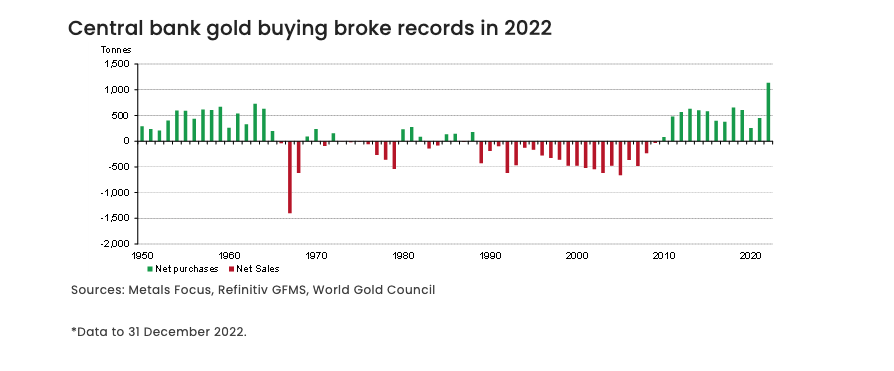

Central banks have been gobbling up gold. On net, central banks bought 1,136 tons of gold in 2022. It was the highest level of net purchases on record dating back to 1950 and the 13th straight year of net gold purchases.

The question is will central banks continue to have an appetite for gold through 2023?

According to the World Gold Council, the most likely answer to that question is “yes.”

This extended period of net gold purchases started in 2010. That was preceded by nearly 50 years of declining world gold reserves.

Many people wonder if the recent trend of net buying will give way to significant net sales as we saw in the late 1960s. According to World Gold Council senior market analyst Louise Street, most likely not.

In fact, we’re confident that central banks will continue to build their official gold holdings.”

Central bankers have indicated as much. According to the most recent annual central bank survey conducted by the WGC last summer, central bankers view gold favorably as a reserve asset. At the time, 61% of respondents stated that they expected global gold reserves to increase over the next 12 months.

Street points out that the dynamics in the late 1960s were much different than today. At that time, a gold standard was in place.

Under the Bretton Woods system, the US – and a syndicate of European central banks – was committed to defending a fixed price of gold, which was convertible to the US dollar at US$35/ounce.

The hefty sales we saw in 1967 were a consequence of this price peg coming under attack as investors piled into gold. The influx was driven by safe-haven motives (fuelled by jitters that a devaluation of sterling signaled a possible currency collapse) and the lure of potential profit as speculators bet that the dollar would be next to fall and the gold price would be unleashed.

The banks in question avoided this scenario by selling vast quantities of gold – around 2,000 tonnes in total over 1967/68. But the episode effectively signaled the end of the Bretton Woods system and the last remnants of the Gold Standard.

In fact, Richard Nixon slammed the gold window shut in 1971.

After the world went off the gold standard, many western central banks were overallocated to gold. That led to a structured program of controlled sales in the 1990s. That has ended.

Meanwhile, emerging market (EM) banks remain relatively under-allocated to gold. Collectively, EM central banks’ gold reserves remain under 10% of total reserves. That’s less than half of the holdings by banks in advanced economies. And this number is skewed further by several EM banks such as Kazakhstan and Uzbekistan that hold around 60% of their reserves in gold.

Given the global economic dynamics, rampant inflation, and geopolitical instability, emerging markets will likely want to expand their gold holdings in the coming years.

Central banks are disproportionately exposed to advanced economy government debt – i.e. US Treasury bonds. But even with rising interest rates, the yield on this debt is relatively low and in real terms often negative.

Meanwhile, the US has used the dollar as a foreign policy tool. Many countries have intentionally worked to diversify away from dollar assets in order to shield themselves from sanctions and foreign policy manipulation.

As Street put it, “There has been a concerted shift away from over-reliance on the US dollar as a reserve currency, in an environment of non-existent real yields on sovereign debt.”

In this environment, gold looks very attractive compared to other reserve assets. It has no political risk, it can’t be debased and it can’t be talked down in a currency war of words. Our comprehensive central bank surveys confirm that gold is an important reserve asset – valued for its performance in times of crisis, its long-term store of value and lack of default risk. And it confirms that central bankers expect further growth in global gold reserves.”

One factor that could reduce central bank gold buying is a steep increase in the price of gold. This would not only curb purchases, but it would also likely incentivize selling by gold-producing countries.

Nevertheless, the World Gold Council expects the trend of increasing gold reserves to continue.

Overall, we expect further buying, with EM banks at the forefront of this trend as they continue to redress the imbalance in gold allocations with their developed market peers.”

Call 1-888-GOLD-160 and speak with a Precious Metals Specialist today!

Buka akaun dagangan patuh syariah anda di Weltrade.

Source link