I love exploring data to try and understand complex situations. My career has mainly been in finance giving rise to the name: Exploring Finance. Using data to explore the current financial landscape shows an unsustainable situation, which has led me to identify gold and silver as the best defensive investments.

I explore multiple data sources each month to examine this hypothesis in the Exploring Finance series. Much of this started in my frustration that gold and silver had such a poor performance over the last decade given the fundamental backdrop. The market clearly did not agree with my view, so was I missing something? Thus, my objective in exploring the data is two-fold:

- I want to test my theory rigorously and make sure I don’t let personal biases cause me to overlook or ignore the data.

- Identify a change in trend that might be the “Canary in the Coal Mine” predicting the inevitable collapse of the dollar is quickly becoming imminent.

When exploring data, nothing is more interesting than large deviations from the trend. Deviations can require a re-examination of your thesis to ensure the underlying fundamentals have not changed. Alternatively, they could show that a current trend is rapidly picking up momentum. Thus, I am always on the lookout for new data to track that could show deviations.

Peter Schiff did a Podcast in 2020 as the oil market was going negative. He asked the question, “what if the opposite were to happen in gold and silver?”. Meaning, in March 2020, no one wanted oil, so the market had to actually pay people to take delivery. There were so many oil contracts maturing in the futures market that the excess physical supply drove the cost negative as people tried to escape taking delivery. Oil became free, as long as you would take it.

The opposite in gold and silver would be a long contract that wants delivery, yet there is no physical metal to be delivered. All of a sudden, the price would spike as short holders needed to acquire physical metal to deliver. This was an interesting theory, so I started looking closely at the Comex delivery data.

This report shows the ownership of physical metal changing hands within Comex vaults. Every month, long contract holders “stop” delivery notices while short holders “issue” delivery notices. This gives name to the “Issues and Stops Report”. I was looking for deviations from the average.

Gold

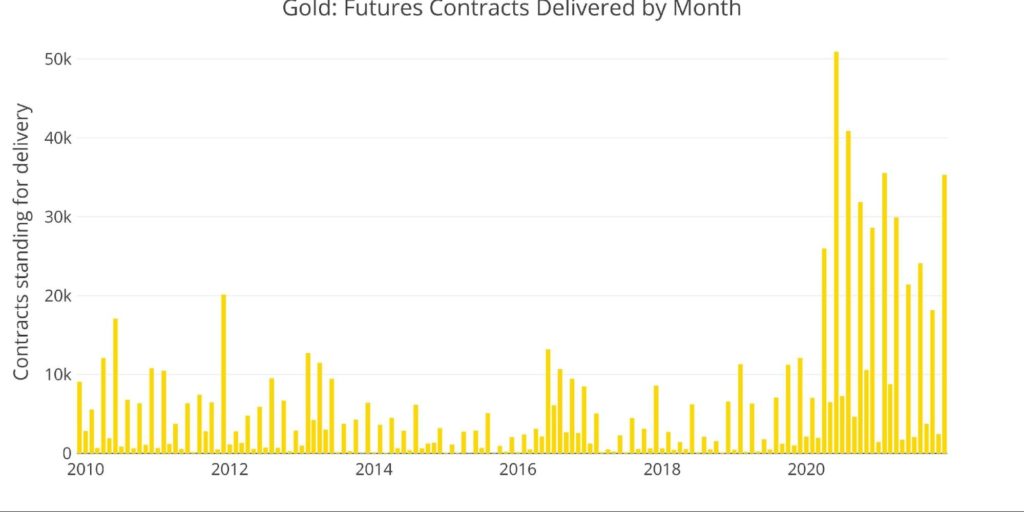

The chart below shows the monthly delivery notices going back to 2010. As shown, 2020 started smashing the old monthly averages regularly.

Figure: 1 Gold Monthly Delivery Volume

While the physical market did not break in 2020, it certainly came under more pressure. In my opinion, this data source could identify early signs of market stress in gold and silver. If/when the dollar starts to implode and the market wants physical metal, it will materialize in the futures market first. So, I now track this data every month. This has given rise to the monthly countdown and delivery results in the Exploring Finance series.

As mentioned in the most recent countdown and results, December 2021 was not a record month, but it was still very high by historic standards (last bar in the chart above).

While perusing the internet over the holidays, I came across a post that discussed the role of “House” accounts in the Issues and Stops report.

The report shows H and C accounts representing House and Client accounts. This will show metal transferring to or from individual investors with the bank house accounts on the other side. Metal moving from the House to the Client means investors are taking ownership of physical metal directly from the bank. The metal could stay in the Comex vault, and even under the same custodian, but moving from a house to client account is an entirely different owner. In essence, this could be metal moving from weak hands to strong hands.

I pulled historical PDF reports from the Web Archives. Utilizing some PDF scraping techniques in R, I was able to read in a decade’s worth of data. The results are astonishing.

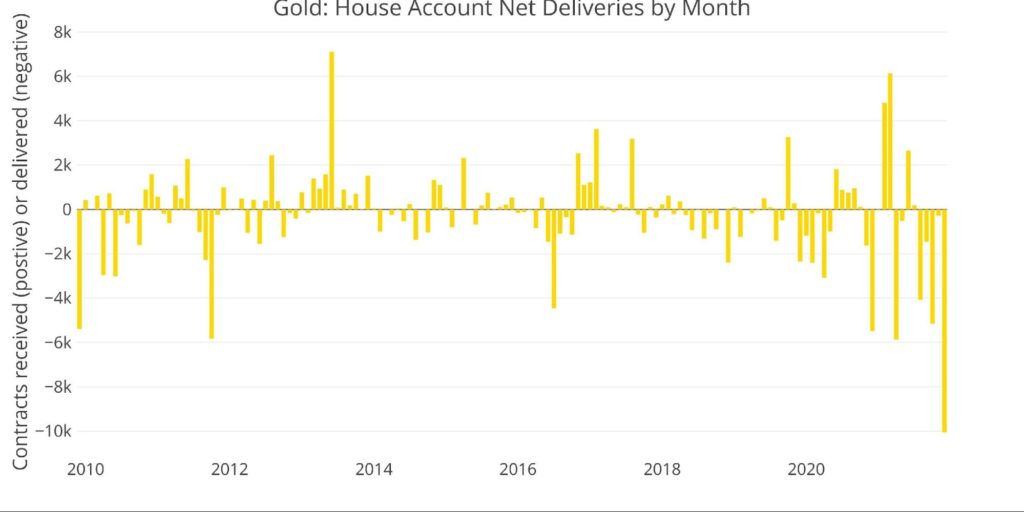

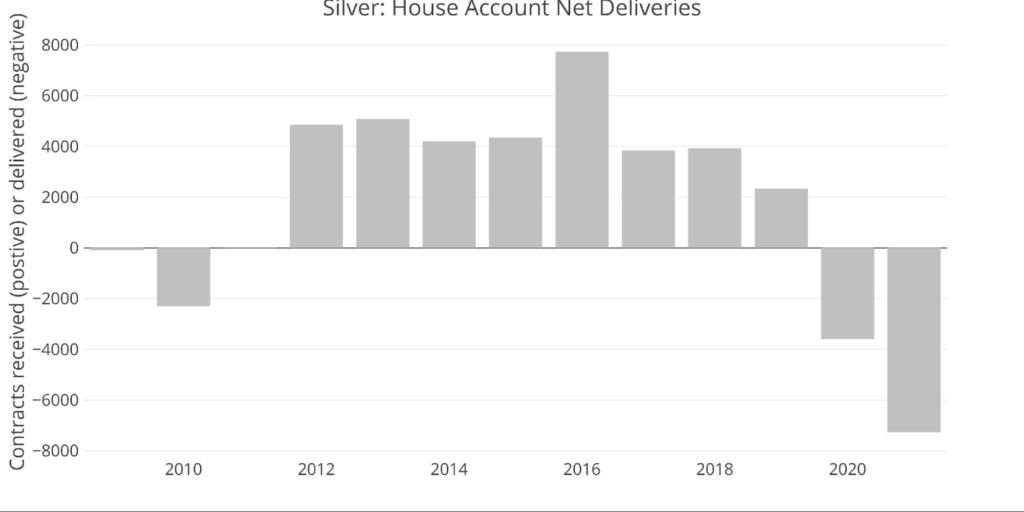

The chart below shows delivery to and from the house accounts. Negative values represent money leaving the house and positive values show metal coming into house accounts. December 2021 obliterated any other month on file by nearly double.

Figure: 2 Gold Monthly House Account Activity

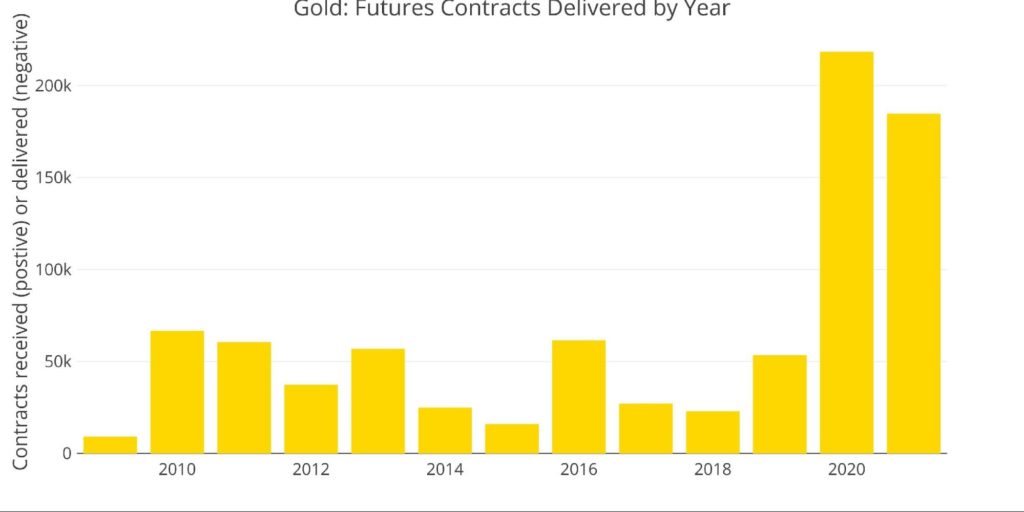

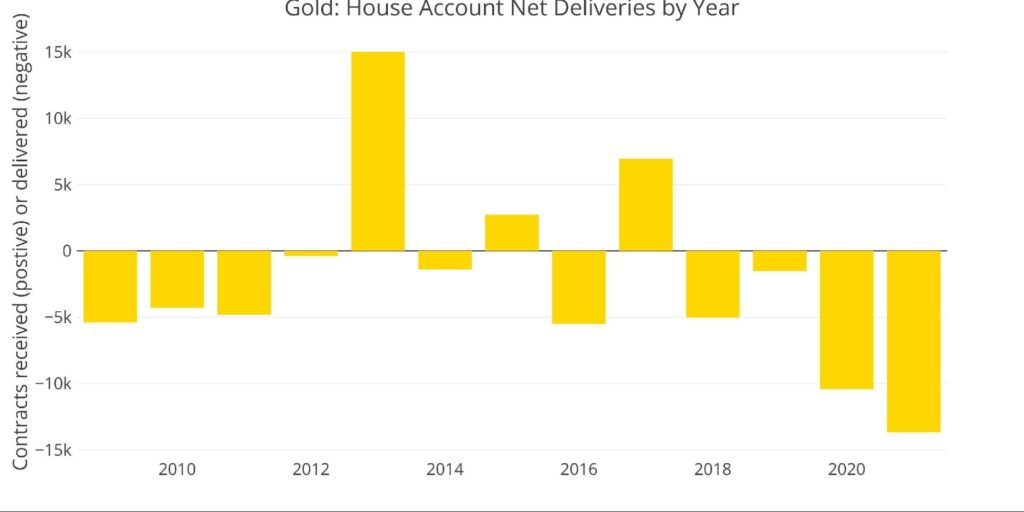

For the past several months I have been commenting on the fact that 2021 delivery volume came up short of the record in 2020 as shown below.

Figure: 3 Gold Yearly Delivery Volume

However, under the surface, a record had been broken due to the activity in December. 2021 saw the most metal move from bank house accounts to client accounts on record.

Figure: 4 Gold Yearly House Account Activity

Digging deeper into the data shows the two big culprits as Bank of America (via the old Merrill Lynch) and Macquarie. More on this below, but first a look at silver.

Silver

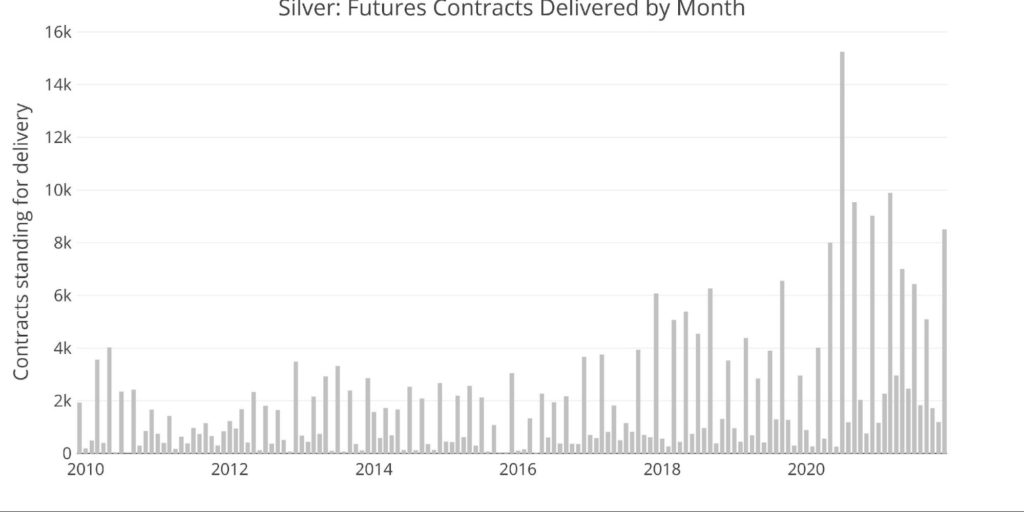

Similar to gold, delivery volume started to pick up in silver around May 2021.

Figure: 5 Silver Monthly Delivery Volume

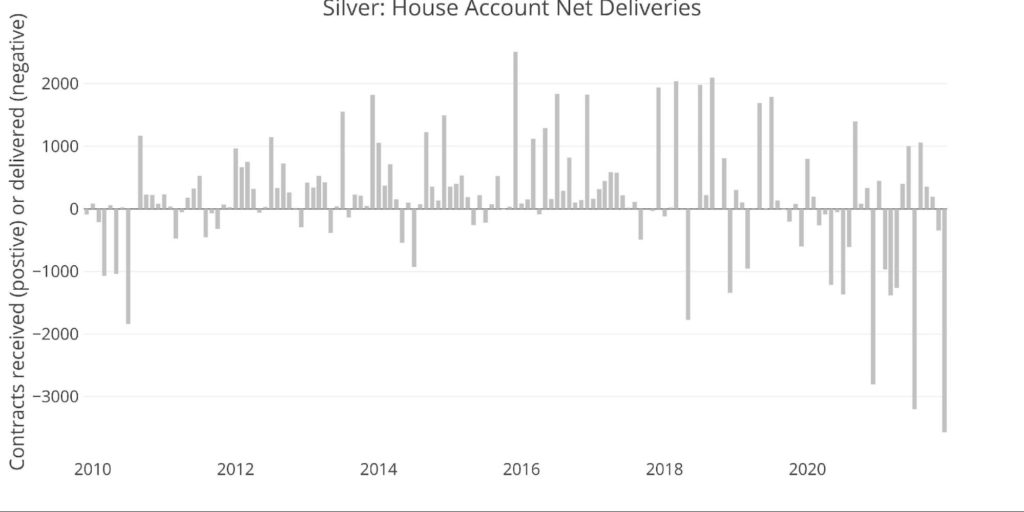

When looking at the flow to and from house accounts, this past December also saw an all-time record (far right bar).

Figure: 6 Silver Monthly House Account Activity

Overall delivery volume in 2021 was actually much closer to breaking the 2020 record than gold as shown below.

Figure: 7 Silver Yearly Delivery Volume

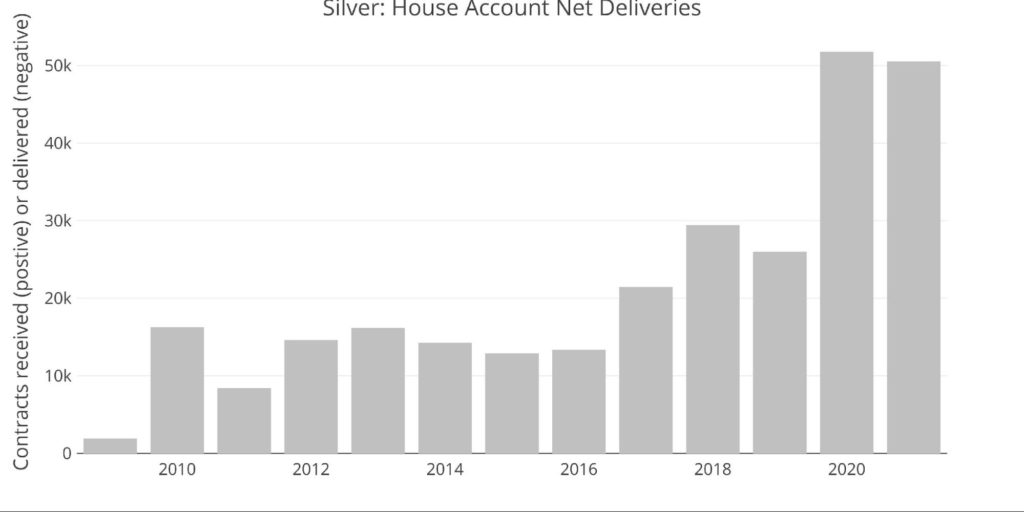

The house account picture looks vastly different. The amount of physical silver leaving house accounts in 2021 more than doubled the previous record.

Figure: 8 Silver Yearly House Account Activity

This does need to be put into context. The chart above shows that from 2012 to 2019, house accounts built up a massive stockpile of physical silver (suspiciously right after the 2011 price run which saw near-zero activity – but that’s another story).

The 8-year inventory surge was driven primarily by JP Morgan House taking delivery of more than 26,000 silver contracts over that period. Bank of Nova Scotia was a distant second at 9.5k followed by CME at a bit under 2k.

While the last two years have been impressive and is certainly considered a change in direction, silver has a long way to go to drain the house accounts of the physical. Especially when compared to gold.

Since Dec 2009, Comex House accounts have delivered out 26,808 contracts (valued at nearly $4.85B @ $1810 gold). Over the same time, Silver has seen Comex House accounts receive in 23,858 contracts (valued at $2.6B @ $22 Silver).

While Silver still has a long way to go, keep in mind that in just the last two years, gold house accounts have lost 23k contracts of the net 26.8k since 2009.

Back to December

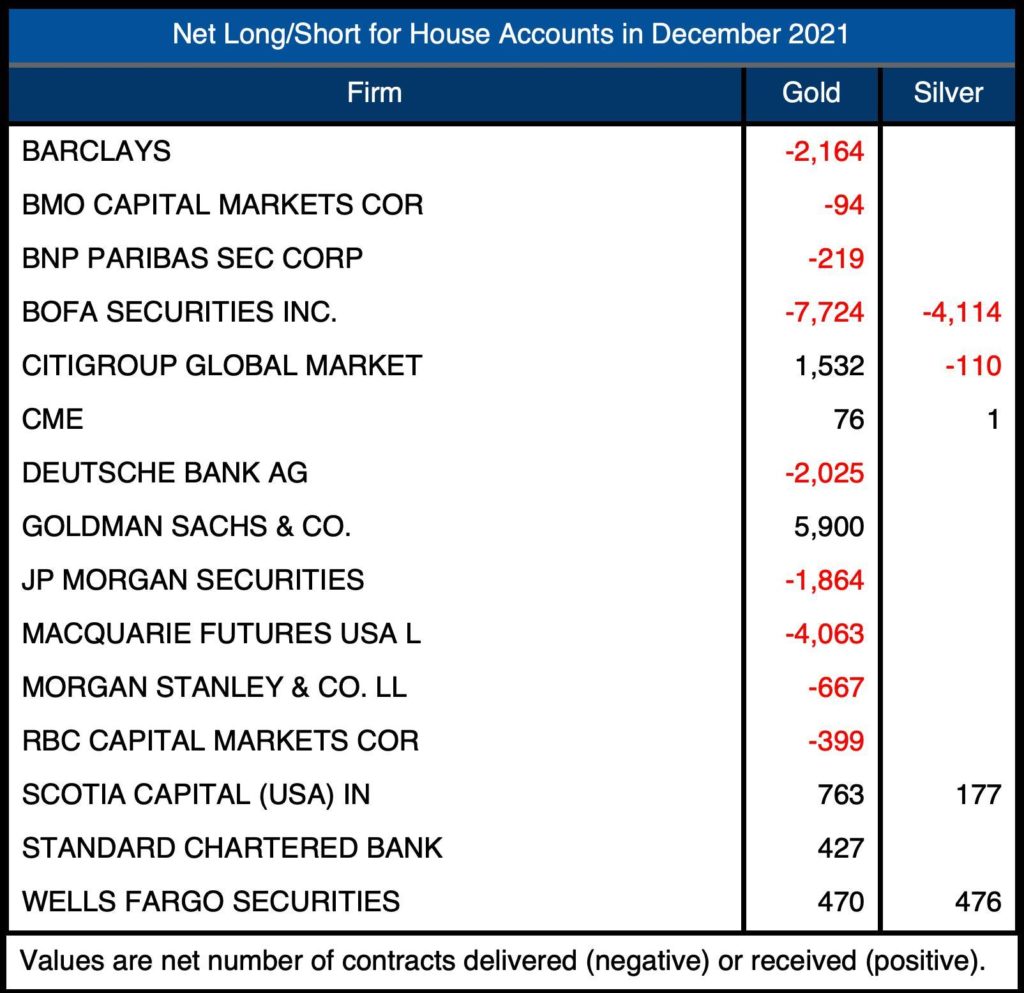

As mentioned above, the biggest losers in December were Bank of America and Macquarie shown in the table below.

Figure: 9 Correlation Table

Interestingly, BofA had spent the entire year building long positions in gold only to see them nearly wiped out in December.

One more dive deeper shows that in mid-December, BofA was actually out ~9,500 contracts, nearly 1,800 higher than the end of the month. In the Comex countdown, I follow the contracts opened mid-month for immediate delivery. Gold saw 4,547 such contracts in December. It’s probable BofA was a big part of this activity, back in the market trying to replenish their physical holdings ownership.

The 1,800 contracts BofA took back came from two sources: JP Morgan house account ~500 contracts and Barclays client accounts to the tune of ~1,300 contracts

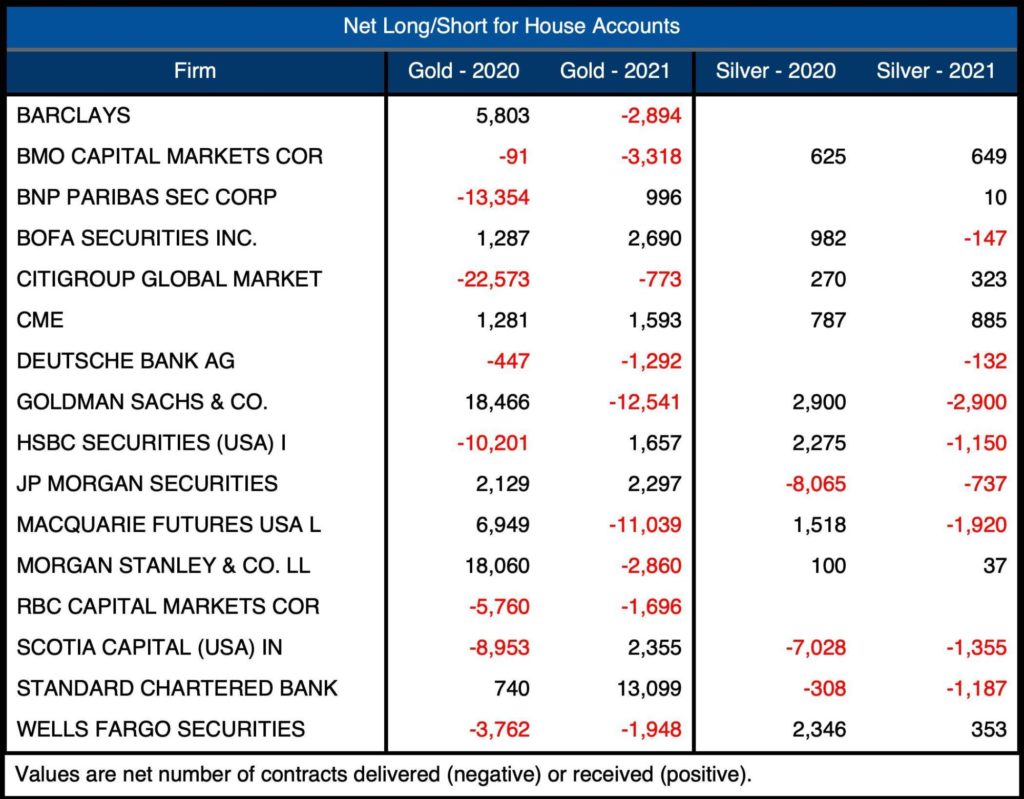

This can be seen in the table below where BofA finished the year net positive 2,690 contracts. This table shows the net movement in house accounts for gold and silver in 2020 and 2021.

Interesting points to note:

Gold

- Morgan Stanley was busy accumulating in 2020 but passed the torch to Standard Chartered in 2021

- Goldman accumulated in 2020 but dropped 65% in 2021

- Citi and BNP lost big hoards in 2020

Silver

- 2020 was a year of accumulation for all but JP Morgan and Scotia

- 2021 saw the reverse with most holders dropping positions

Figure: 10 Correlation Table

What does it all mean?

Unfortunately, the short answer is that I am unsure. Why is so much metal migrating from house accounts to client accounts all of a sudden? Are banks trying to keep a lid on prices by using their inventory? Do they believe prices will drop, perhaps hoping to buy back later as they did after the price run-up from 2010-2011 (Figures 4 & 8)?

Or, is this the Canary in the Coal Mine? Are investors waking up and taking ownership? As the stock report shows, metal has been leaving Comex vaults at a pretty steady clip. Are investors taking ownership and then taking actual delivery by getting metal out of the Comex vaults? Maybe this shows up in a big way on the next few stock reports.

Time will tell, but I know this will be another data point I am tracking each month. December was so massive; I will be watching to see if we repeat in the coming months.

Much of what goes on under the surface is impossible to see, so all we can do is track the available data and see how things materialize. Across all the data, everything is pointing to the fact we are closer to the end than the beginning. Perhaps this data will provide an early warning sign that the inevitable collapse of fiat is, in fact, growing much more imminent!

Data Source: Comex Issues and Stops

Data Updated: Nightly around 11 PM Eastern

Call 1-888-GOLD-160 and speak with a Precious Metals Specialist today!

Buka akaun dagangan patuh syariah anda di Weltrade.

Source link