Breaking Down the Balance Sheet

For the second month in a row, the Fed held true to its word and kept the balance sheet relatively flat. In aggregate, the balance sheet expanded by only $2B, though it did reach an all-time high mid-month. The drop to close out the month came as a result of $15B in MBS rolling off in the latest week.

The Fed is preparing to launch Quantitative Tightening (QT) in May with a monthly reduction of $95B. Given that the previous QT lasted 20 months and $750B before the market cracked, it seems highly improbable the Fed will make it even 12 months into this QT cycle.

The recent sell-off in the bond market has occurred just on the promise of higher rates and QT. If the Fed actually follows through, it must be hoping that magic can keep the markets levitating.

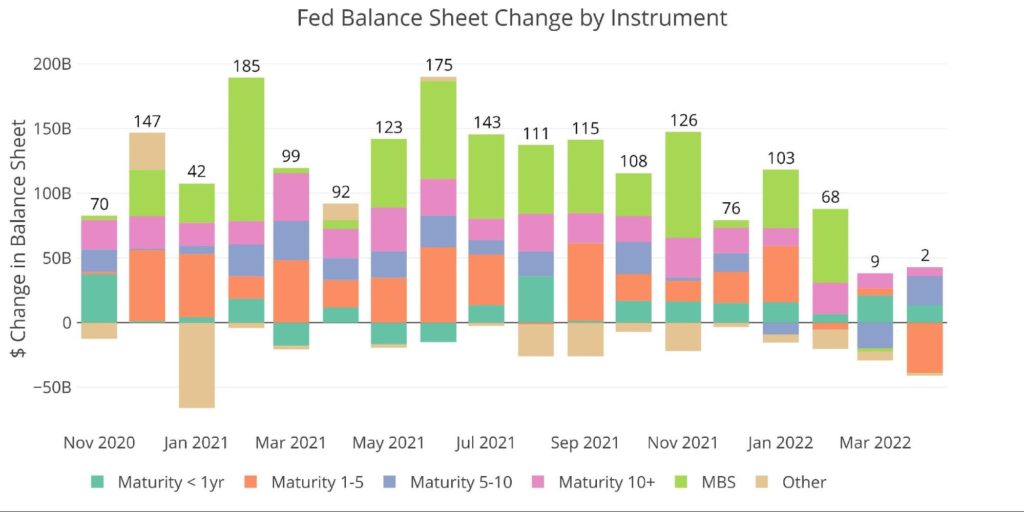

Figure: 1 Monthly Change by Instrument

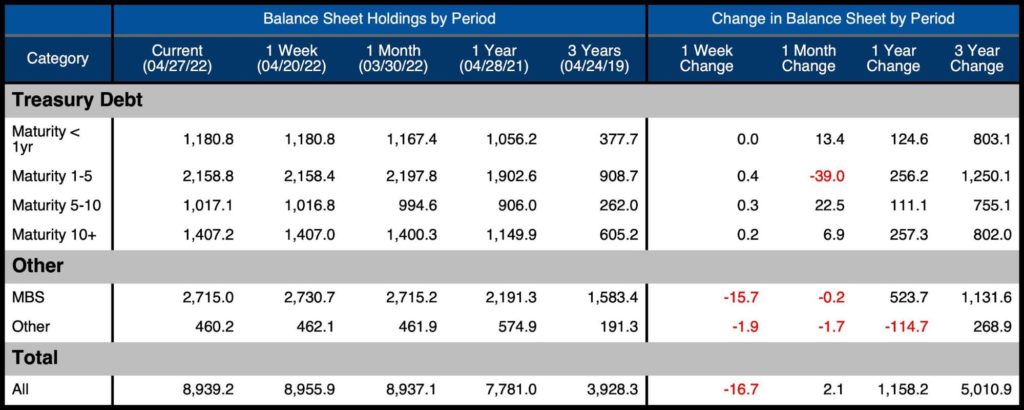

As shown in the table below, the Balance Sheet now stands at $8.94T down from $8.96T last week.

- 1-5 year maturities fell by almost $40B in the last month

- Other Treasury securities saw a combined increase of $42.8B over the same period

- MBS was practically flat for the month, down $200M

Figure: 2 Balance Sheet Breakdown

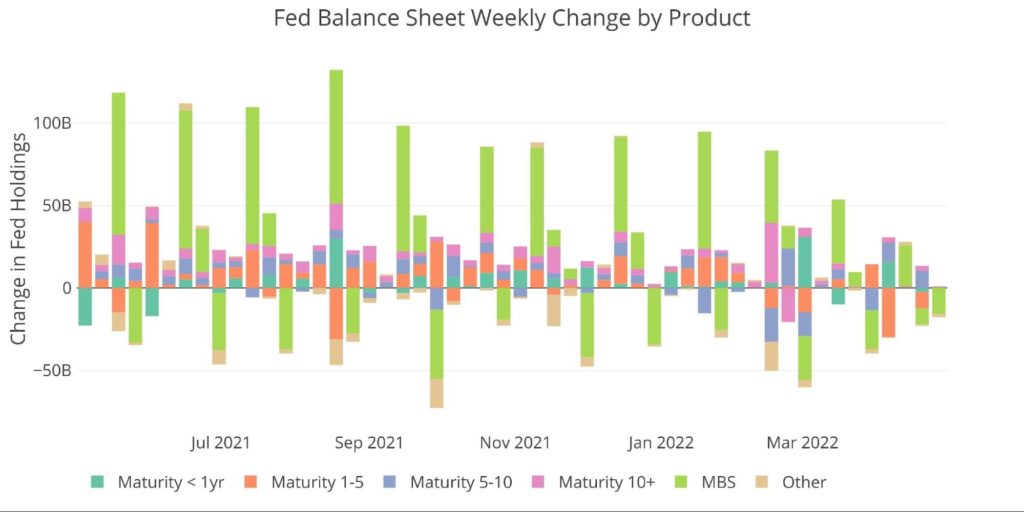

Looking at the weekly data shows how the activity on the balance sheet has been much more muted in recent weeks.

Figure: 3 Fed Balance Sheet Weekly Changes

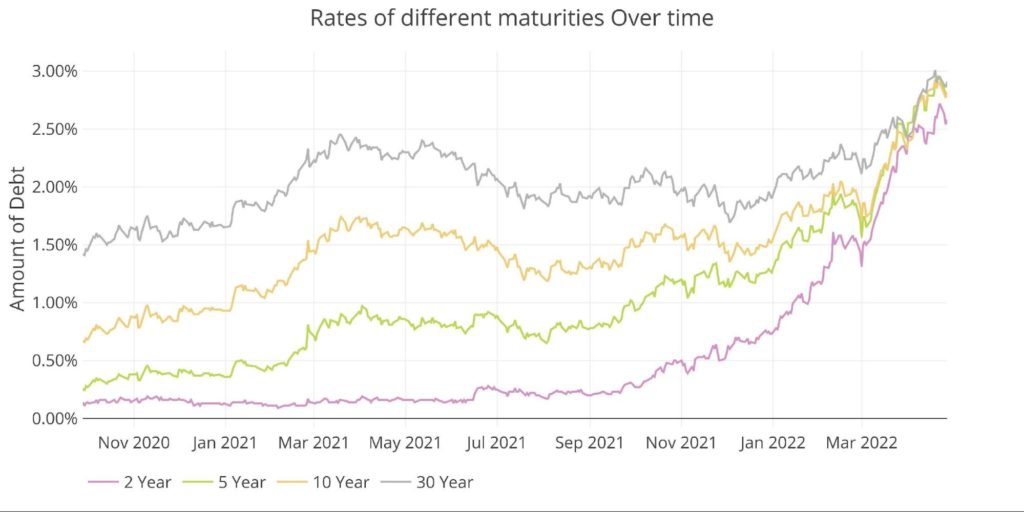

The bond market has certainly reacted to the Fed pulling back from the market. Some of the movement shown below is from traders pricing in the Fed stepping away; however, the bond market has lost its biggest buyer of Treasuries. It should be no surprise that rates along the entire yield curve have moved up rapidly in response.

Figure: 4 Interest Rates Across Maturities

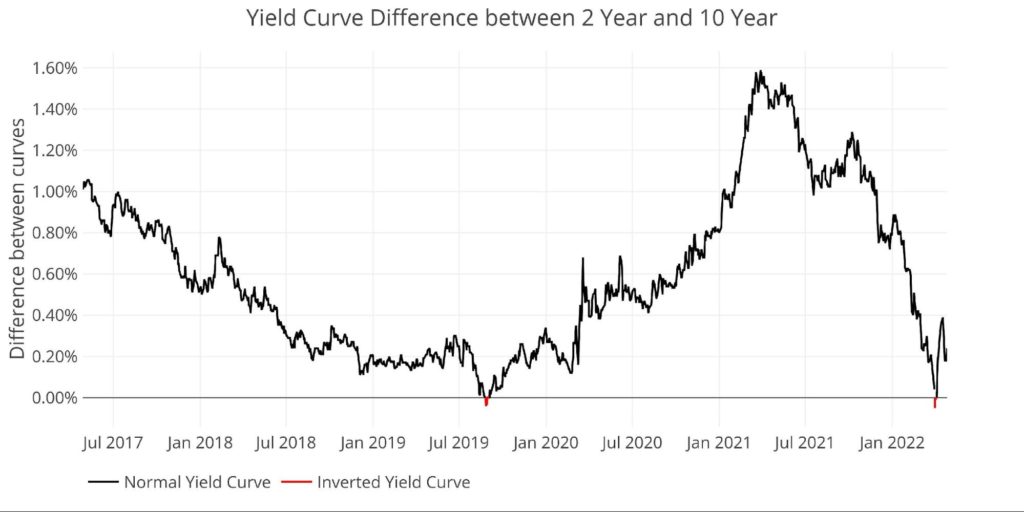

After a very brief inversion, the 2-10 year spread has widened quite rapidly.

Figure: 5 Tracking Yield Curve Inversion

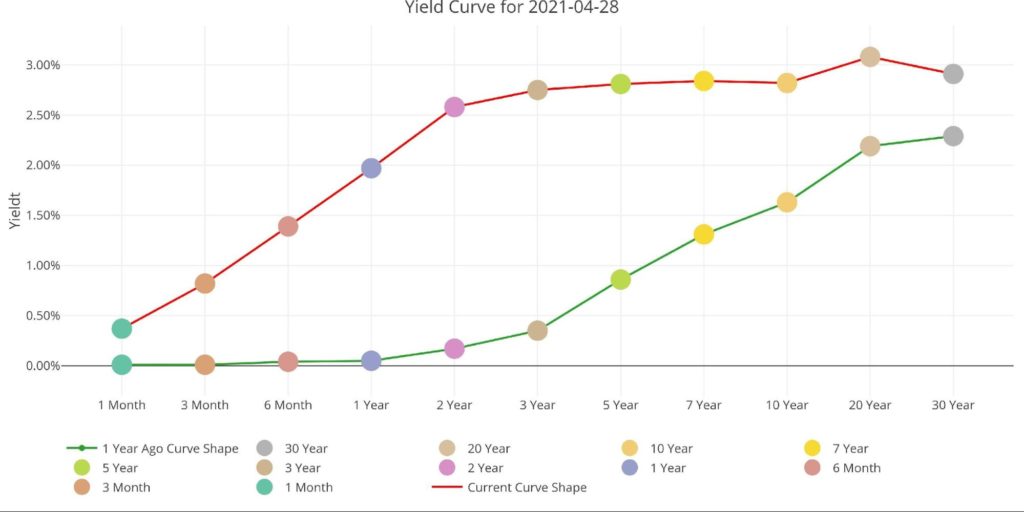

The chart below shows the entire yield curve compared to one year ago. The flattening can be seen in the red line on top. It is very flat, but no longer inverted.

Figure: 6 Tracking Yield Curve Inversion

The Fed Monetization

The Fed monetized almost all the debt for 2020-2021. However, the Treasury is now issuing far less debt than it was during that time. This means the Fed can actually step back from the market and it shouldn’t create too much turmoil in the immediate future.

This could change quickly though if any of the situations below were to occur:

- Yields were to spike putting pressure on the budget (the early stages of this are in motion)

- The tax revenue windfall dries up as the market trades sideways or down

- Foreigners start to dump their bonds (see below)

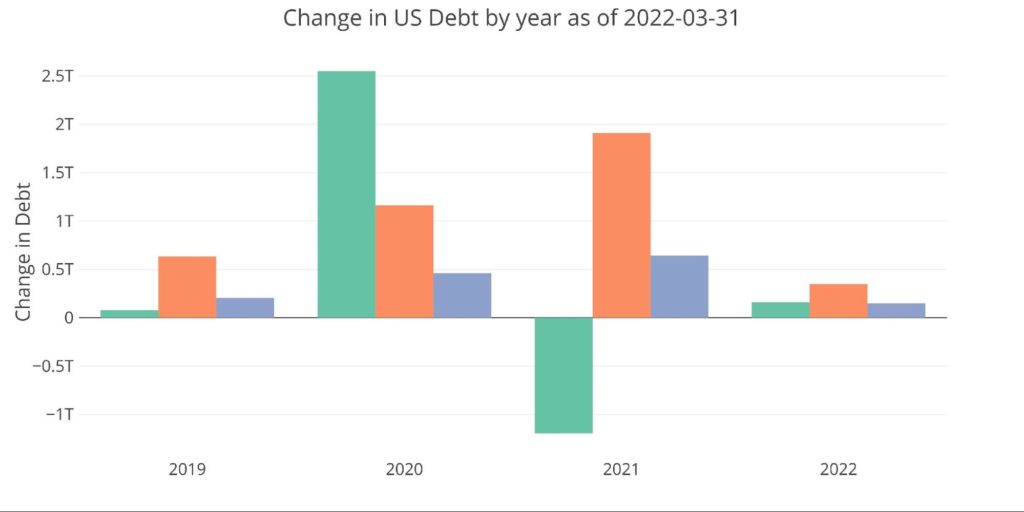

Figure: 7 Debt Issuance by Year and Instrument

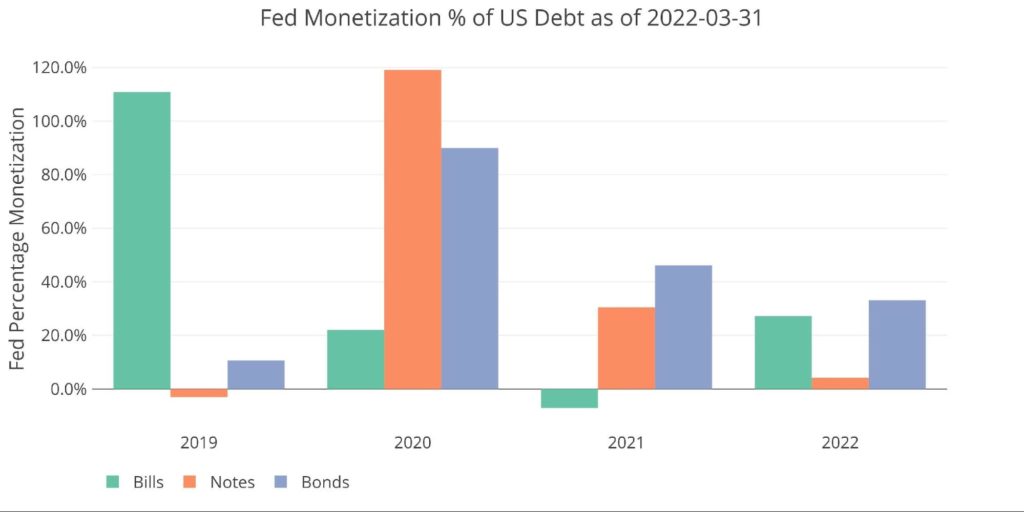

With much smaller issuance in 2022, the Fed has “only” monetized:

- 27.2% of the $159B in Bills

- 4.2% of the $348B in Notes

- 33.1% of the $150B in Bonds

Figure: 8 Fed Purchase % of Debt Issuance

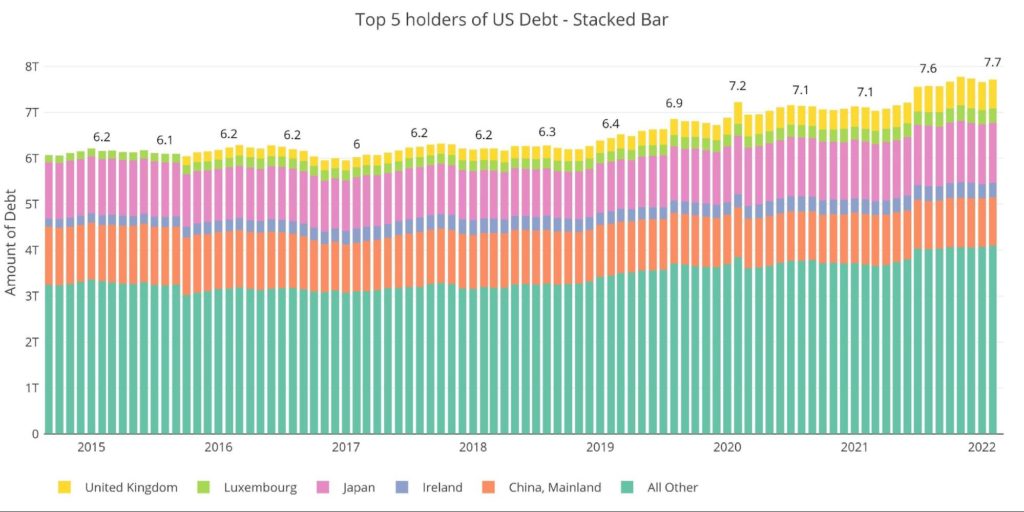

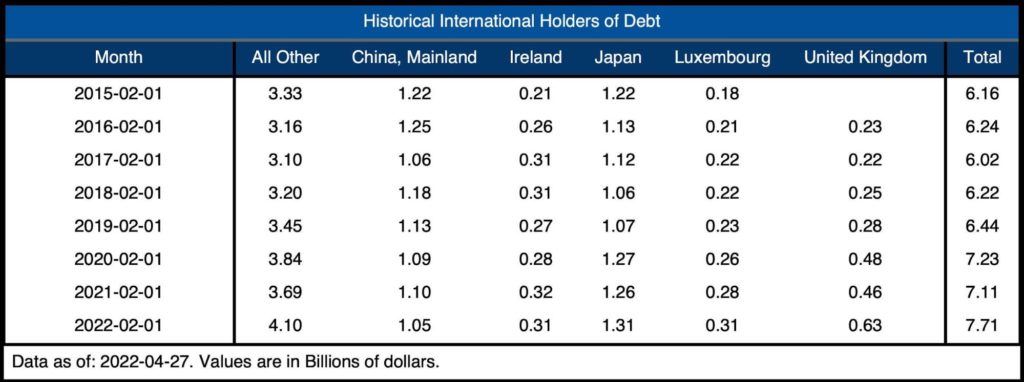

Who Will Fill the Gap?

The chart below looks at international holders of Treasury securities. International holdings are down $50B from the peak in Nov 2021. Of the 5 biggest holders, 4 have trimmed Treasury holdings since November with the UK being the lone exception.

Note: Data was last published as of February

Figure: 9 International Holders

The table below shows how debt holding has changed since 2015 across different borrowers. It’s quite incredible that since Feb 2020, international ownership has increased by less than $500B against an increase in total debt that exceeds $7T.

Figure: 10 Average Weekly Change in the Balance Sheet

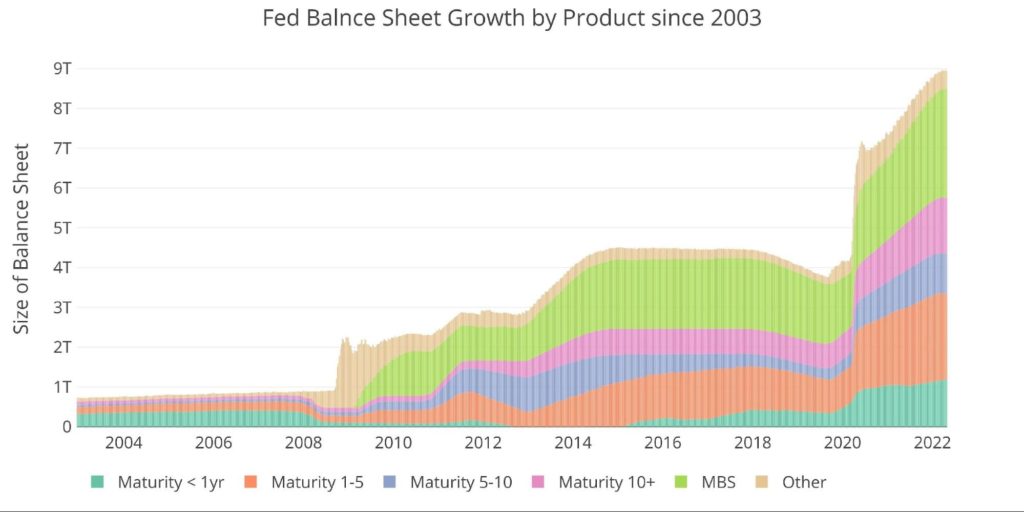

Historical Perspective

The final plot below takes a larger view of the balance sheet. It is clear to see how the usage of the balance sheet has changed since the Global Financial Crisis. The tapering from 2017-2019 can be seen in the slight dip before the massive surge due to Covid.

There is no way the Fed will come close to shrinking the balance sheet at this stage. Most forecasters are suggesting the Fed can get down to $6T before causing serious pain in financial markets, a $3T reduction. This seems laughable given how little it took in 2018 to send the markets into a tailspin (a decrease of $750B).

At least one positive for the Fed is a stalemate in Congress against surging tax revenues. If this helps shore up the Federal Budget deficit, then maybe they can push into QT. Unfortunately, this might be a temporary relief for everyone before interest rates start rising, debt starts exploding, and the Fed is back to monetizing.

Figure: 11 Historical Fed Balance Sheet

What it means for Gold and Silver

The Fed has been mostly talk on interest rates with only one 25bps hike so far. It has followed through with its promise to stop QE though. If the reaction in the bond market is any indication, things could get very precarious as the Fed attempts to shrink its balance sheet and raise interest rates “aggressively”.

The Fed is going from the biggest buyer of treasuries to the biggest seller. Same thing for MBS. In this environment, it’s hard to think there will not be major repercussions. The last QT cycle started in Dec 2017 and ended by Aug 2019. With the Fed promising to be more aggressive this time ($95B a month), how many months will the Fed get into QT before the legs fall out from under the bond market?

An equivalent $750B reduction will occur within 8 months. Can the Fed make it to 10 months of QT (~$1T) before things fall apart? Unlikely. Just because something is inevitable does not make it imminent. In this case though, “imminent” seems like a more appropriate term if the Fed stays on its promised trajectory.

Data Source: https://fred.stlouisfed.org/series/WALCL and https://fred.stlouisfed.org/release/tables?rid=20&eid=840849#snid=840941

Data Updated: Weekly, Thursday at 4:30 PM Eastern

Last Updated: Apr 27, 2022

Interactive charts and graphs can always be found on the Exploring Finance dashboard: https://exploringfinance.shinyapps.io/USDebt/

Call 1-888-GOLD-160 and speak with a Precious Metals Specialist today!

Buka akaun dagangan patuh syariah anda di Weltrade.

Source link