A Dramatic Yield Curve Transition From a Steep Front to Back End Flatness – Mish Talk

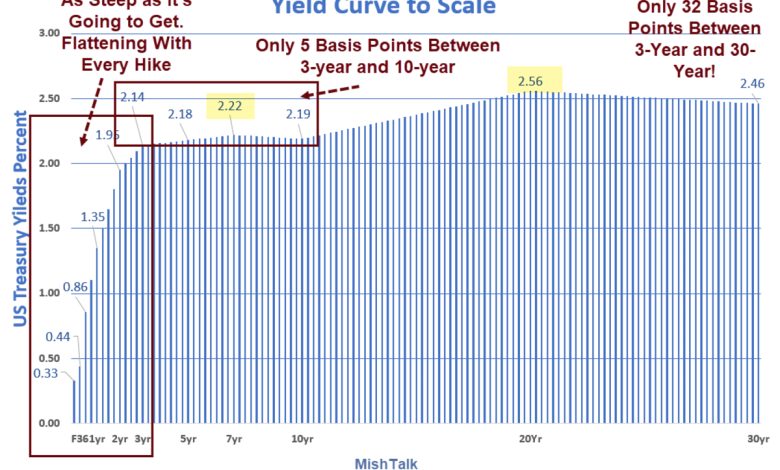

Yield Curve data from New York Fed, chart by Mish

On Wednesday, the Fed hiked interest rates for the first time since 2018.

The lead chart is as of the close yesterday. Yellow highlight are inversion spots.

The hike was 25 basis points BPs (a quarter-point hike) as widely expected.

Yield Curve Comments

- The front end of the curve is as steep as it’s going to get. Every hike will flatten the front end.

- The Effective Fed Funds rate rose by a quarter point to about 0.33 percent from 0.08 percent.

- At one point on Wednesday, the spread between the 5-year and 10-year notes inverted. The 5-10 spread closed at 1 basis point.

- The 7-10 spread is inverted by 3 BPs.

- The 20-30 spread is inverted by 10 BPs.

- The 5-10 spread is 1 BP.

- The 3-10 spread is 5 BPs.

- The 2-10 spread is only 24 BPs

- The 3-30 spread is only 32 BPs

Inversion means a shorter-term note has a higher yield than a longer-term note.

Economists watch the 2-10 spread as a recession indicator.

Treasury Yields December 2021 to Date

Yield Curve data from New York Fed, chart by Mish

This is a very flat curve between 3 and 30 years and is poised to get flatter as the Fed hikes.

Yield Curve Spreads Since January 2021

Yield Curve data from New York Fed, chart and calculations by Mish

Chart Notes

- Less than a year ago the 2-10 spread was 159 BPs. With only a single hike, the spread collapsed to 24 BPs.

- Unless the 10-year bond further sells off (yields rise), another quarter-point hike will flatten if not invert the 2-10 spread.

Fed Stops Hiking When 2-10 Inverts

History shows the Fed generally stops hiking as soon as the 2-10 spread inverts for longer than a month.

The Fed has hiked up to the point of causing a 2-10 inversion, but then it stops. Greenspan managed an additional hike or two one time.

You have to go back to the Volcker Fed in 1978 to find a major exception. Powell is no Volcker.

Let those thoughts sink in as you ponder the Fed’s dot plot of rate hike expectations.

Dot Plot

Fed Dot Plot of rate hike expectations. Chart from FOMC, annotations by Mish.

The median fed expectation for the end of 2022 is a total of 7 quarter-point hikes in 2022 and 3 or more hikes in 2023.

Scroll to Continue

Not Gonna Happen!

Heading into the FOMC meeting there was discussion of the Fed steepening the curve via very hawkish balance sheet reduction.

See Beware of a Very Aggressive Steepening of the Yield Curve by the Fed

I kept an open mind on this but had my doubts.

My doubts are now resolved.

Hawkish Fed? No, This Was a Dovish Fed Meeting

Yesterday, I commented Hawkish Fed? No, This Was a Dovish Fed Meeting

The Fed penciled in 7 rate hikes this year and 4 more next year. Who believes this?

What we have is a Punt by the Fed.

I am quite certain the Fed does not want to upset the stock market or housing. You can see it in the reaction today, albeit from very oversold conditions.

Economy Far Weaker Than Most Think

This economy is far weaker than most believe. I side with Steph Pomboy on this.

These Tweets are in reference to Fed Chair Jerome Powel telling everyone multiple times after the meeting how “strong” the economy is.

Stock Market Crash and Recession Anyway

As concerned as the Fed might be about inflation and an inverted yield curve, they are clearly more concerned about a stock market selloff and causing a recession by QT or hiking.

The Fed can try to tiptoe its way to a soft landing but it will get in no more than three more hikes in my estimation, and more likely only two.

Most People Have No Idea How Much Stocks are Likely to Crash

I stick with my call Most People Have No Idea How Much Stocks are Likely to Crash QT or not.

Demand destruction from that crash will lead to a recession (if not before).

Tiptoe Addendum

This post originated at MishTalk.Com.

Thanks for Tuning In!

Please Subscribe to MishTalk Email Alerts.

Subscribers get an email alert of each post as they happen. Read the ones you like and you can unsubscribe at any time.

If you have subscribed and do not get email alerts, please check your spam folder.

Mish

Source link