Breaking Down the Balance Sheet

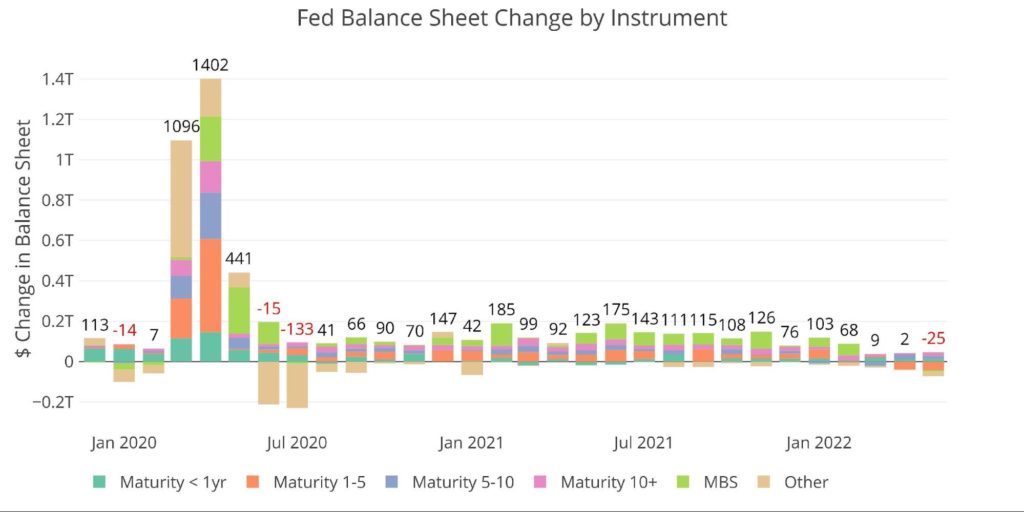

The Fed balance sheet fell during May by $25B. This was the first monthly decline in the balance sheet since $220B of “Other” rolled off in July 2020. In that case, “Other” were repurchase agreements with foreign entities to provide liquidity and alleviate stress in the global markets.

“Other” also played a role this month with $22B rolling off the balance sheet. The Fed actually increased total Treasuries by $5.5B despite $41.8B of 1-5 Year Maturities rolling off. Regardless, the Fed has clearly stopped QE and turned into net sellers in May. This is set to continue in June as the Fed embarks on QT.

Figure: 1 Monthly Change by Instrument

Given the recent fall in the money supply, the Fed is clearly trying to reduce stimulus in the economy. Unfortunately, the problem for the Fed is that the stimulus withdrawal has been extremely mild and yet has wreaked havoc on markets. This has left the Fed with tough talk as their primary tool to combat inflation.

They recognize there is little they can do to actually remove stimulus without collapsing the economy. Even Bullard, the most “hawkish” of Fed members, is talking about rate cuts in 2023 and 2024. How could the most hawkish FOMC member be talking about rate cuts in the middle of their inflation fight?

If they start cutting rates in 2023, will they also stop QT? 12 months of QT at $95B a month will reduce the balance sheet by $1.1T. This will do nothing to counteract the aggressive QE over the last two years.

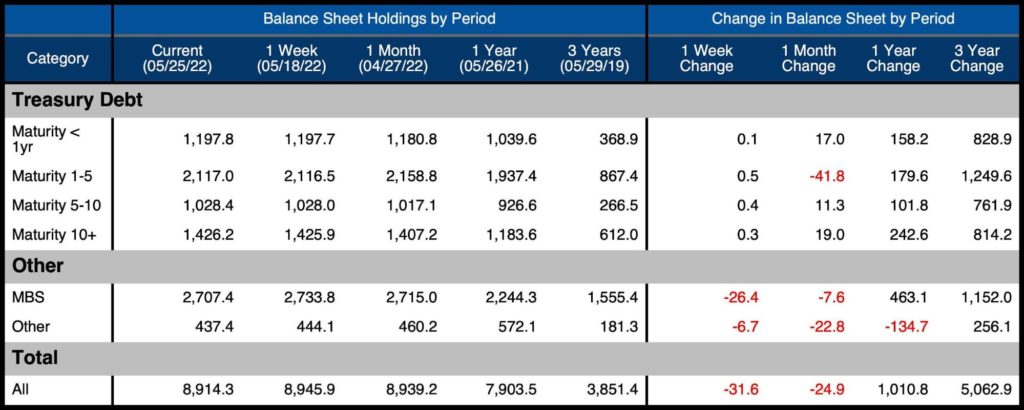

As shown in the table below, the Balance Sheet now stands at $8.9T. 3 Years ago the balance sheet was at $3.8T. It would take more than 4 years of $100B monthly QT just to get back to pre-Covid levels. Given that QT has not even started yet, this seems quite impossible.

Figure: 2 Balance Sheet Breakdown

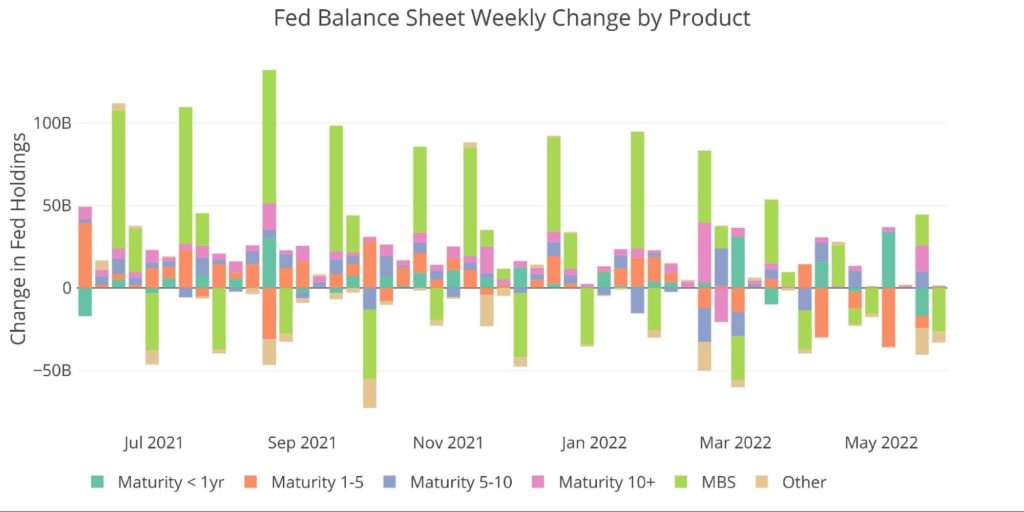

Looking at the weekly data shows how the activity on the balance sheet has transitioned over the last few months. It will be interesting to watch what the Fed starts rolling off in its first month of QT in June.

Figure: 3 Fed Balance Sheet Weekly Changes

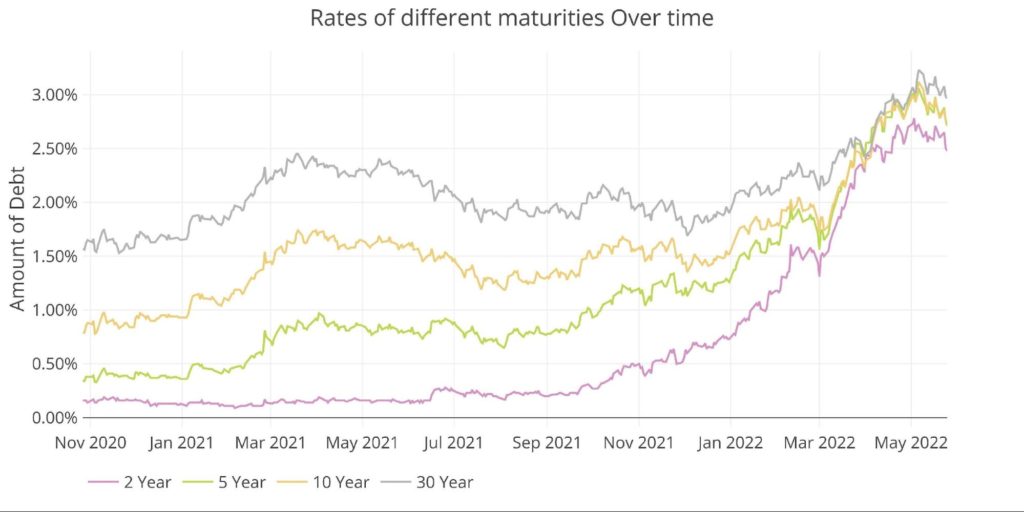

The bond market has certainly reacted to the Fed’s more hawkish tone. The 10-year reached 3.12% back on May 6 but has since dropped to 2.72%. The pullback most likely has two drivers:

- 3.1% is major resistance in the 40-year bond bull market

- The recent weak economic data may have the market pricing in a less hawkish Fed already

The second point is supported by the CEM Fed watch tool which has market participants already anticipating fewer hikes compared to one month ago.

Figure: 4 Interest Rates Across Maturities

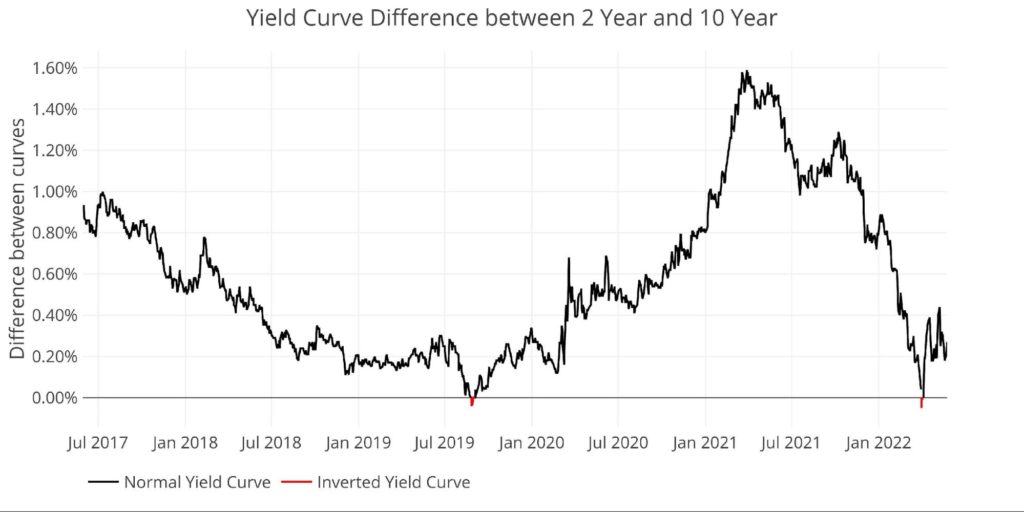

It’s hard to imagine the economy can avoid recession at this point. The tech sector is shedding jobs at a rapid pace. The yield curve was already inverted back in April. It had a big bounce but is starting to flatten again.

Figure: 5 Tracking Yield Curve Inversion

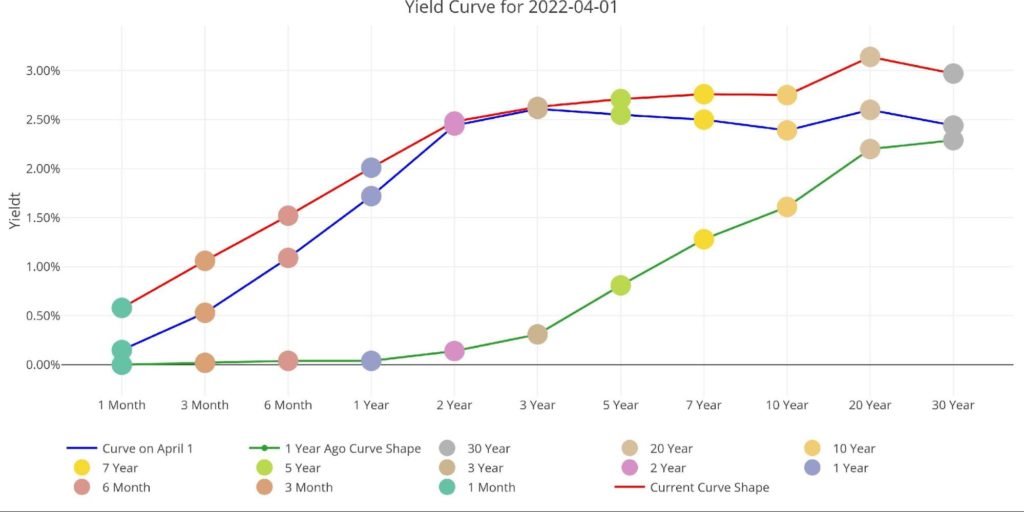

The chart below shows the entire yield curve compared to one year ago and on April 1 when it was inverted. Even though it is no longer inverted, comparing the blue line to the red line shows that the difference is minimal.

Figure: 6 Tracking Yield Curve Inversion

The Fed Monetization

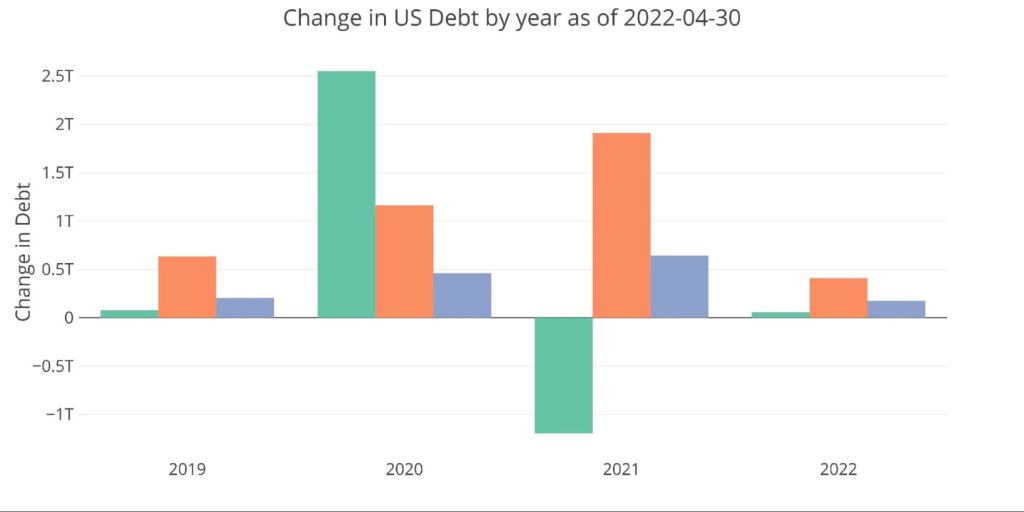

Although the Fed has stopped expanding the balance sheet, its actions in 2022 can be seen. The first chart below shows the amount of debt issued by the Treasury in the last 4 calendar years. So far, debt issuance in 2022 has been relatively mild compared to recent history with “only” $640B issued so far.

Figure: 7 Debt Issuance by Year and Instrument

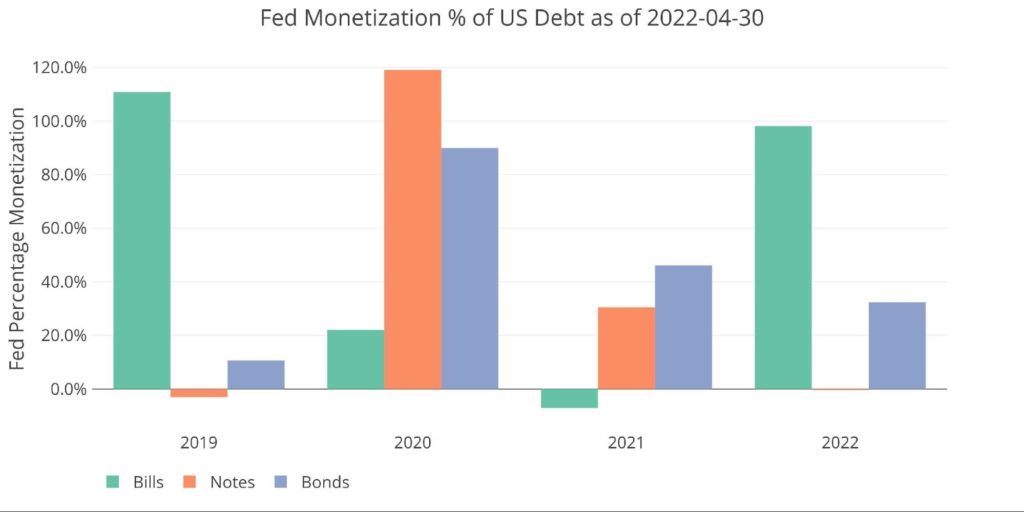

Ironically, due to this smaller issuance, the Fed has monetized nearly 100% of the Treasury Bills issued so far and 32% of the Bonds. Most issuance has been in Notes which the Fed has been entirely absent on.

Figure: 8 Fed Purchase % of Debt Issuance

Who Will Fill the Gap?

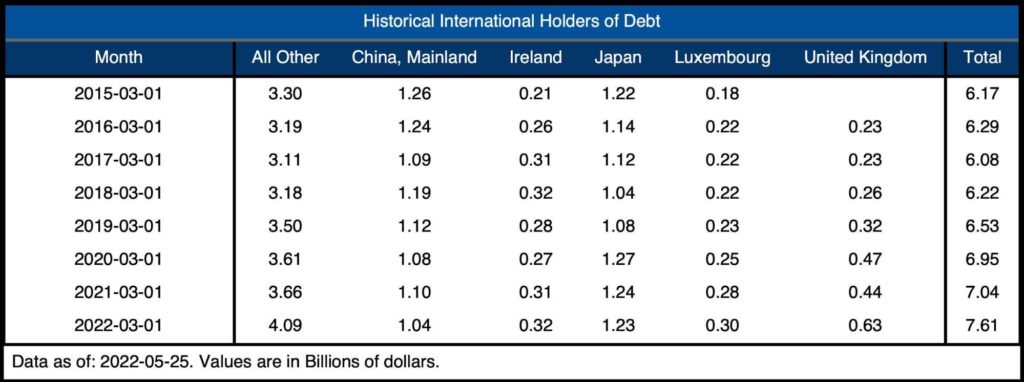

The chart below looks at international holders of Treasury securities. International holdings are down $135B from the peak in Nov 2021. It dropped by $100B between March and Feb alone!

Note: Data was last published as of March

Figure: 9 International Holders

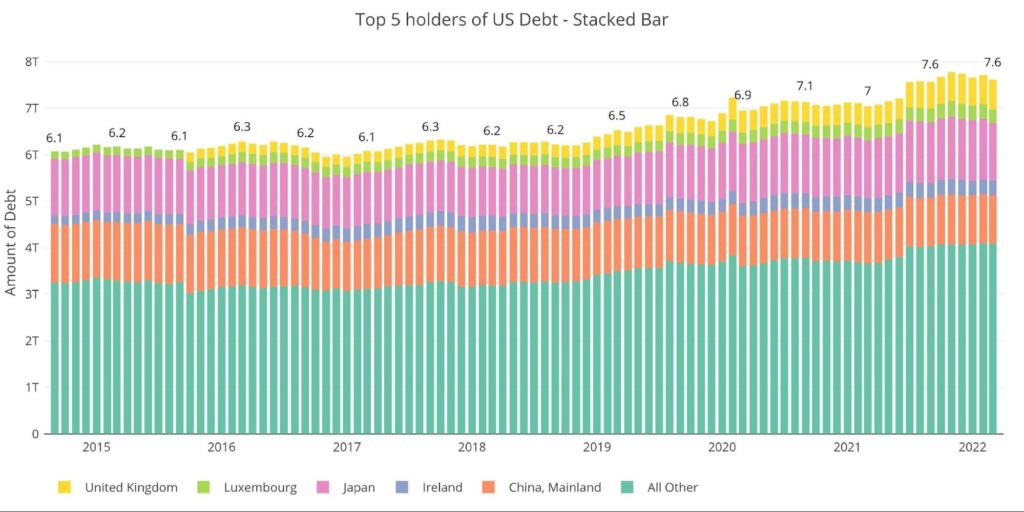

The table below shows how debt holding has changed since 2015 across different borrowers. It’s quite incredible that since Mar 2020, international ownership has increased by about $650B against an increase in total debt that exceeds $7T. International holders absorbed less than 10% of total debt issuance over the last two years.

The Fed filled most of that gap. With Treasury revenues increasing, perhaps everyone feels that the debt is no longer a problem. Complacency could be a very dangerous posture given that a recession could cause a large pullback in tax revenue. Surging interest rates could also prove catastrophic for the Federal budget.

Figure: 10 Average Weekly Change in the Balance Sheet

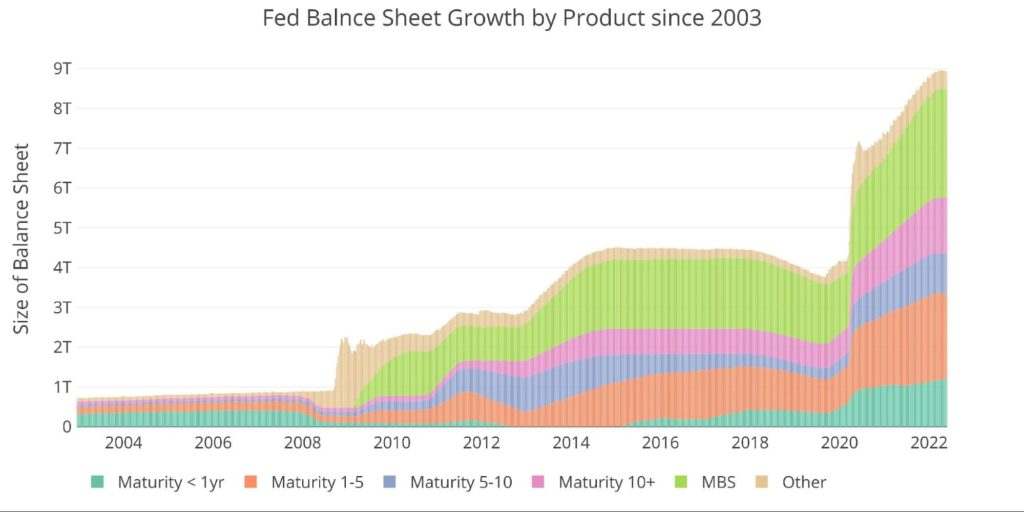

Historical Perspective

The final plot below takes a larger view of the balance sheet. It is clear to see how the usage of the balance sheet has changed since the Global Financial Crisis. The tapering from 2017-2019 can be seen in the slight dip before the massive surge due to Covid.

There is no way the Fed will come close to shrinking the balance sheet at this stage. Most forecasters are suggesting the Fed can get down to $6T before causing serious pain in financial markets, a $3T reduction. This seems laughable given how little it took in 2018 to send the markets into a tailspin (a decrease of $750B).

Furthermore, at the pace of $95B a month, it would take more than 2.5 years to achieve a $3T reduction. This means the Fed would have to continue tightening if a recession hit.

Figure: 11 Historical Fed Balance Sheet

What it means for Gold and Silver

The Fed continues to talk tough but does very little in terms of action. The next two months will be interesting. The Fed is scheduled to raise rates by 100Bps and also begin QT. The stock market has priced in these two moves so far with large sell-offs and much higher volatility. The gold market has also been hit hard after reaching $2003.

Will the Fed succeed in bringing down inflation? Inflation may drop from 8.3%, but it seems very unlikely it will reach 2% before the removal of stimulus really starts to impact the economy. Layoffs have started and the housing market has been under pressure.

The Fed cannot stick to its aggressive trajectory without major ramifications. This may be why the stock market has rallied this week. With GDP coming in weaker than expected, the market may be looking beyond the tightening to the next round of stimulus. Gold has bounced but is still stuck around $1850. That being said, it looks to be building a healthy base and turning fragile support into a stronger foundation for its next big up-move. Once the Fed pivots, that up-move will be swift!

Data Source: https://fred.stlouisfed.org/series/WALCL and https://fred.stlouisfed.org/release/tables?rid=20&eid=840849#snid=840941

Data Updated: Weekly, Thursday at 4:30 PM Eastern

Last Updated: May 25, 2022

Interactive charts and graphs can always be found on the Exploring Finance dashboard: https://exploringfinance.shinyapps.io/USDebt/

Call 1-888-GOLD-160 and speak with a Precious Metals Specialist today!

Buka akaun dagangan patuh syariah anda di Weltrade.

Source link