Please note: the CoTs report was published 10/28/2022 for the period ending 10/25/2022. “Managed Money” and “Hedge Funds” are used interchangeably.

Gold

Current Trends

Managed Money net short is now at 38.8k which is 13k larger than last week but down 5k from the report last month. Swaps also increased net shorts over the month which helped drive total net positioning slightly higher. Despite the slight move higher, the overall market has contracted considerably over the last 6 months.

Figure: 1 Net Position by Holder

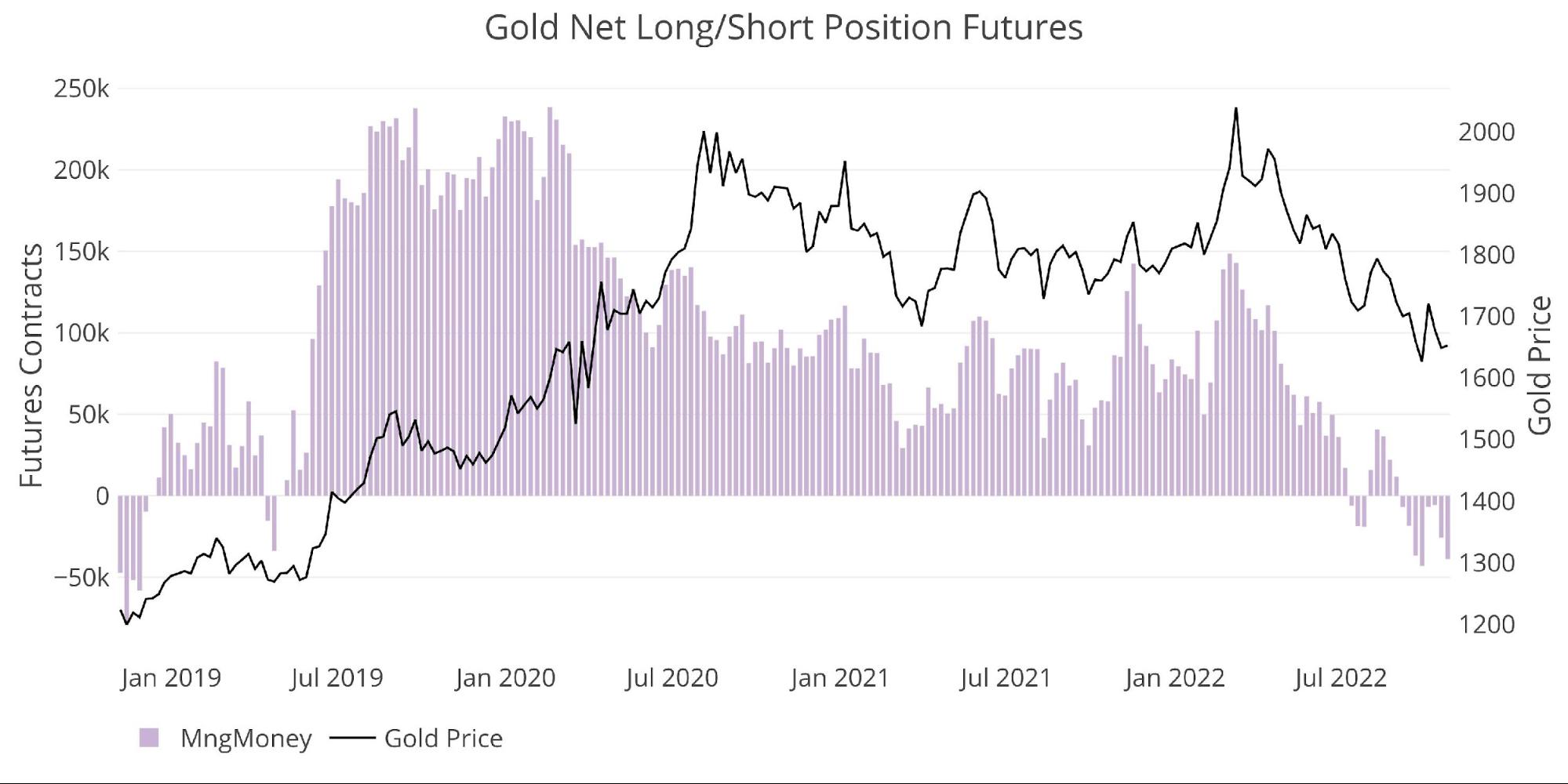

The Managed Money group is in complete control of this market (for now). The chart below shows the close link between Managed Money’s net position and price. The correlation for 2022 is at an incredible 0.95. While correlation is not causation, it’s hard to think the relationship shown below is not causal.

That being said, the last time Managed Money had such a large net short position was back in 2019 when the gold price was $400 lower, so the correlation does not hold over longer periods.

Figure: 2 Managed Money Net Position

Weak Hands at Work

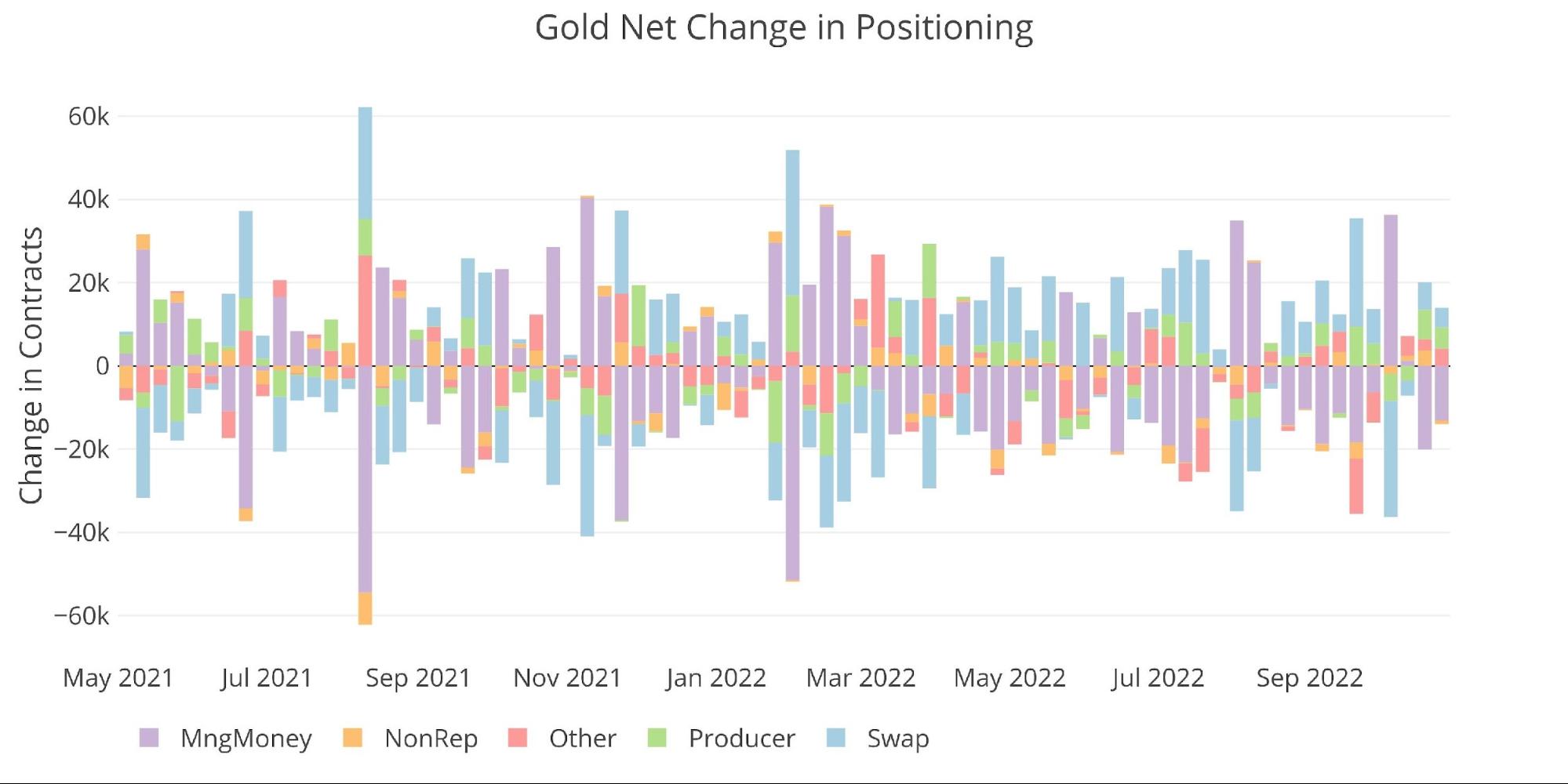

The chart below shows the weekly data. Typically, Managed Money will fluctuate back and forth between long and short. Over the last 34 weeks, it has been a different story. Managed Money has increased net positioning in only 8 weeks against 26 weeks of decreasing net positioning.

This has crushed the gold price from over $2,000 to below $1,700.

Figure: 3 Silver 50/200 DMA

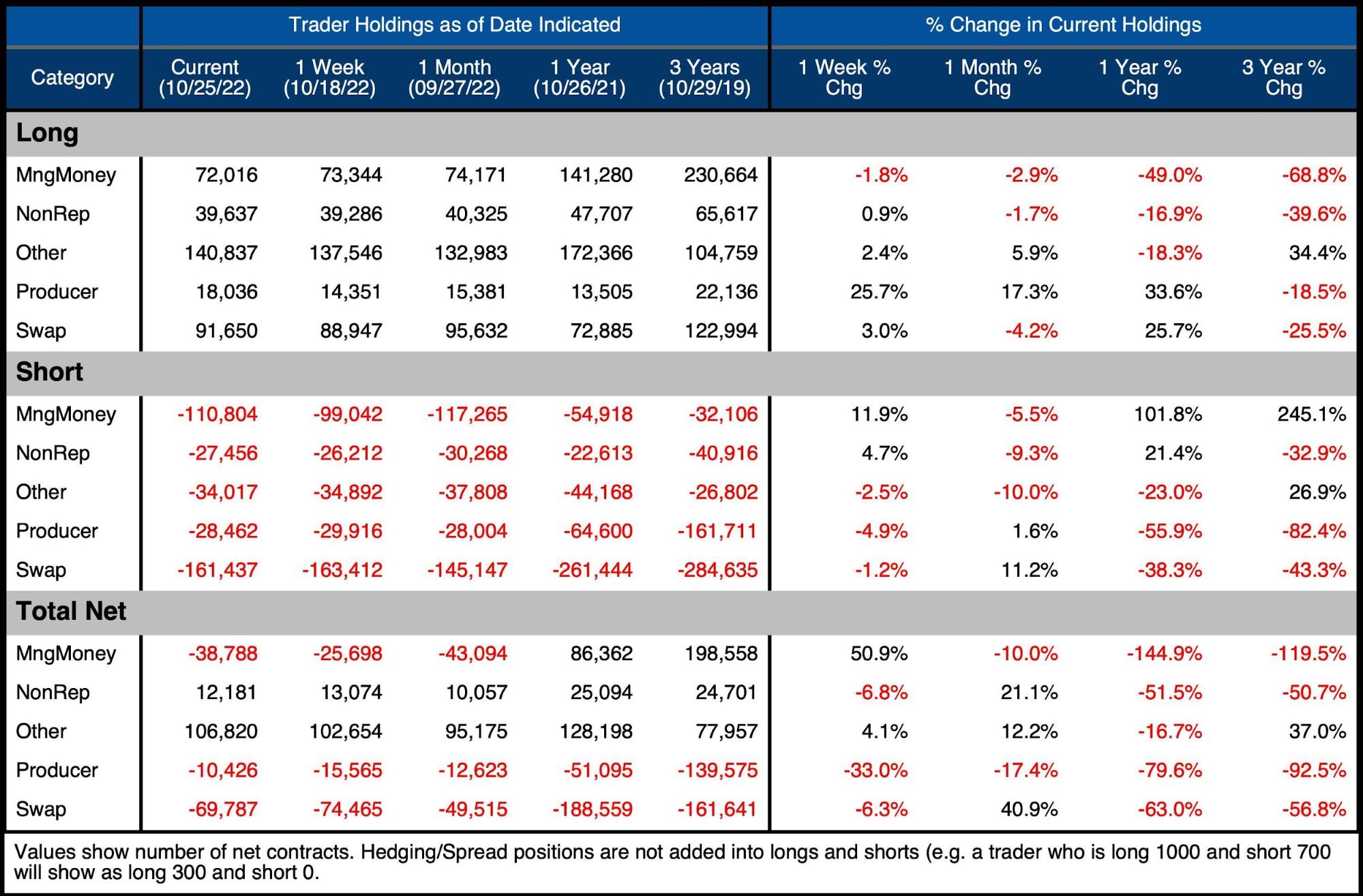

The table below has detailed positioning information. A few things to highlight:

-

- Over the month, Managed Money change was driven mainly by Gross shorts increasing 12% from 99k to 110k

- Over the last year, Managed Money Gross Longs are down 50% while Gross Shorts are up 102%

-

- This has led to a -150% change in overall net positioning

-

- The rest of the players should not be ignored though. Over the last year:

-

- Non-Rep net long is down over 50% (12k)

- Other net long is down almost 17% (22k)

- Producer net short is down 80% (41k)

- Swap net short is down 63% (119k)

-

Every participant has reduced their overall gross positioning, but Managed Money is the only group that has flipped from net long to net short (and in a big way).

One thing to highlight is that over the last year, Managed Money gross shorts have increased 55k contracts (102%). At the same time, the other 4 participants have reduced gross shorts by a combined 142k contracts or 64%.

Figure: 4 Gold Summary Table

So, what is going on? I think a trap is being set!

This is pure speculation, but the physical market is sending very loud signals that supply is disappearing. I think Swaps, Producers, Other, and Non-rep have taken notice and reduced short positioning to get out of the way.

Managed Money plays in the paper market only, trading on technicals. They don’t want or care about physical. Gold was unable to hold any momentum despite high inflation, which means when the Fed started hiking, Managed Money could only see a reason for gold to fall hard. They smelled blood and pounced.

As Managed Money reduced longs and increased shorts, the other four participants (mainly Swaps and Producers) have been able to close out of their shorts without pushing up the price. They have effectively dumped their shorts onto Managed Money.

The overall market has been getting back to neutral as shown in the net positioning chart below. Producers now have their smallest net short position since 2014 at the depths of the gold bear market. So, over the last year, while everyone has been reducing net exposure, Managed Money has gone from 86k net long (198k net long 3 years ago), to ~40k net short.

Eventually, Managed Money will swing back towards long, but will Swaps and Producers step in to provide the liquidity (by going short). This liquidity helps keep the price contained while big moves happen in the futures market. This is why gold has not crashed back to $1300 in the face of incredible selling by Managed Money – Swaps and Producers were liquidating their shorts.

The point is, if the Swaps and Producers (who can see the physical supply constraints) are not willing to step up on the short side, then the price could go much higher when Managed Money swings back. The alternative scenario is that Managed Money stays short, and is then on the hook for delivering out metal to contract holders who are taking delivery. But they don’t have physical, so they would rely on the Comex inventory, which is rapidly drying up.

This chart shows a contraction in net positioning

Figure: 5 Net Positioning

Historical Perspective

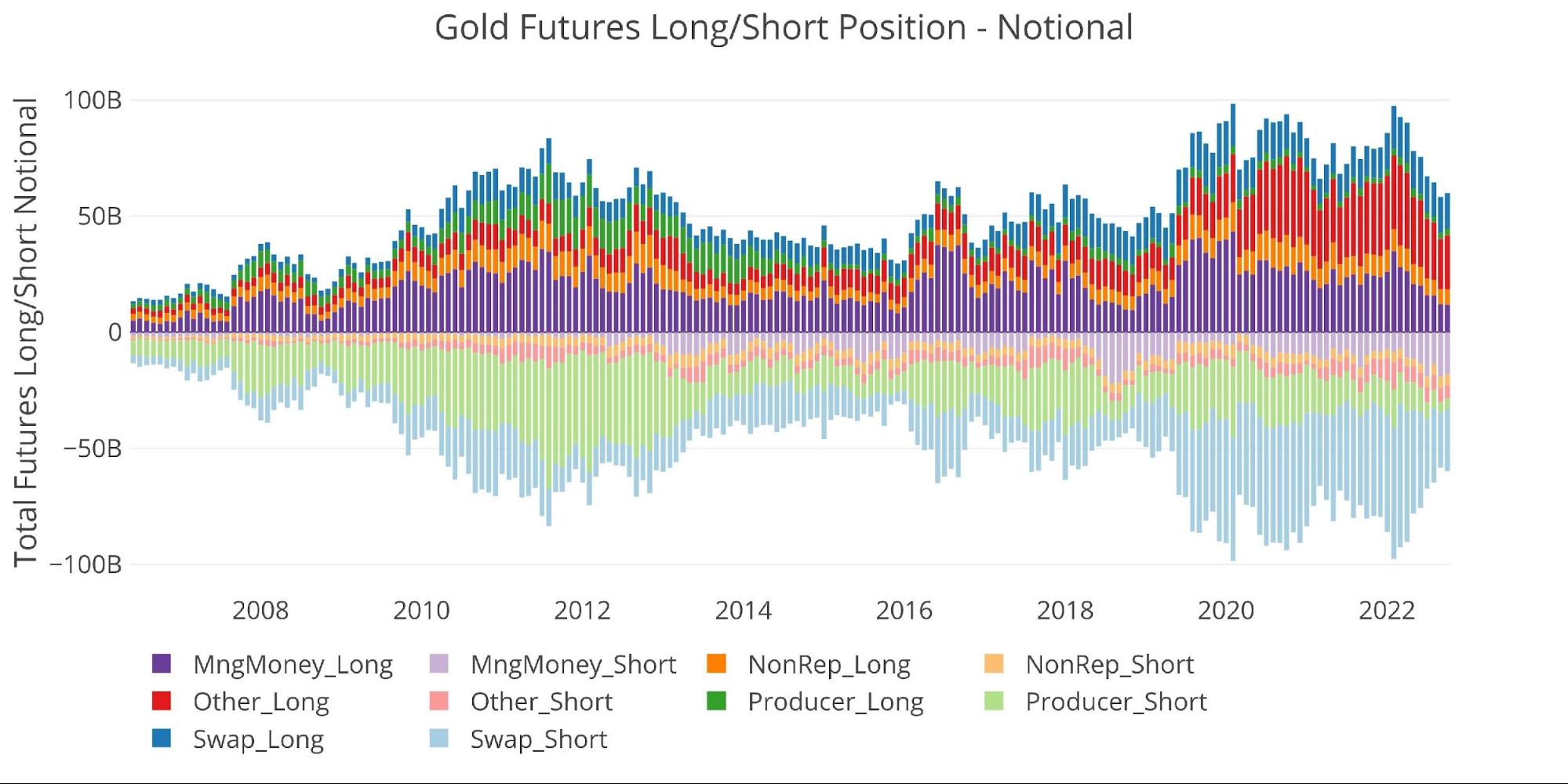

Looking over the full history of the CoTs data by month produces the chart below (values are in dollar/notional amounts, not contracts). There has never been a downward move like the recent one. And this downward move occurred in the face of historically strong physical demand from Comex vaults!

Figure: 6 Gross Open Interest

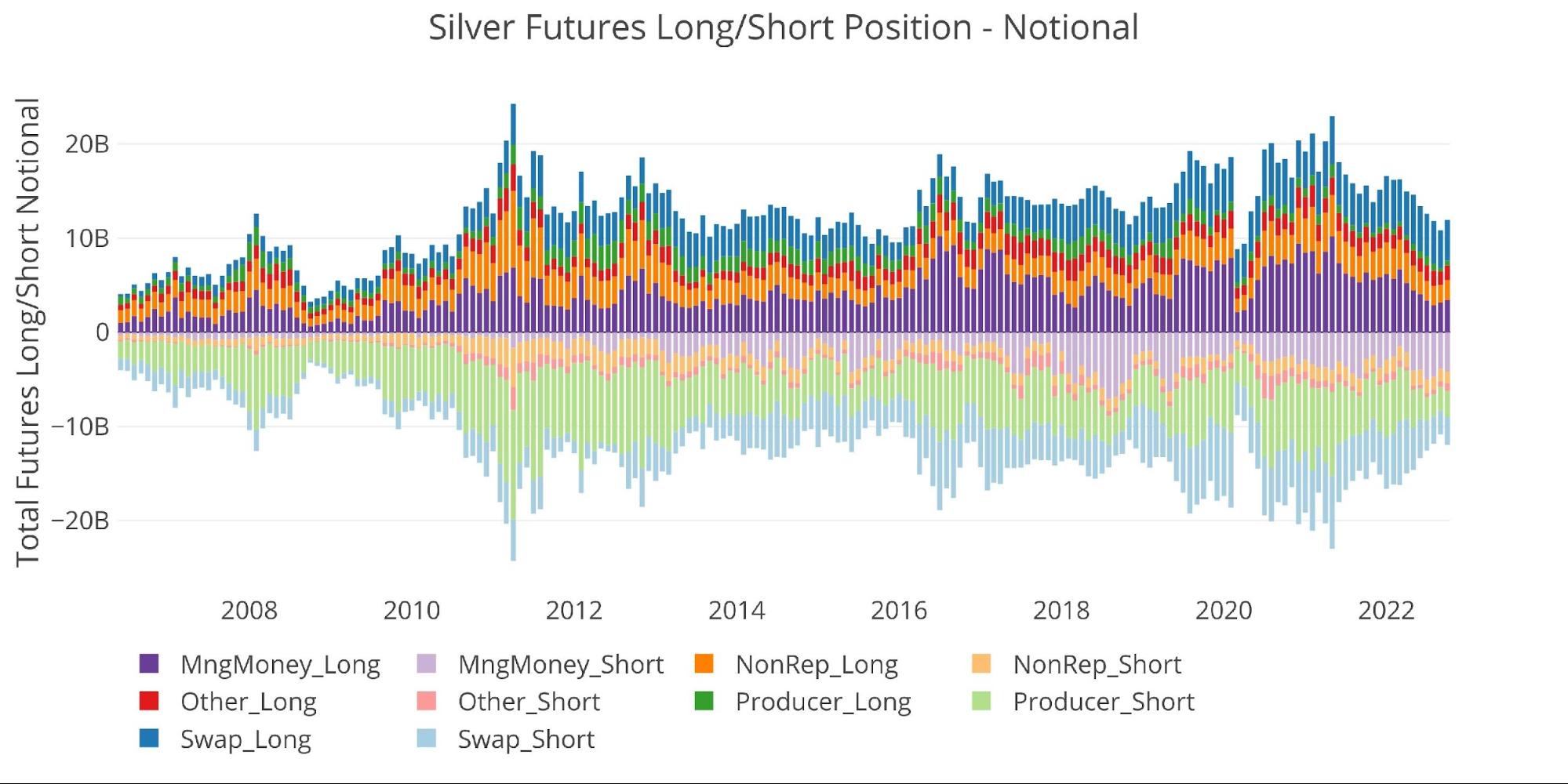

The chart below looks at net notional positioning against price on a longer time frame. Again, the market (colored bars) has recently come crashing down even worse than 2012. At the same time, the price (line) has not had nearly the same reaction as in 2012. the price has held up much better this time.

Figure: 7 Net Notional Position

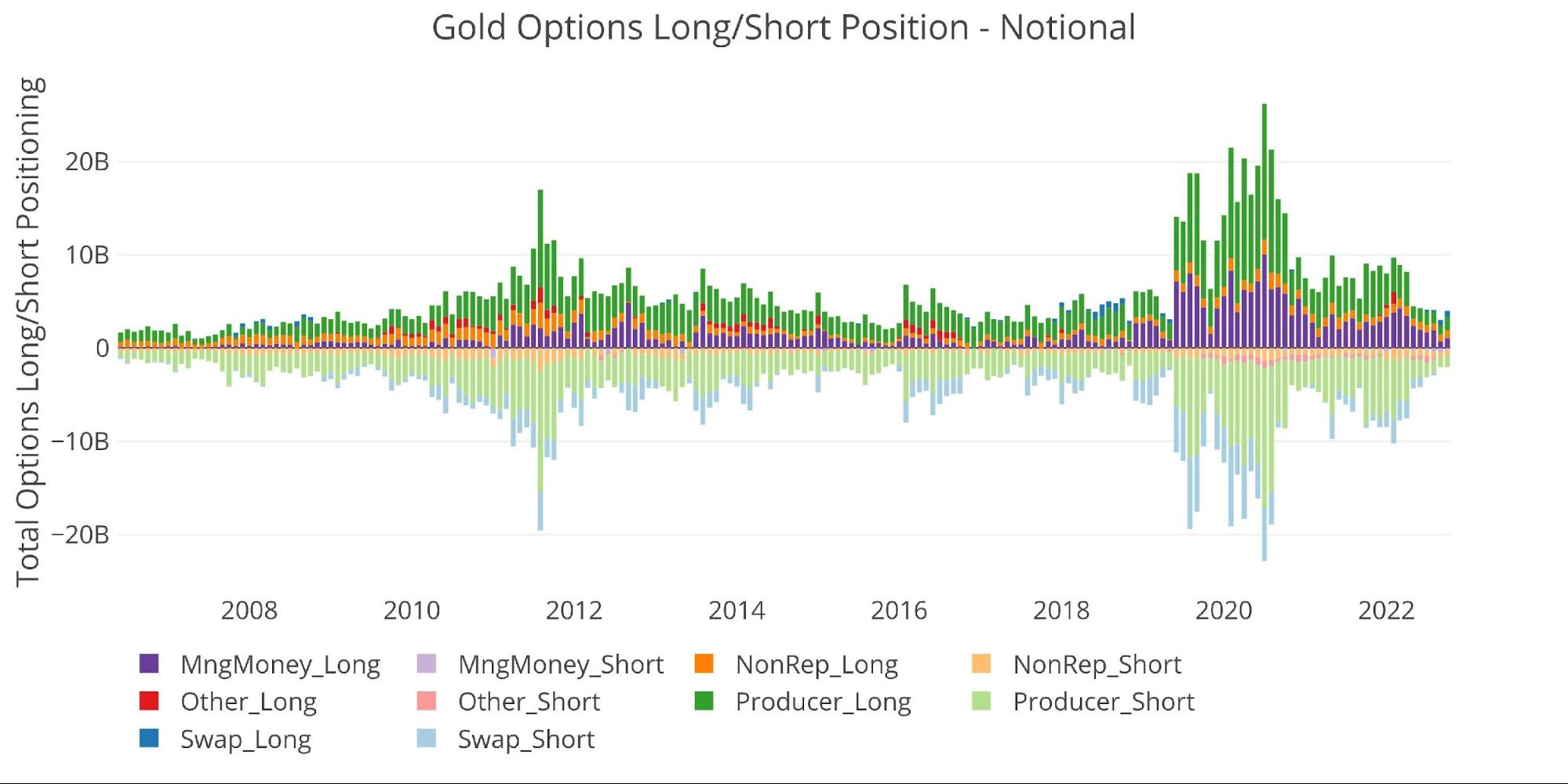

The options market still looks very quiet, which means no one is taking on extra leveraged bets for now.

Figure: 8 Options Positions

Silver

Current Trends

I think the same trap that’s been laid in gold has also been set in silver and is perhaps even further along.

Similar to gold, Managed Money has been a relentless seller of silver. However, unlike gold, Swaps have completely reversed their short position and have been net long in silver since May. Producers are still well net short, with little movement over the last few months.

Figure: 9 Net Position by Holder

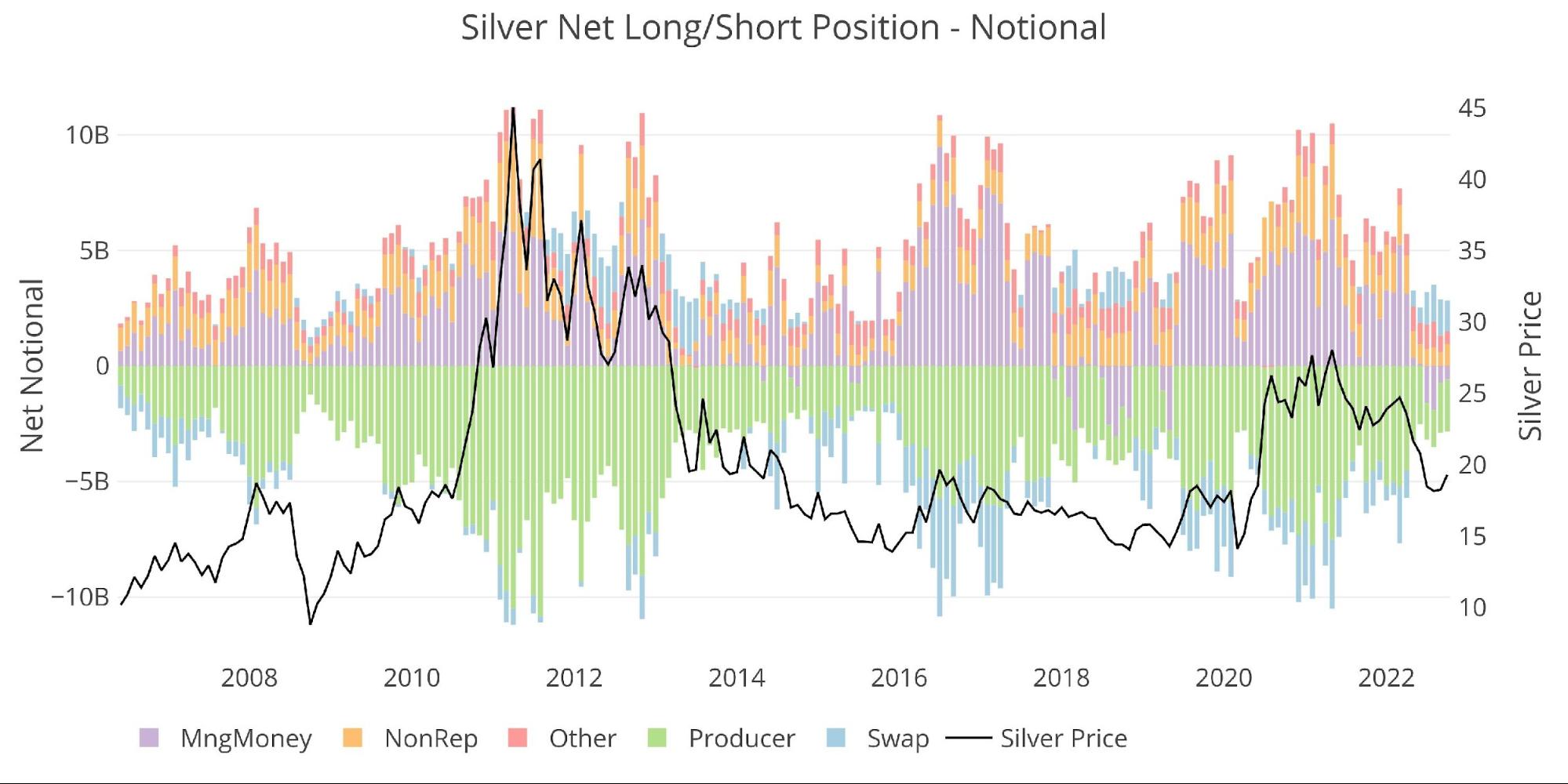

Managed Money net shorts have been mostly stable in Silver for a few months except for a brief reversal to net positive in early October which also sent the price over $21 very quickly. This shows how much control Managed Money has over price and how quickly things can move.

Figure: 10 Managed Money Net Position

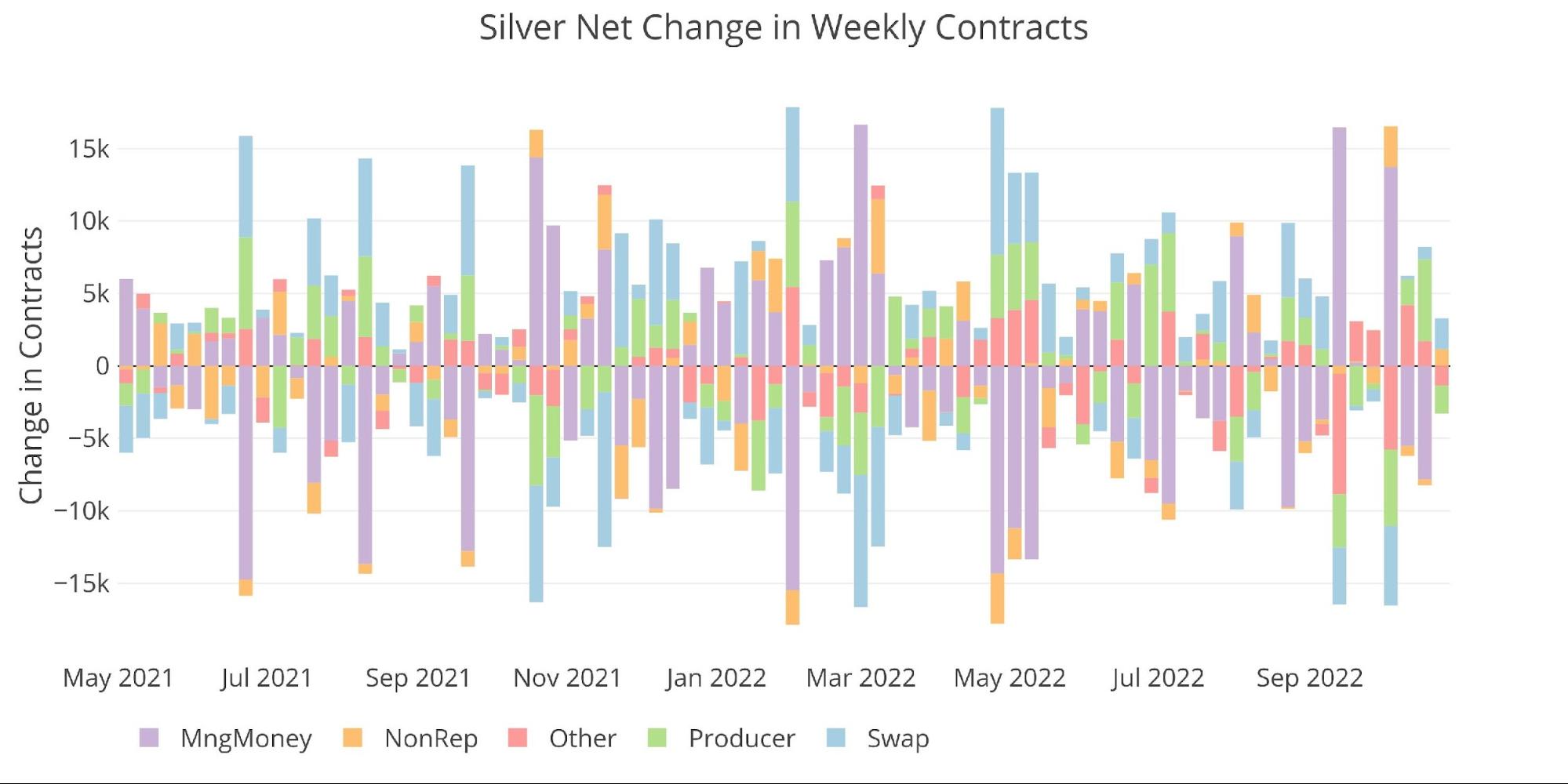

The trading by Managed Money has been a bit more erratic in gold as shown below.

Figure: 11 Net Change in Positioning

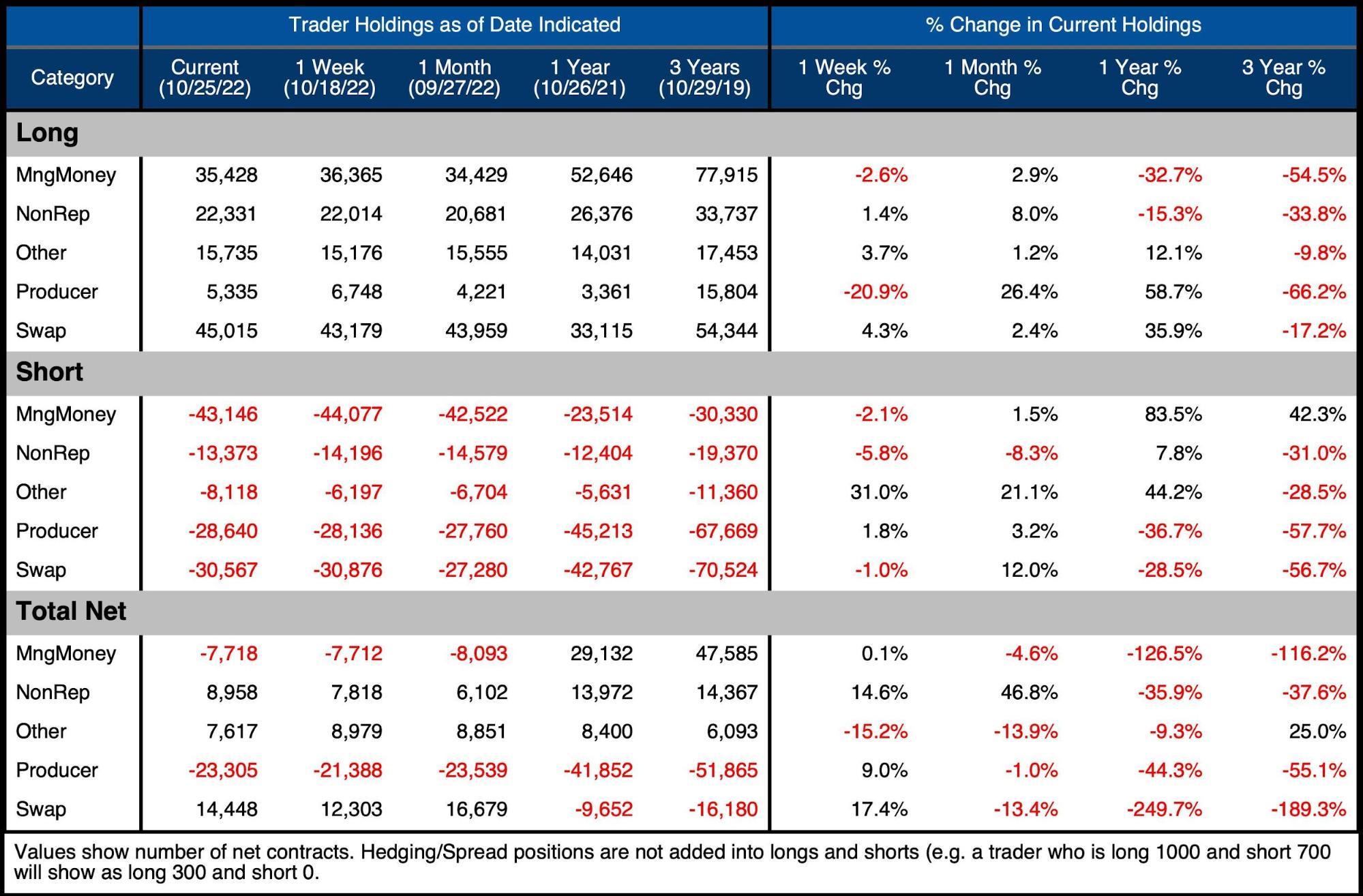

The table below shows a series of snapshots in time. This data does NOT include options or hedging positions. Important data points to note:

-

- Over the last year, Managed Money Net positioning went from long to short, changing by -126%

-

- This was driven by a reduction in longs by 32.7% and increase in shorts by 83.5%

-

- Over the last year, Managed Money Net positioning went from long to short, changing by -126%

Similar to gold, Managed Money has increased their gross short substantially (83% or 20k contracts), while the other four combined have reduced their gross shorts by 24% or 25k contracts. Again, this has been driven by Swaps and Producers.

Figure: 12 Silver Summary Table

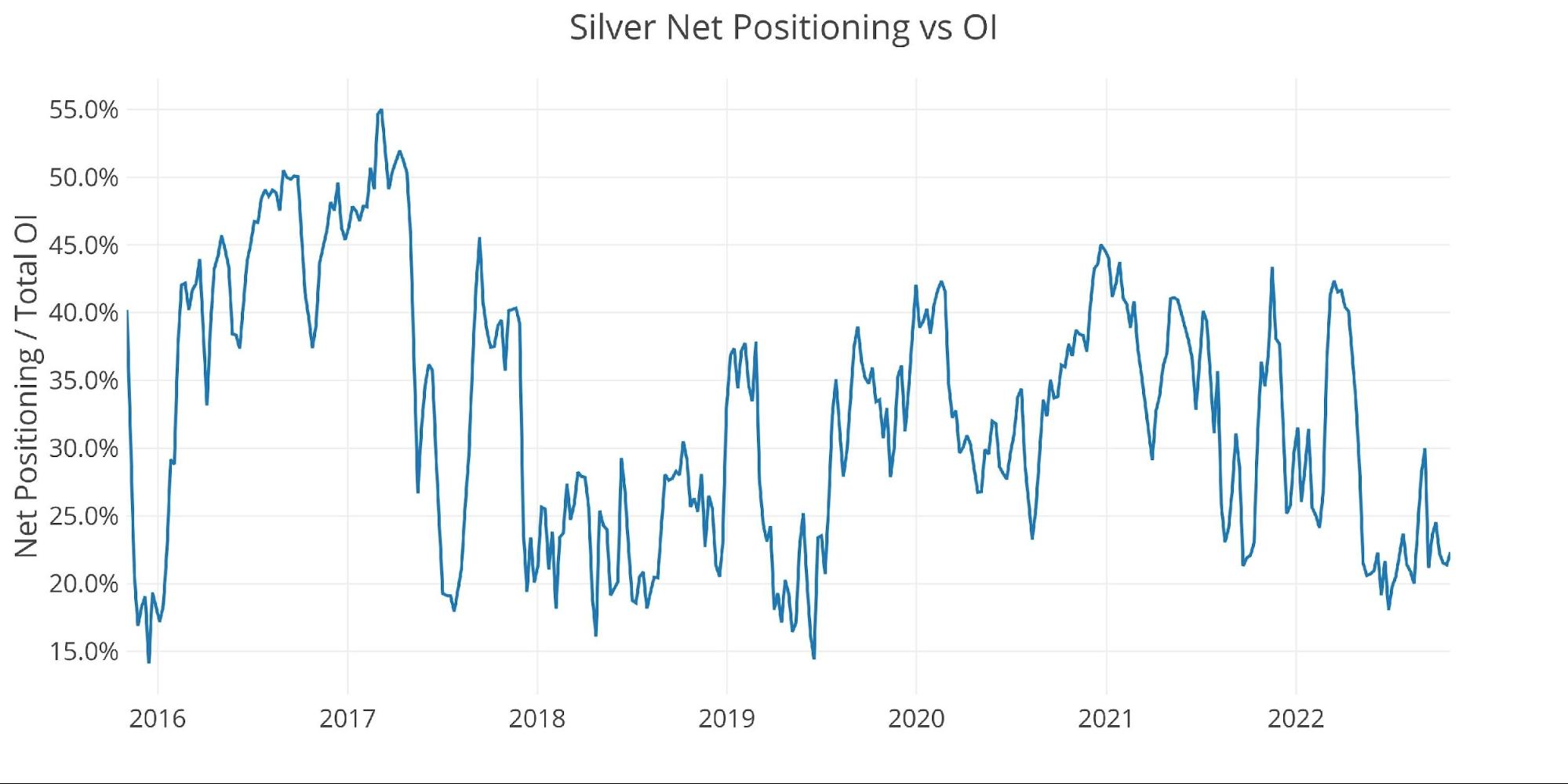

Net positioning as a percent of total open interest remains low relative to the last few years.

Figure: 13 Net Positioning

Historical Perspective

Looking over the full history of the CoTs data by month produces the chart below. The overall market has been contracting in recent months to multi-year lows.

Figure: 14 Gross Open Interest

Looking at historical net positioning shows that Managed Money has never held a net short position for longer than 5 consecutive month-end periods, which it did back in 2018. October 2022 just completed month four of being net short despite a mid-month burst into positive territory. With the Fed dropping hints of a pivot, Managed Money will likely turn around soon for more than just a short burst. Given how quickly the price reversed in early October, this could be setting up for a spectacular rise in price in short order if Managed Money decides they need to get back to a long position.

Figure: 15 Net Notional Position

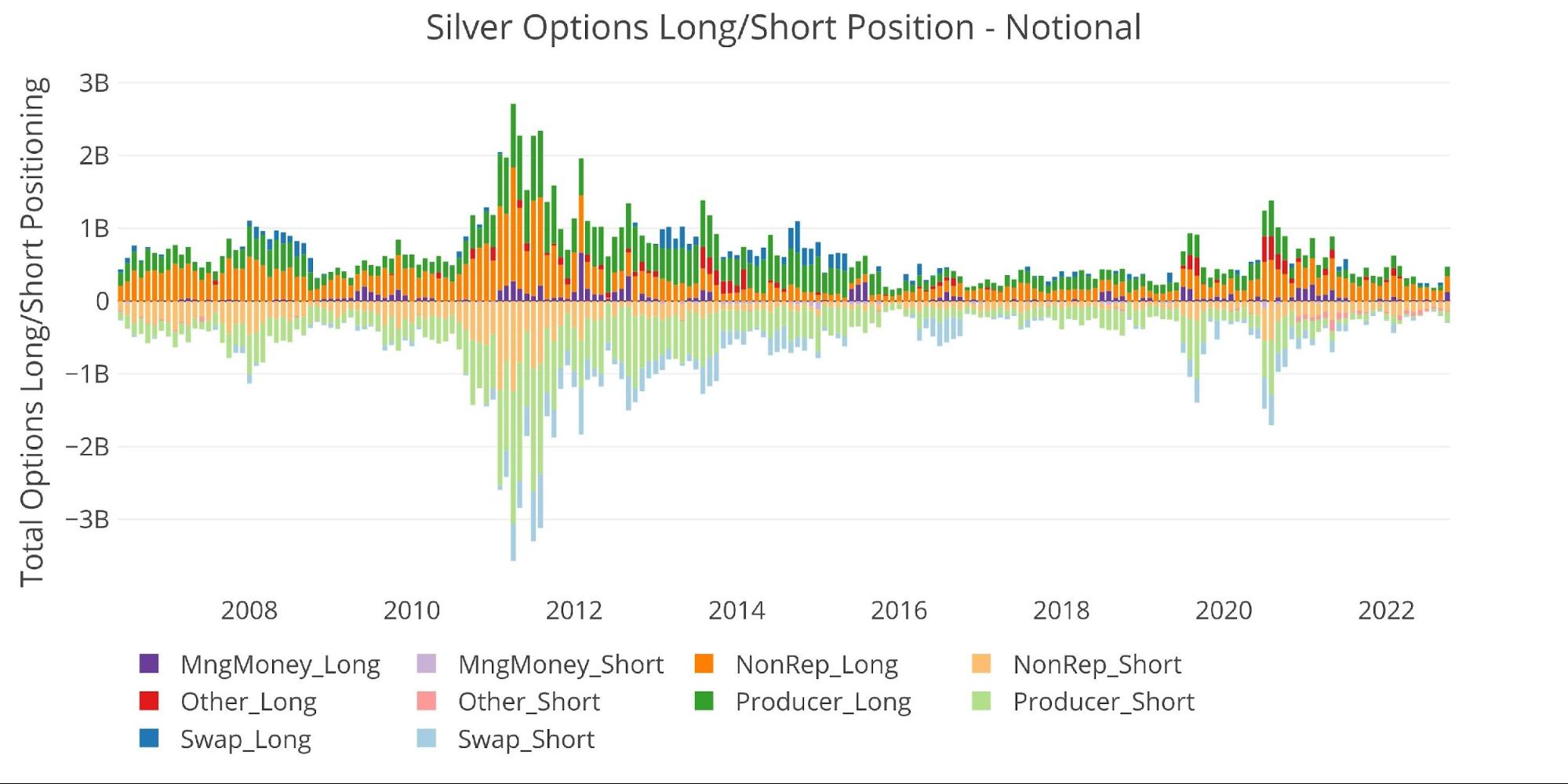

Perhaps this is why Managed Money has actually taken on its biggest net long position within the options market since May 2021. Are they front-running their move?

Figure: 16 Options Positions

Conclusion

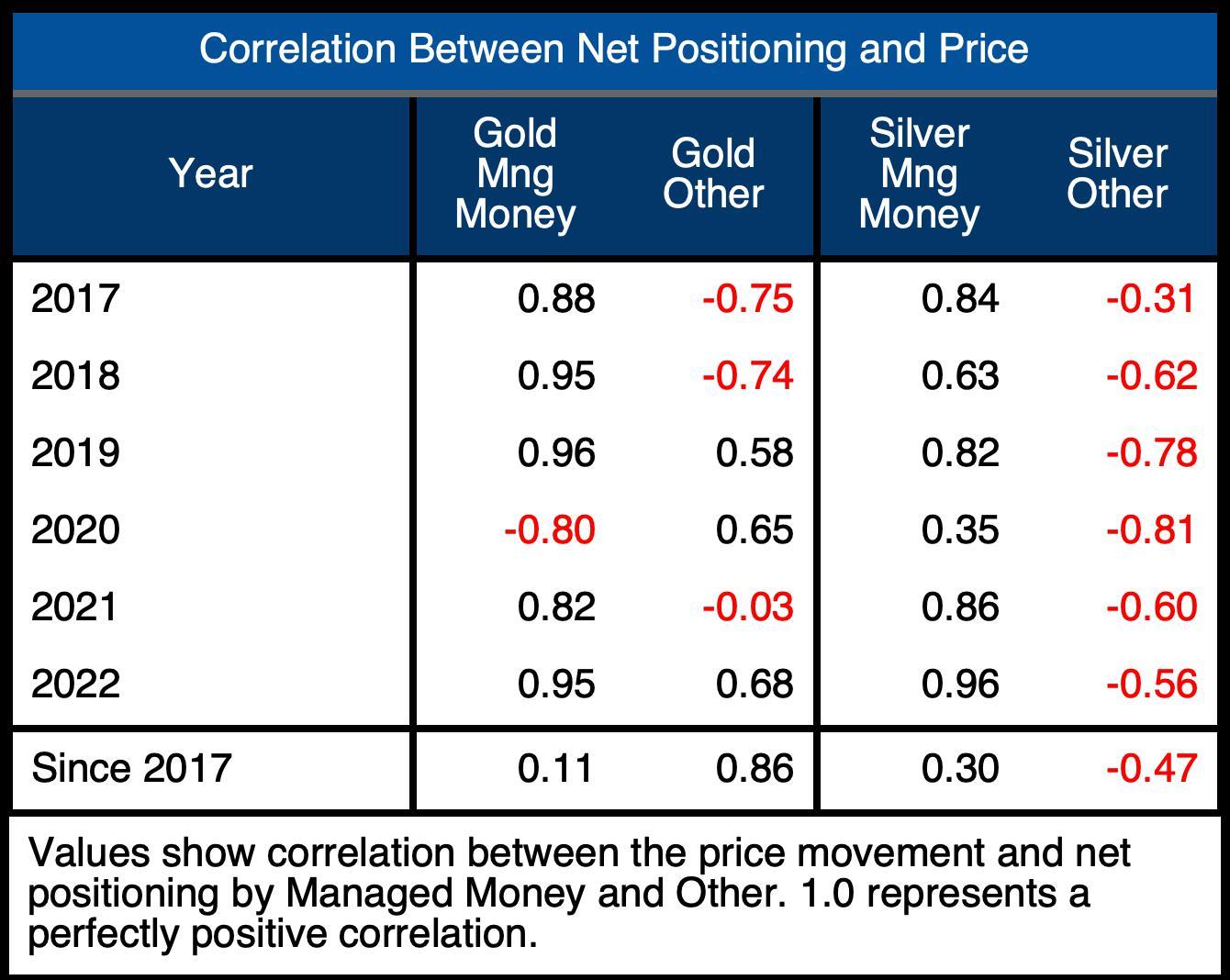

Managed Money continues to dominate control over the market. Looking at the correlation table below shows gold at .95 and silver at an incredible .96. This is complete control over the market.

Figure: 17 Correlation Table

However, what if this has given a false sense of confidence? Given the recent massive exodus of metal from Comex vaults, physical supply is running thin. This could lead to a short squeeze in the physical market that spills over into the paper market, creating a blood bath for paper shorts.

The Fed might be dialing back the hawkish talk this week which could be the soft pivot that marks a bottom in the gold and silver market. With Managed Money positioned for a big down move in metals, they may have to cover quickly if the price starts to rebound. If Swaps and Producers don’t want to re-enter the ring on the short side due to supply constraints, the price of metals could move up dramatically.

While the market may need a bit more time to get its footing, when it does, the landscape is perfectly set up for a massive move-up in price.

Data Source: https://www.cftc.gov/MarketReports/CommitmentsofTraders/index.htm

Data Updated: Every Friday at 3:30 PM as of Tuesday

Last Updated: Oct 25, 2022

Gold and Silver interactive charts and graphs can be found on the Exploring Finance dashboard: https://exploringfinance.shinyapps.io/goldsilver/

Call 1-888-GOLD-160 and speak with a Precious Metals Specialist today!

Buka akaun dagangan patuh syariah anda di Weltrade.

Source link