(Bloomberg) — Sign up for the New Economy Daily newsletter, follow us @economics and subscribe to our podcast.

Most Read from Bloomberg

Jerome Powell’s first four years as Federal Reserve chair were defined by saving the U.S. economy from the historic challenge of the pandemic. His second term — and his legacy — will be about saving the economy from overheating.

Powell and his colleagues on the Federal Open Market Committee, who meet Tuesday and Wednesday, are wrestling with how to quell the highest inflation in a generation without stalling labor market gains.

The risks of error in this quest for a soft landing are big: move too fast and the economy tips back into recession. Go too slow and inflation gets entrenched.

Powell’s emergency support of financial markets in 2020 as Covid-19 spread helped stage a solid recovery in 2021. The 68-year-old’s dexterity won backing from both parties and ultimately his nomination by President Joe Biden to a second term.

Now, “that legacy is being challenged” by inflation that’s too high and the Fed’s response which to some appears too slow, said Tim Duy, chief economist at SGH Macro Advisors. “It is going to be hard to glide path prices back to the 2% target” quickly without inducing a recession.

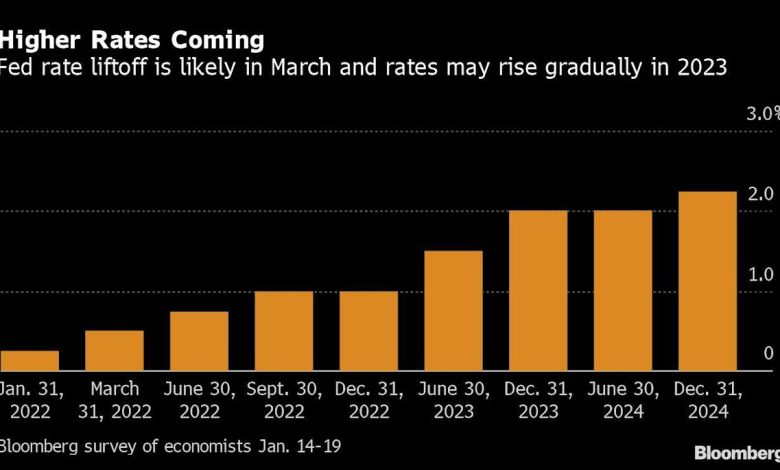

Officials are expected to signal a rate hike in March after their meeting ends Wednesday. But Powell may need to open the door to more increases this year than the three projected in their December forecasts. Some urge that Powell suggest that every meeting is live for a potential rate hike if warranted.

He will have to balance that message with the Fed’s commitment to a new framework that pledges to let the labor market to run hot in pursuit of broad-based and inclusive gains. There is also the issue of financial market fragility. The S&P 500 has slid more than 7% since the end of last year, in part because of nerves surrounding the Fed’s tightening.

Plus, U.S. central bankers are operating in a very different inflation climate than the last time they lifted interest rates from near zero, in December 2015. Back then, the Fed’s preferred inflation index rose by 0.2% over the prior 12 months, compared to 5.7% in the most recent reading.

As the Fed chair prepares for his first press conference of the year, critics see two pressing areas for more clarity: the pace of rate increases and the balance sheet.

One hitch in Fed communication is that officials talk a lot about their baseline projection. They don’t have a good way to describe their collective response to a rapidly evolving outlook, and they refresh their forecasts only once a quarter.

Right now, their baseline from December doesn’t look fully credible, says Anna Wong, chief U.S. economist for Bloomberg Economics.

“They have the unemployment rate falling to 3.5% this year, below their long-run sustainable rate, and staying there in the next two years, and yet inflation drifts down back down to 2.1% in 2024,” she said.

Meanwhile, they forecast their policy rate would rise to just above 2% — not even reaching what they view as restrictive territory.

“Despite retiring the word ‘transitory’ that forecast still suggests that they think inflation is mostly supply driven and will go away on its own,” said Wong, who forecasts the Fed will have to raise the benchmark policy rate five times this year.

Some officials are starting to publicly second guess their December estimates.

St. Louis Fed President James Bullard says that it might take four increases to slow down prices instead of three as he had thought. Governor Chris Waller argued three hikes was still his baseline forecast, but cautioned that four or even five moves in 2022 may be needed if inflation fails to abate as expected.

With the committee already shifting, Powell has a chance at his Wednesday press conference to open the door to a rate path with more than three increases this year.

He could even dislodge the idea that hikes only happen quarterly by suggesting that every meeting — there are seven more scheduled in 2022 following this week’s gathering — is potentially live for a move.

Investors have already priced in four increases for this year with the first in March. Some say they could do more, including Goldman Sachs Group Inc. who sees “a risk that the FOMC will want to take some tightening action at every meeting” until inflation is cooled.

Minutes from the December meeting showed a consensus among Fed officials on running off their balance sheet not long after rate liftoff. Powell said earlier this month that the committee wants to move “a little faster” and said more clarity is coming.

Officials say that shrinking their balance sheet will put some upward pressure on longer-term borrowing costs. That tightens financial conditions and works a bit like a conventional rate hike, though the exact impact is hard to judge.

The Fed chair might spell out how the tightening of financial conditions through balance sheet runoff meshes with rate increases — one way perhaps to explain the moderate pace of tightening in their December outlook.

“There is a consensus that the committee wants to get a plan of quantitative tightening in the right place so it is part of the policy mix,” said Julia Coronado, partner at MacroPolicy Perspectives LLC. “There is less consensus around equivalency with rate hikes” or its impact on financial conditions, she added.

Fed Credibility

Powell has repeatedly said that policy makers need to be nimble as they adjust to an economy that’s responding in unexpected ways during the pandemic. That reflects some hard-won lessons over the last year.

Central bankers insisted for months that price surges would be temporary as demand shifted from goods to services and supply constraints eased. But consumer prices marched higher, reaching 7% last month — the most in almost four decades. Even Biden is telling the central bank to start fighting inflation and normalize policy.

Some question if the Fed behind is the curve and whether Powell will adjust.

“They sure seemed to have dragged their feet in response to their inflation threat,” said Mark Spindel, chief investment officer at MBB Capital Partners. “Are they hard wired to move gradually?”

Most Read from Bloomberg Businessweek

©2022 Bloomberg L.P.

Source link