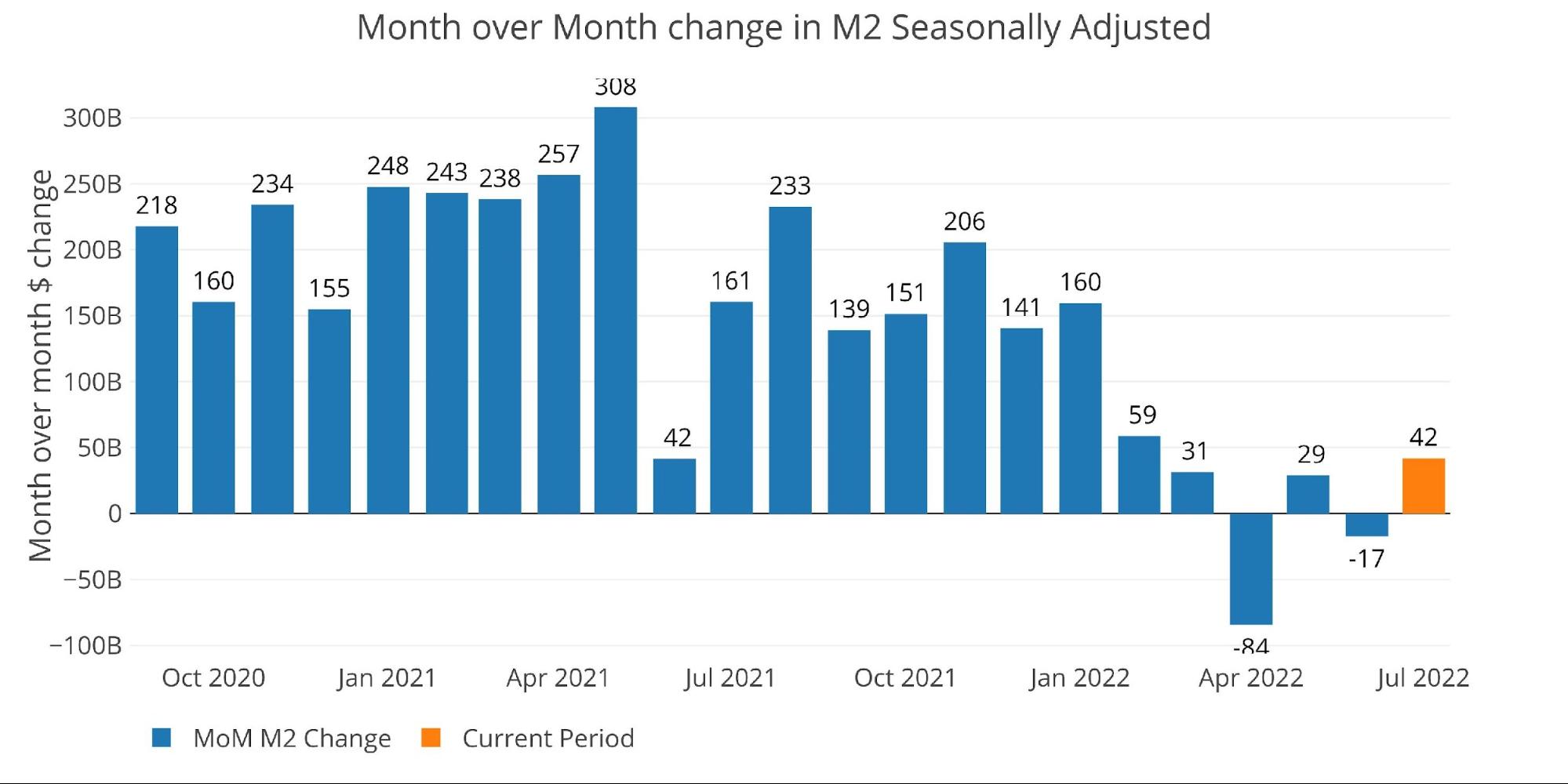

Money Supply growth was positive in July at $42B but sits well below the $161B seen last year. As the chart below shows, Money Supply growth has collapsed since February. Last year started with 5 straight months above $200B whereas 2022 has only seen one month above $100B and that was January.

Figure: 1 MoM M2 Change (Seasonally Adjusted)

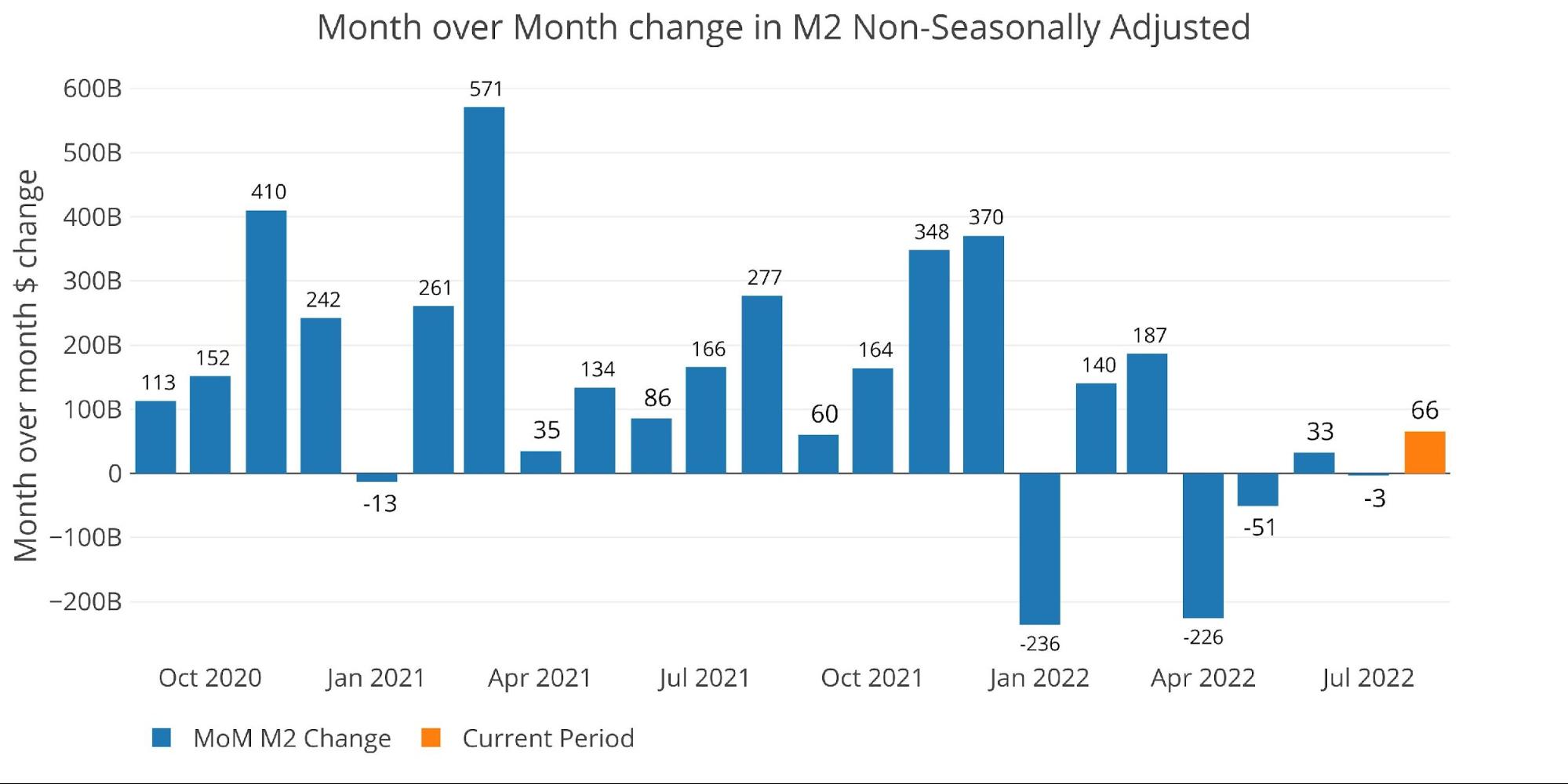

Figure 2 below shows non-seasonally adjusted money supply which is a bit more erratic. Even with the increased volatility, it is very clear that there is far more weakness in the Money Supply in recent months.

Figure: 2 MoM M2 Change (Non-Seasonally Adjusted)

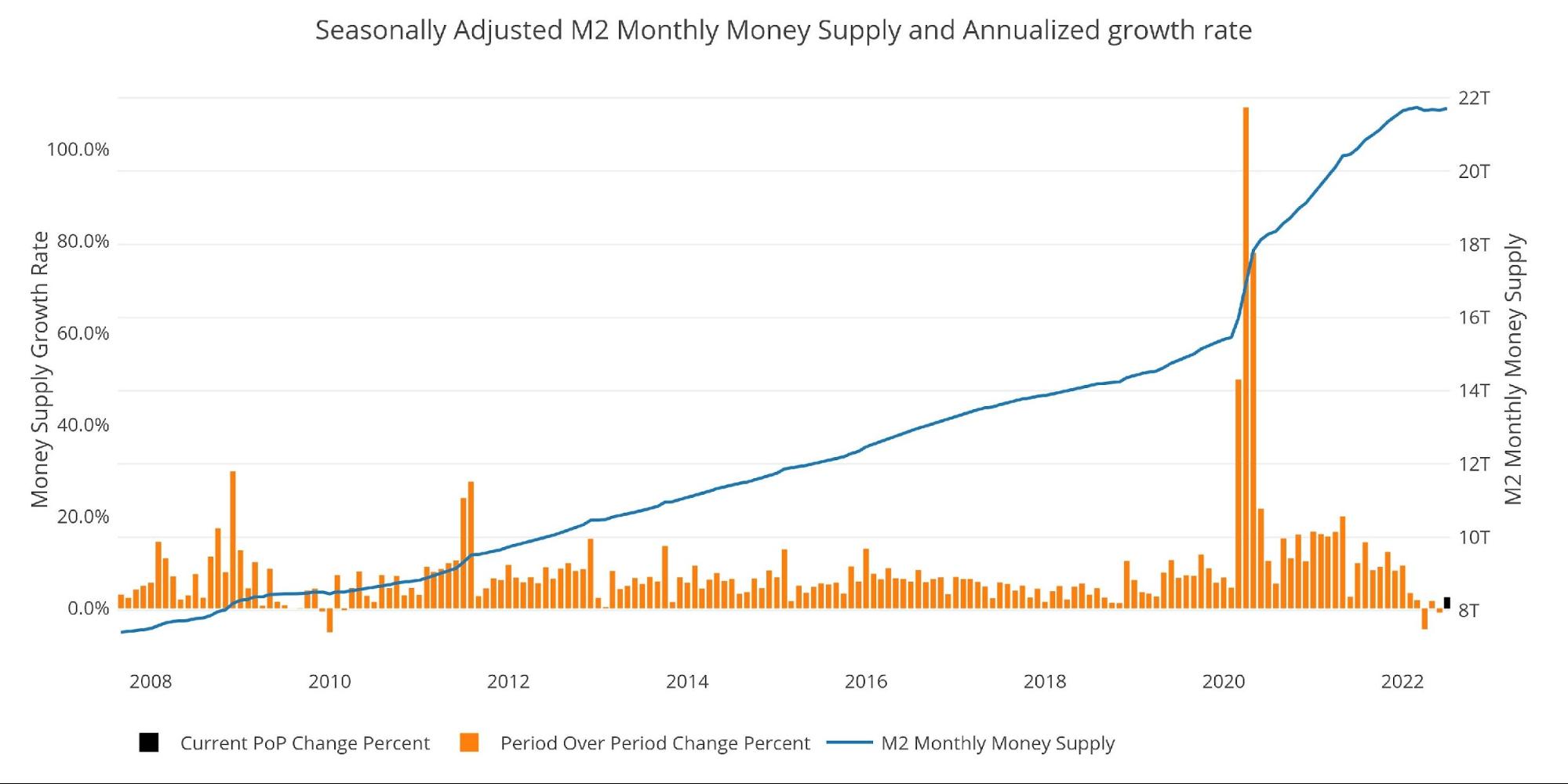

Despite the recent trends, the latest month is actually above the 6-month average growth rate (2.3% VS 0.6%). this still represents less than half the 1-year growth rate of 5.3% and well below the three-year annualized growth rate of 13.5%.

Figure: 3 M2 Growth Rates

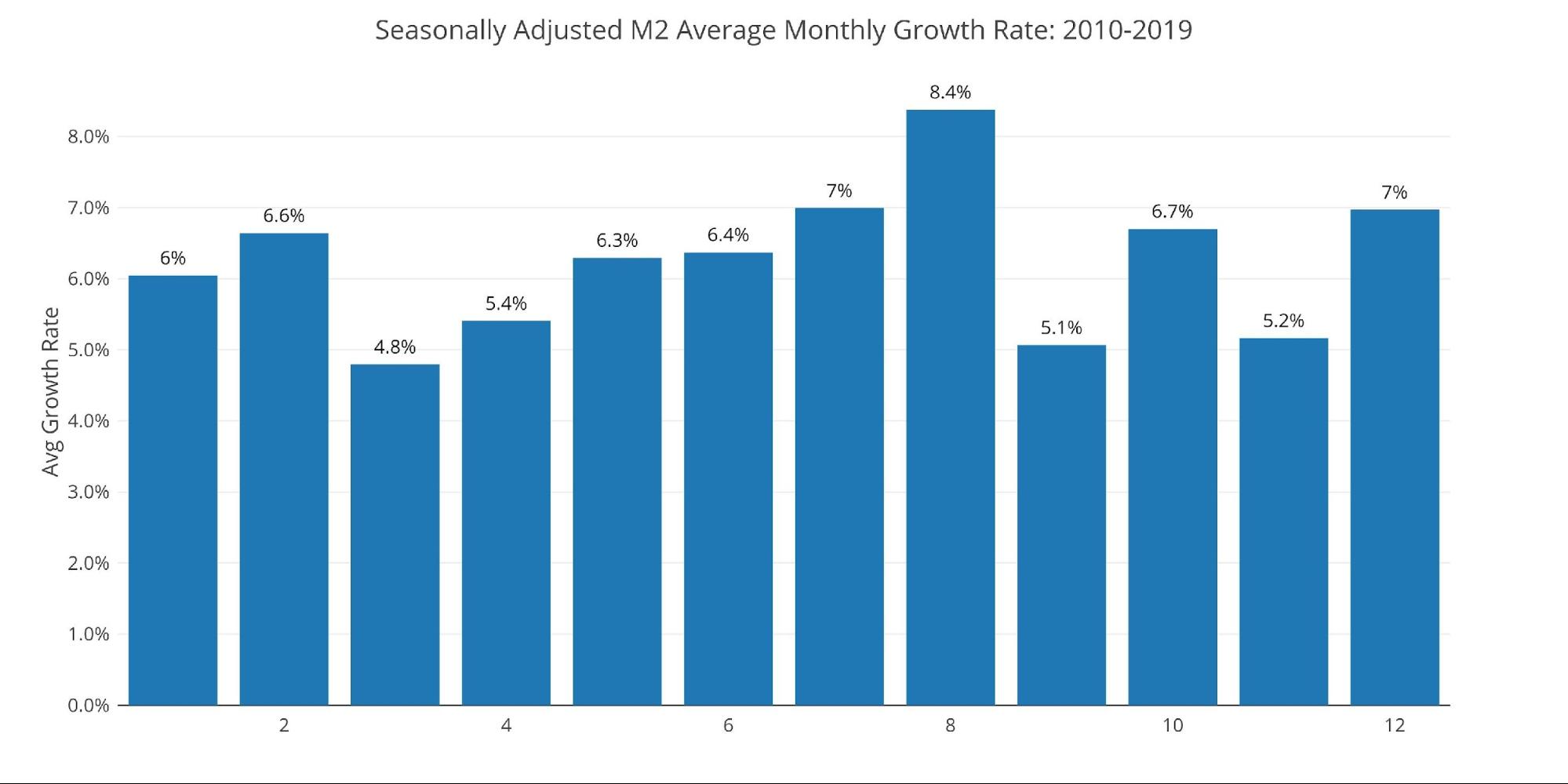

When looking at the average monthly growth rate, before Covid, July historically expands at an annualized 7%. This compares to 2.3% for the current month.

Figure: 4 Average Monthly Growth Rates

The Fed only offers weekly data that is not seasonally adjusted. As the chart below shows, we have been seeing more frequent weeks of negative growth. When growth is positive, it’s much lower than it has been in the recent past.

Figure: 5 WoW M2 Change

The “Wenzel” 13-week Money Supply

The late Robert Wenzel of Economic Policy Journal used a modified calculation to track Money Supply. He used a trailing 13-week average growth rate annualized as defined in his book The Fed Flunks. He specifically used the weekly data that was not seasonally adjusted. His analogy was that in order to know what to wear outside, he wants to know the current weather, not temperatures that have been averaged throughout the year.

The objective of the 13-week average is to smooth some of the choppy data without bringing in too much history that could blind someone from seeing what’s in front of them. The 13-week average growth rate can be seen in the table below. Decelerating trends are in red and accelerating trends in green.

Growth has now collapsed to -2.57% which is the lowest reading since April 1993. This is also the 29th week of negative or zero growth in Money Supply.

Figure: 6 WoW Trailing 13-week Average Money Supply Growth

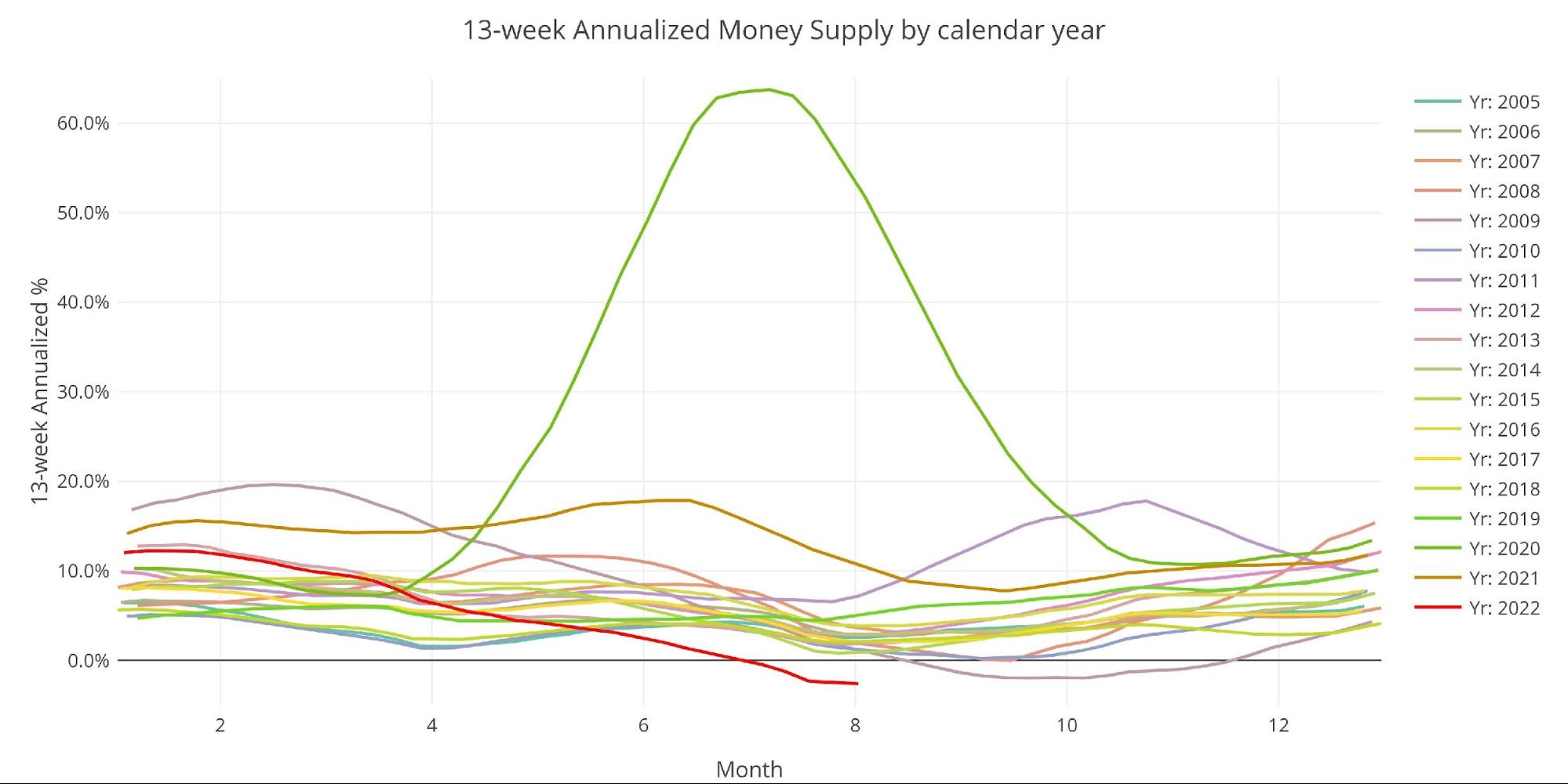

The plot below helps show the seasonality of the Money Supply and compares the current year (red line) to previous years. For the month of August, this is the slowest 13-week Money Supply growth ever recorded.

The chart below goes back to 2005 and the current growth rate is below every single period on the chart and well below any other data point for this time of year.

Wenzel often commented on his ability to guess the timing of the 2008 stock market crash based on the Money Supply that year falling from 11.6% to 0% in a matter of months. In 2022, growth has slowed from 12.2% to -2.5% in less than 6 months. Not to mention the collapse from 64% seen in 2020.

This is a major slowdown in Money Supply and could pose significant headwinds for the stock market and economy.

Figure: 7 Yearly 13-week Overlay

Behind the Inflation Curve

To combat rising prices, the Fed would need to undo most of the money it has created over the last several years. This would require bringing interest rates above the rate of inflation.

Unfortunately, the chart below shows that the Fed has never been further behind the inflation curve. A recession on its own will not cure this inflation problem because of the lagged effects. Looking at the period of 1970, inflation always moved higher on a delay after significant expansion in the money supply. Price increases are still waiting to feel the full effects of all the M2 growth from 2020 and 2021. Furthermore, history shows it required rates higher than inflation to bring prices back down.

The blue line below (Fed Funds Rate) has almost always gotten above the black line (CPI) to force inflation back down. The one anomaly was in 2011 after the Great Recession. The mainstream is now assuming this is the norm (i.e., a recession alone will slow inflation), but the chart below shows that it’s far more common that interest rates must exceed inflation to bend the curve back down. The recent period has made the Fed complacent. This is very dangerous!

Figure: 8 YoY M2 Change with CPI and Fed Funds

Historical Perspective

The charts below are designed to put the current trends into a historical perspective. The orange bars represent annualized percentage change rather than raw dollar amount. The current slowdown can be seen on the right side.

If a few months of M2 slowdown can cause this much pain across the economy (stock market, real estate, bond yields, etc.), how much carnage would unfold in a prolonged fight against inflation where M2 had to shrink consistently for months?

Figure: 9 M2 with Growth Rate

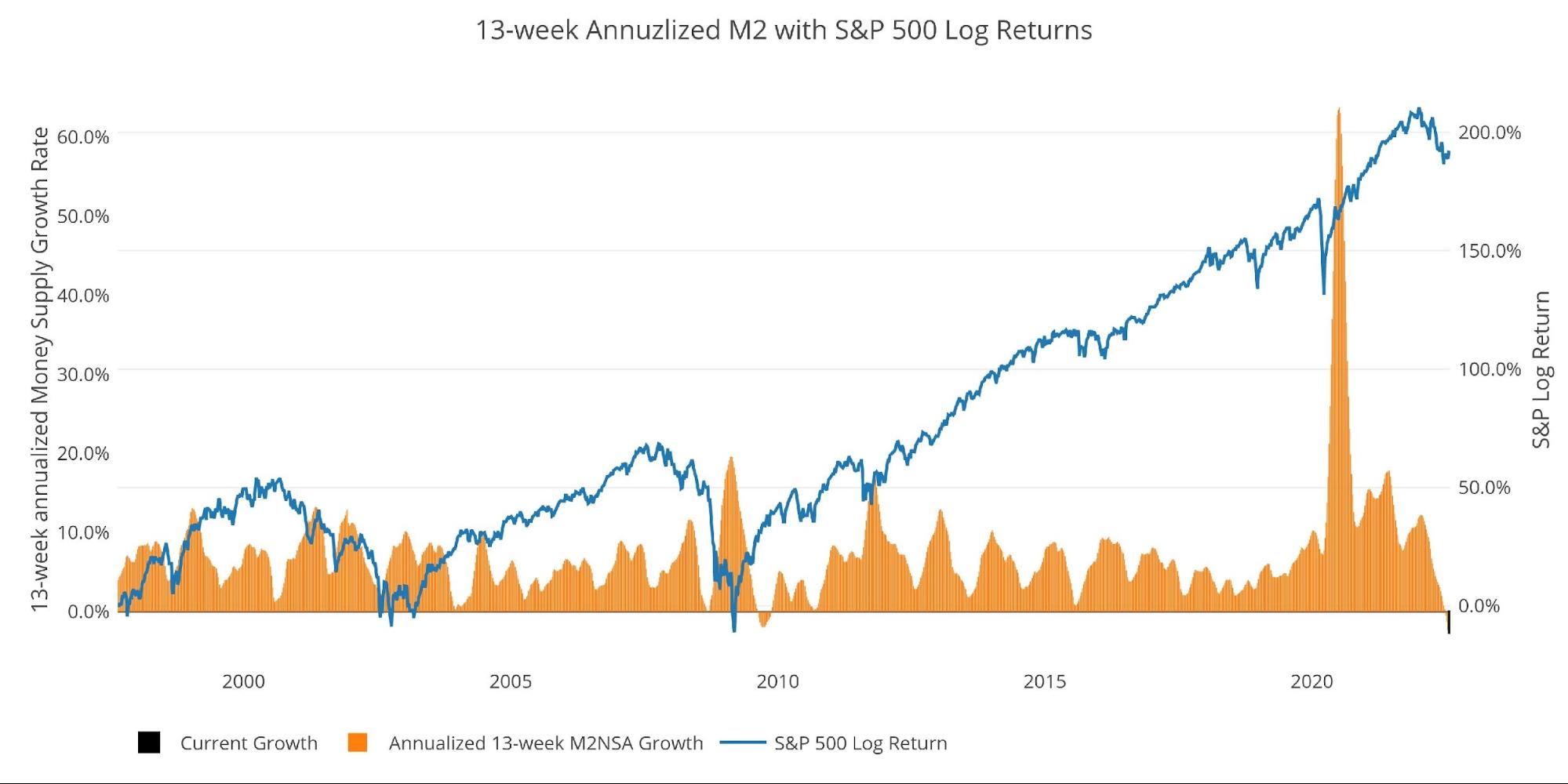

Taking a historical look at the 13-week annualized average also shows the current predicament. This chart overlays the log return of the S&P. Mr. Wenzel proposed that large drops in Money Supply could be a sign of stock market pullbacks. His theory, derived from Murray Rothbard, states that when the market experiences a shrinking growth rate of Money Supply (or even negative) it can create liquidity issues in the stock market, leading to a sell-off.

While not a perfect predictive tool, many of the dips in Money Supply precede market dips. Specifically, the major dips in 2002 and 2008 from +10% down to 0%. The economy is now grappling with a peak growth rate of 63.7% in July 2020 down to -2.5%. This is a major collapse.

The market may have rebounded off the lows, but it seems unlikely to reach new all-time highs without more liquidity from the Fed.

Please note the chart only shows market data through August 1 to align with available M2 data.

Figure: 10 13-week M2 Annualized and S&P 500

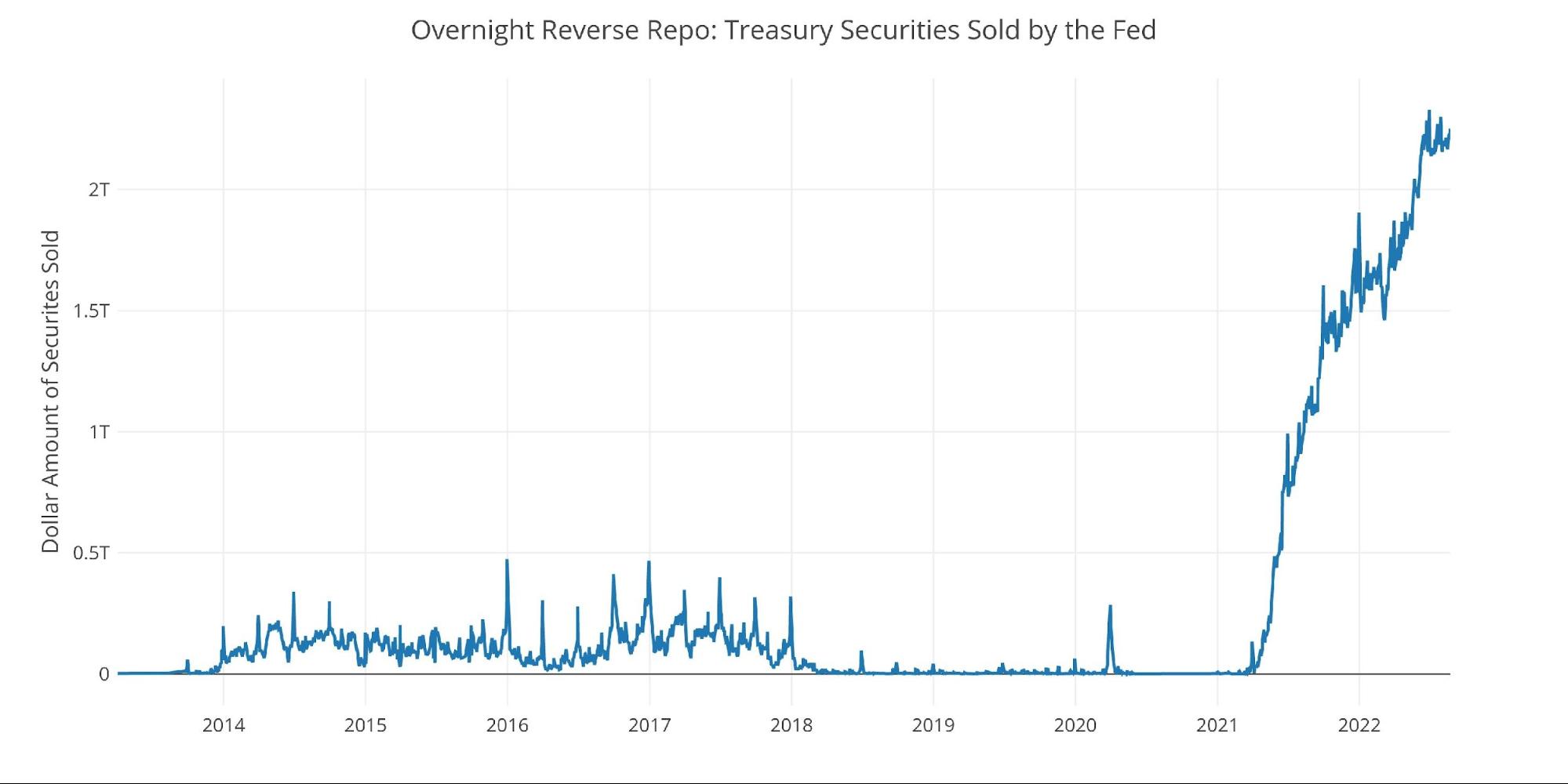

One other consideration is the massive liquidity buildup in the system. The Fed offers Reverse Repurchase Agreements (reverse repos). This is a tool that allows financial institutions to swap cash for instruments on the Fed balance sheet.

Current Reverse Repo exceeded $2T on May 23 for the first time in history and has stayed above $2T ever since. This dwarfs the old record of ~$500B in 2016-2017. Repos hit a record $2.3T on June 30th.

Bottom line, even though M2 has slowed there is still trillions of dollars in liquidity sloshing around. New money will not be available to prop up the stock market, but excess liquidity is still available to bid up prices and keep inflation elevated.

Figure: 11 Fed Reverse Repurchase Agreements

What it means for Gold and Silver

The market is currently experiencing an epic collapse in the Money Supply growth rate. Based on historical data, August is typically when Money Supply growth reaches the bottom. There should be an increase in the months ahead, but will it be enough to keep the bottom from falling out?

The Fed is doing everything it can to bring inflation back down without crashing the economy. Unfortunately, the current slow-down in money supply seems very likely to bring the drug-addicted economy to its knees. This is another reason that the Fed needs a quick inflation fight. The Fed has to go back to easy money sooner rather than later or deal with the consequences.

The money supply is not shrinking fast enough to bring inflation back down but it will damage many other parts of the economy. The economy will need to be rescued long before the Fed gets inflation back below 2%. When this happens, gold and silver will offer the best protection from the Fed’s reckless lifeline, which will turn out to be an anchor.

Data Source: https://fred.stlouisfed.org/series/M2SL and also series WM2NS and RRPONTSYD. Historical data changes over time so numbers of future articles may not match exactly. M1 is not used because the calculation was recently changed and backdated to March 2020, distorting the graph.

Data Updated: Monthly on fourth Tuesday of the month on 3-week lag

Most recent data: Aug 01, 2022

Interactive charts and graphs can always be found on the Exploring Finance dashboard: https://exploringfinance.shinyapps.io/USDebt/

Call 1-888-GOLD-160 and speak with a Precious Metals Specialist today!

Buka akaun dagangan patuh syariah anda di Weltrade.

Source link