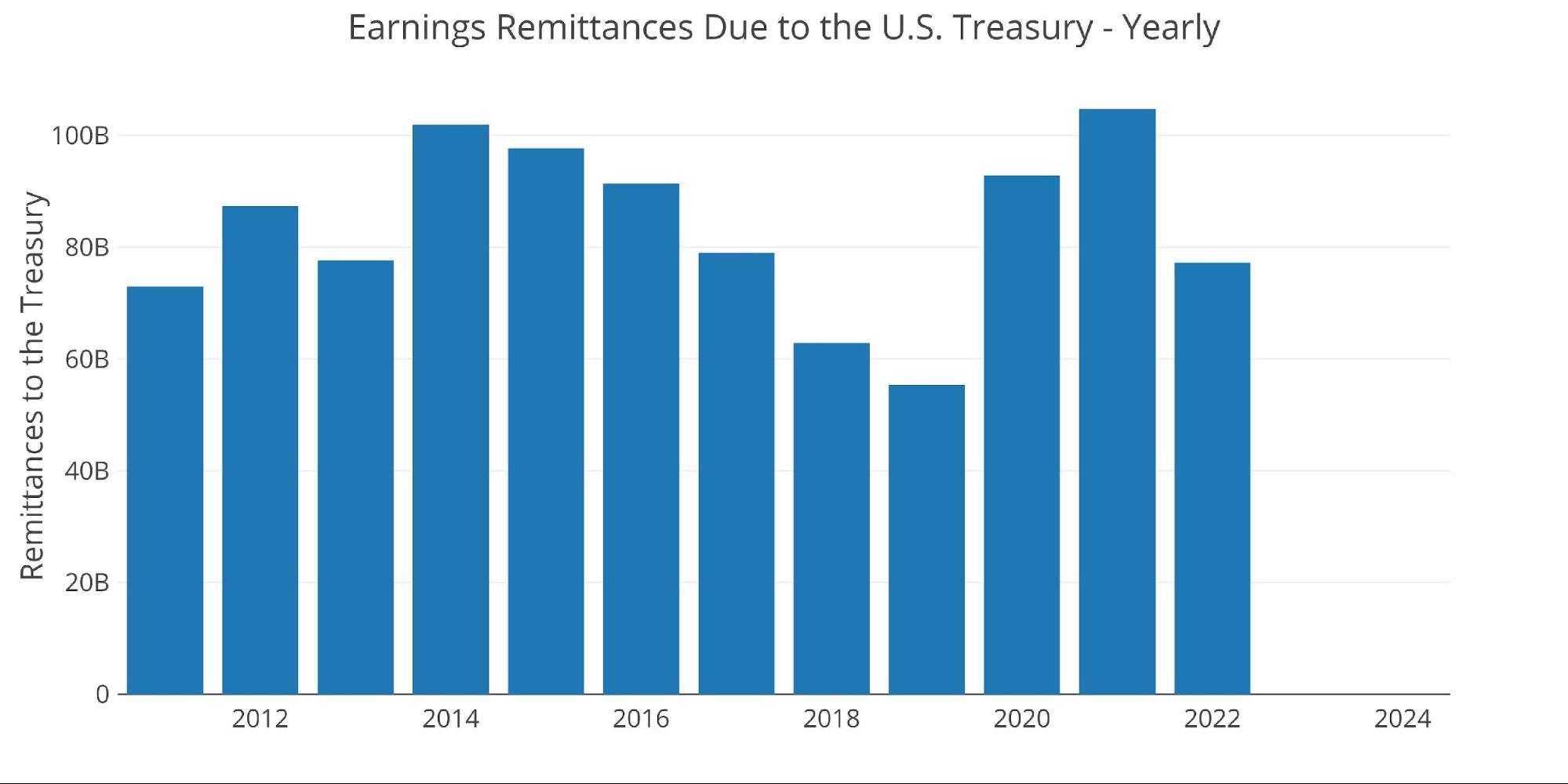

The Fed Takes Losses

When the Fed makes money, it sends it back to the Treasury. This has netted the Treasury close to $100B a year. This can be seen below.

Figure: 8 Fed Payments to Treasury

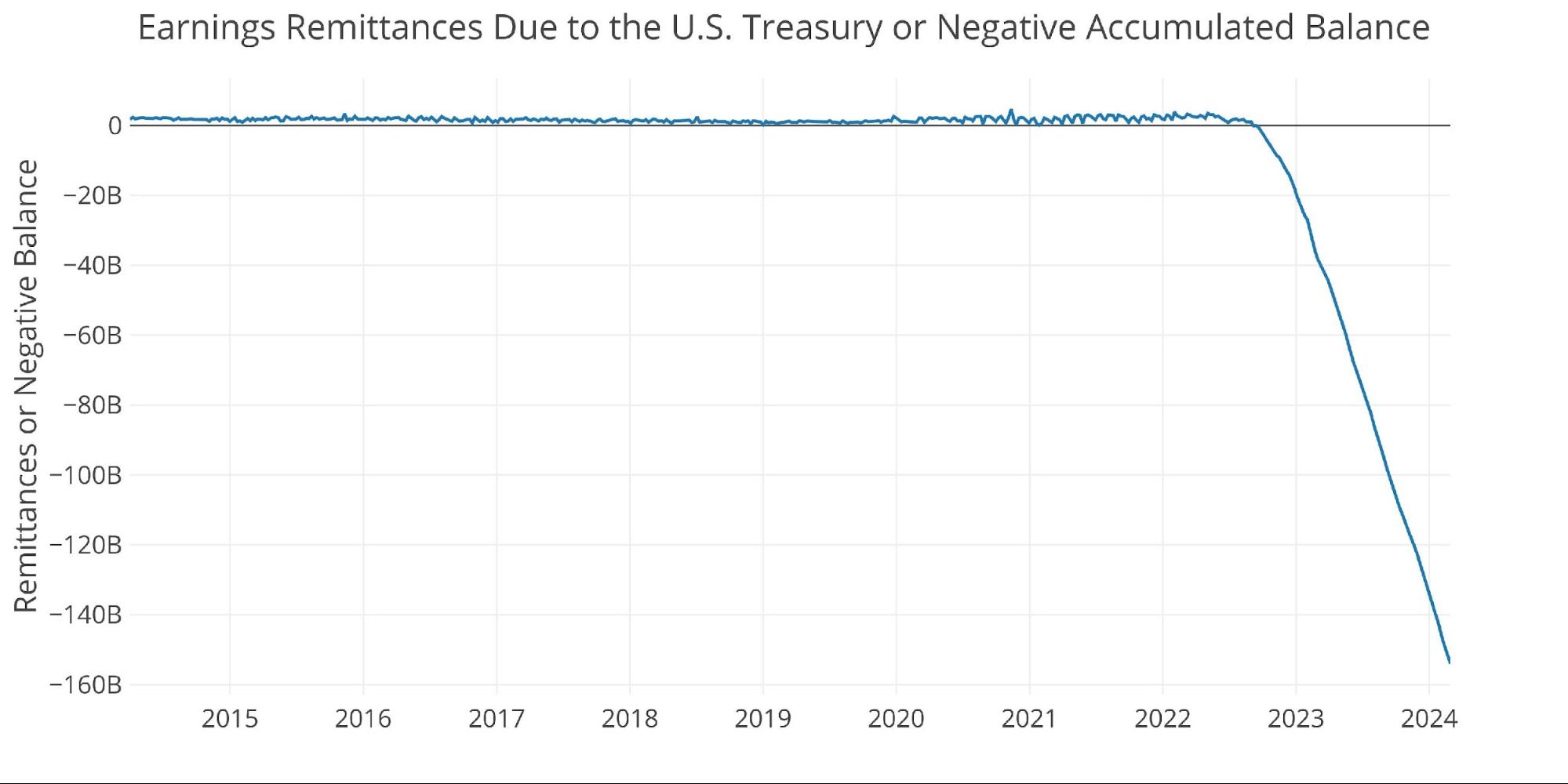

You may notice in the chart above that 2023 and 2024 are showing $0. That’s because the Fed has been losing money. According to the Fed: The Federal Reserve Banks remit residual net earnings to the U.S. Treasury after providing for the costs of operations… Positive amounts represent the estimated weekly remittances due to U.S. Treasury. Negative amounts represent the cumulative deferred asset position … deferred asset is the amount of net earnings that the Federal Reserve Banks need to realize before remittances to the U.S. Treasury resume.

Basically, when the Fed makes money, it gives it to the Treasury. When it loses money, it keeps a negative balance by printing the difference. That negative balance has just exceeded $153! This negative balance is increasing by about $10B a month!

Figure: 9 Remittances or Negative Balance

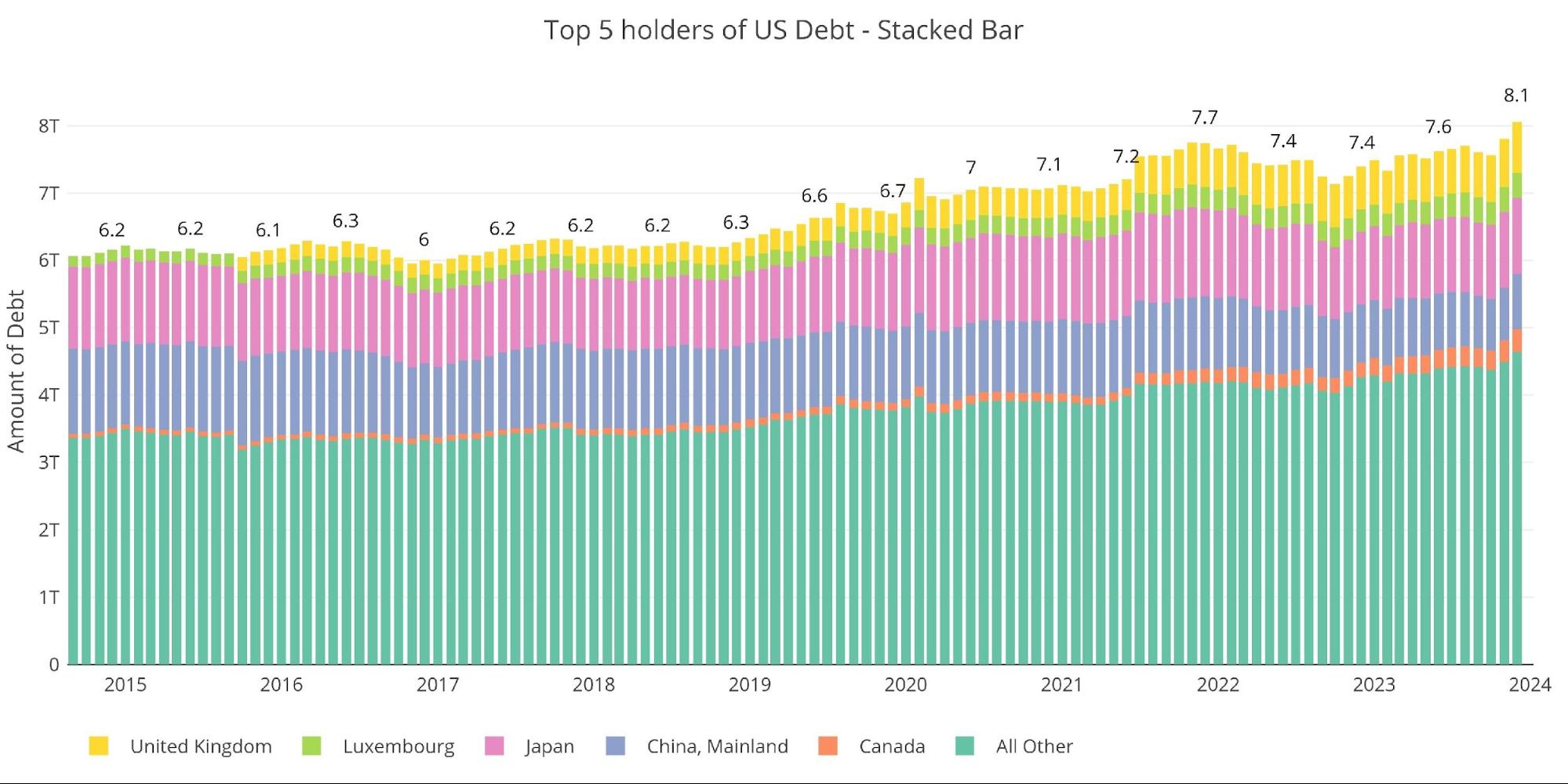

Who Will Fill the Gap?

The Fed has not been buying in the Treasury market for over a year (they have been selling); however, the Treasury is still issuing tons of new debt. Who has been picking up the slack since the Fed stepped away?

International holdings have been steady since July 2021 at around $7.6T. The latest month did see an increase in foreign holdings compared to recent months, but it’s not nearly enough to make up for all the debt the Treasury has issued.

Note: data is updated on a lag. The latest data is as of December

Figure: 10 International Holders

It should be noted that both China and Japan (the largest international holders of Treasuries) have been reducing Treasury holdings. China is now nearing $800B in total holdings (down from $1.25T) with Japan dropping down to almost $1T.

Figure: 11 Average Weekly Change in the Balance Sheet

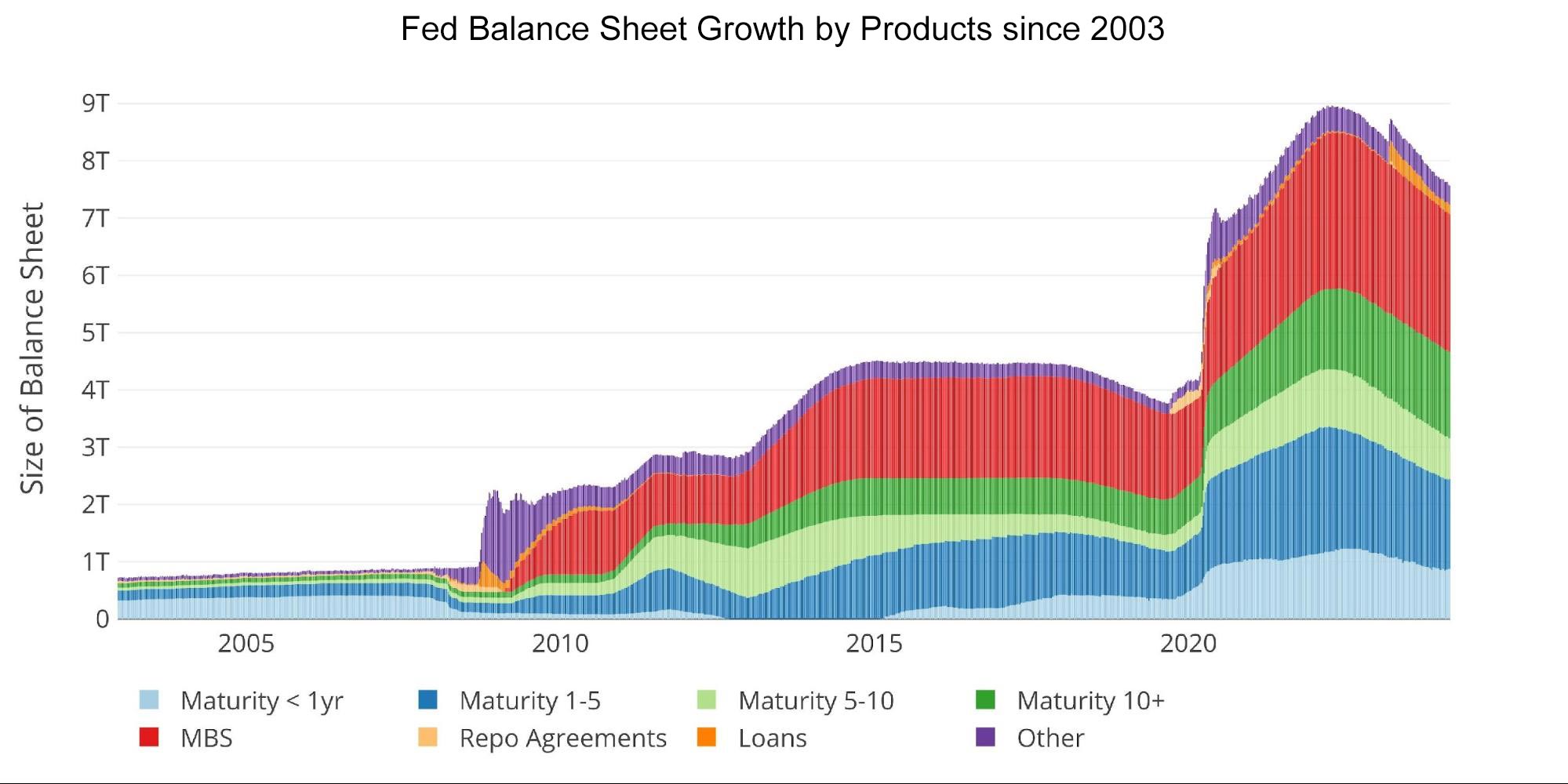

Historical Perspective

The final plot below takes a larger view of the balance sheet. It is clear to see how the usage of the balance sheet has changed since the Global Financial Crisis.

The recent moves by the Fed in the wake of the SVB collapse can also be seen below. When the next break in the economy occurs, it’s likely that the balance sheet will spike again.

Figure: 12 Historical Fed Balance Sheet

Wrapping up

The lack of Fed buying combined with weak international demand creates a market that is not very deep or liquid in Treasuries. This is likely another reason the Treasury is issuing all short-term debt. Short-term debt is absorbed much more easily by the market compared to medium and long-term debt. With the Fed out of the market as buyers and international holders not buying much, the Treasury is issuing only the debt that will be well absorbed by the market to keep rates low.

Data Source: https://fred.stlouisfed.org/series/WALCL and https://fred.stlouisfed.org/release/tables?rid=20&eid=840849#snid=840941

Data Updated: Weekly, Thursday at 4:30 PM Eastern

Last Updated: Feb 28, 2024

Interactive charts and graphs can always be found on the Exploring Finance dashboard: https://exploringfinance.shinyapps.io/USDebt/

Call 1-888-GOLD-160 and speak with a Precious Metals Specialist today!

Buka akaun dagangan patuh syariah anda di Weltrade.

Source link